Insurance Talk V2, Anything and everything about insurance

Insurance Talk V2, Anything and everything about insurance

|

|

Dec 29 2013, 08:27 PM Dec 29 2013, 08:27 PM

|

Moderator

10,308 posts Joined: Jan 2003 From: Kuala Lumpur |

Thanks for the explanation.

|

|

|

|

|

|

Jan 10 2014, 07:24 PM

|

Junior Member

381 posts Joined: Feb 2012 |

Do you all request free gift (book, umbrella etc) from your insurance agent ??

Every year?? |

|

|

Jan 11 2014, 01:01 PM

|

|

Newbie

1 posts Joined: Mar 2008 |

Any Prudential agent here, want to ask somethings, my sis bought a Prulife Ready plan, medical card room & board RM 150, what happen if she stay a room higher than that amount??

|

|

|

Jan 11 2014, 01:11 PM

|

Senior Member

2,173 posts Joined: Jan 2012 From: Butterworth, Penang |

QUOTE(woodyzai @ Jan 11 2014, 01:01 PM) Any Prudential agent here, want to ask somethings, my sis bought a Prulife Ready plan, medical card room & board RM 150, what happen if she stay a room higher than that amount?? PRUlife Ready is the main plan and not the medical card. For PRUflexi med medical card, if you stay at a higher room, you only need to pay the differences, no penalties. If you stay at a lower room, Prudential will reimburse the differences to you. Eg. If you stay in rm100 room, Prudential will pay back Rm50 per day. For PRUhealth medical card, if you stay at a higher room, you need to pay the differences, no penalties. But if you stay at a lower room, Prudential will not reimburse to you the variance. |

|

|

Jan 11 2014, 03:26 PM

|

Senior Member

5,613 posts Joined: Jun 2006 From: Cyberjaya, Shah Alam, Ipoh |

Hi...nothing related to insurance...but just wana say I'm quite impressed with prudential mutual investment team aka eastspring investment ... their unit trust return on some fund is phenomenon n beat unit trust industry standard....

|

|

|

Jan 11 2014, 08:18 PM

|

|

Senior Member

2,173 posts Joined: Jan 2012 From: Butterworth, Penang |

QUOTE(max_cavalera @ Jan 11 2014, 03:26 PM) Hi...nothing related to insurance...but just wana say I'm quite impressed with prudential mutual investment team aka eastspring investment ... their unit trust return on some fund is phenomenon n beat unit trust industry standard....    |

|

|

|

|

|

Jan 13 2014, 02:55 PM

|

Junior Member

191 posts Joined: Jan 2012 |

Hi just like to know the price for a top notch medical insurance package i'm looking for. I want a package that cover medical, a package that give me a medical card. A straight foward agreement that will pay all my hospital fee & room & not a package that is full of things in the Term & Conditions sections, like this don't cover that don't cover full. In the end i am paying for a package that don't give me much benefits.

|

|

|

Jan 13 2014, 04:26 PM

|

|

Junior Member

29 posts Joined: Nov 2013 From: Ipoh, Perak |

QUOTE(nujikabane @ Dec 2 2013, 10:06 PM) I understand that Insurance is generally associated to long-term commitment. Hi there,However, am wondering; is there any TPD insurance plan that caters for specific situations? Coz here's the thing; my father-in-law will be undergoing Lasik surgery, and even though the Doc mention that there are no known cases of people going blind due to the procedures, I would want to be proactive. As such, I plan to take TPD insurance plan for him, for this specific matter only. i.e once after the procedure is done, am not continuing with the plan. Is it possible? TPD is a by-product of Life Insurance. Meaning, you need to buy Life in order to buy TPD. And, insurance is usually referred as a long term commitment in terms of investment returns/ surrender value. If you only want to be covered, having cover for a short period, does not affect you. In your father-in-law's case, in case if only one eye is affected, then again TPD will not work. (Please do check the TPD description before you buy). If your father-in-law having life policies, he could have had TPD (subjective) in it - do check the expiry of the coverage. Thank you. Regards. |

|

|

Jan 13 2014, 04:31 PM

|

|

Junior Member

29 posts Joined: Nov 2013 From: Ipoh, Perak |

QUOTE(scottyvstheworld @ Jan 13 2014, 03:55 PM) Hi just like to know the price for a top notch medical insurance package i'm looking for. I want a package that cover medical, a package that give me a medical card. A straight foward agreement that will pay all my hospital fee & room & not a package that is full of things in the Term & Conditions sections, like this don't cover that don't cover full. In the end i am paying for a package that don't give me much benefits. Hi,I also wish there is such a plan but I am afraid that is not the case. That is why you need to choose carefully. The best I have come across so far is unlimited cover and renewable till age 100 but there are other conditions definitely! Well, I was told if insurance companies were to run no limit & all cover medical card - they will end up bankrupt in no time! Thank you. Regards. |

|

|

Jan 13 2014, 04:43 PM

|

|

Junior Member

29 posts Joined: Nov 2013 From: Ipoh, Perak |

QUOTE(HMMaster @ Dec 28 2013, 11:29 PM) Hi, Hi there,For AIA's A-Plus CriticalCare, is it that the sum assured for the CI will increase 1% per year? For example, If I purchase A-Lifelink 380k + A-PlusCriticalCare 100k (both with 1% anniversary bonus, max 20%) after 30years, the sum assured will be:- 380k*1%*20=76000 + 380000 = 456000 100k*1%*20=20000 + 100000 = 120000 Is the above calculation correct? Btw, any reason why AIA cash value higher than GE at 30years~? Your calculation is correct and it increases gradually 1% from the beginning of second policy year and by the beginning of 21st year, you will have a Sum Assured of RM 456K for life & RM 120K for Critical Illness. By the way, AIA has Critical Illness cover that pays up to 3 times and also Early Pay Critical illness Cover (in case you have not heard of it). I am not sure why you refer to 30 year but generally returns is based upon underlying fund performance - whether you want it to be aggressive, moderate &/or mild. Also, the returns you see in the Proposal is a projection. Actual performance may vary. You can also monitor your fund performances and in case not satisfied, you can do fund switchings. Thank you. Regards. |

|

|

Jan 13 2014, 04:47 PM

|

|

Junior Member

29 posts Joined: Nov 2013 From: Ipoh, Perak |

QUOTE(patrickthissen @ Jan 10 2014, 08:24 PM) Do you all request free gift (book, umbrella etc) from your insurance agent ?? Every year??  No - but I wish they send. Only received it in the first year! No - but I wish they send. Only received it in the first year! |

|

|

Jan 14 2014, 02:08 PM

|

|

Junior Member

29 posts Joined: Nov 2013 From: Ipoh, Perak |

QUOTE(blue_scott @ Dec 4 2013, 04:36 PM) Hi, is there any AIA agent here ? Hi, I guess the Premiere PA is not sold through agency as I do not see it in the list of products.Yesterday AIA telemarketer called me, and introduce me a PA plan 'Premiere PA'. Any idea what is that ? Couldn't find related info in website. Thanks! Thank you. Regards. |

|

|

Jan 14 2014, 05:05 PM

|

|

Junior Member

381 posts Joined: Feb 2012 |

QUOTE(joyce.ipoh @ Jan 13 2014, 04:47 PM) No - but I wish they send. Only received it in the first year!The agent gave book/umbrella to my cousin but no give me  Maybe because of my cousin pay insurance by cash, so the agent have to come collect money from him every month. I paying using credit card I guess I have to make a call to that agent... |

|

|

|

|

|

Jan 15 2014, 03:01 PM

|

Junior Member

11 posts Joined: Aug 2013 |

QUOTE(patrickthissen @ Jan 14 2014, 05:05 PM) I bought insurance from my cousin's friend. I didnt know that we can actually request for all these goods. Okay calling my agent now The agent gave book/umbrella to my cousin but no give me Maybe because of my cousin pay insurance by cash, so the agent have to come collect money from him every month. I paying using credit card I guess I have to make a call to that agent...  |

|

|

Jan 17 2014, 10:17 PM

|

Senior Member

1,290 posts Joined: Jan 2003 From: PD |

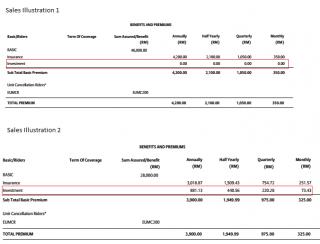

Hi Guys,

Agent quoted me the sales illustration as attached image. Anyone why is it a investment portion in one of the sales illustration?  Thanks This post has been edited by clsia1001: Jan 17 2014, 10:19 PM Attached thumbnail(s)

|

|

|

Jan 17 2014, 11:13 PM

|

|

Senior Member

2,479 posts Joined: Jan 2003 From: Cheras |

Wondering if anyone can comment on my situation. I currently do not have any outside insurance plan except from my company. I'll try to describe my situation in the least confusing manner as possible. My current age is 35.

July 2002: Started working with current company, I have AIA card, good medical plan in general. Feb 2014: Expected my last at the company since I'm planning to pursue my study overseas, will have to hand over my AIA medical card. March 2014: Start of period without medical card. September 2014: Expected to begin studying at US university for my Masters, I will be forced to buy university-sanctioned medical plan as requirement for any new students. June 2016: Anticipated time of graduation from US and return to Malaysia to work, I assume my future company that hires me will also offer medical card similar to AIA that I had previously. How often have I used the AIA medicall card from 2002-2014? Not often, once every 6 months maybe, for regular fever or flu, never been warded, paling teruk pun just injection for severe tonsilitis. Do I have a family? I am single, unmarried. My question: If I want a medical card to cater for normal fevers, and God-forbids, critical illness, I presume at my age, it will be RM350/mo premium? Correct me if I'm wrong. What would be the strategy if i foresee that I'll be having university-sanctioned insurance while continue paying RM350/mo to Malaysia just to "maintain" a medical card here? Or should I just get a medical card when I return to Malaysia in 2016 at age of 37 and presumably pay RM400/mo for medical card by then? |

|

|

Jan 17 2014, 11:49 PM

|

All Stars

11,954 posts Joined: May 2007 |

why u take bonus then resign from ur company?

|

|

|

Jan 17 2014, 11:58 PM

|

Senior Member

670 posts Joined: Aug 2005 |

QUOTE(my44 @ Jan 17 2014, 11:13 PM) Wondering if anyone can comment on my situation. I currently do not have any outside insurance plan except from my company. I'll try to describe my situation in the least confusing manner as possible. My current age is 35. its up to you . . . you can sign up a basic plan while maintain it for 2 years until you are back in MalaysiaJuly 2002: Started working with current company, I have AIA card, good medical plan in general. Feb 2014: Expected my last at the company since I'm planning to pursue my study overseas, will have to hand over my AIA medical card. March 2014: Start of period without medical card. September 2014: Expected to begin studying at US university for my Masters, I will be forced to buy university-sanctioned medical plan as requirement for any new students. June 2016: Anticipated time of graduation from US and return to Malaysia to work, I assume my future company that hires me will also offer medical card similar to AIA that I had previously. How often have I used the AIA medicall card from 2002-2014? Not often, once every 6 months maybe, for regular fever or flu, never been warded, paling teruk pun just injection for severe tonsilitis. Do I have a family? I am single, unmarried. My question: If I want a medical card to cater for normal fevers, and God-forbids, critical illness, I presume at my age, it will be RM350/mo premium? Correct me if I'm wrong. What would be the strategy if i foresee that I'll be having university-sanctioned insurance while continue paying RM350/mo to Malaysia just to "maintain" a medical card here? Or should I just get a medical card when I return to Malaysia in 2016 at age of 37 and presumably pay RM400/mo for medical card by then? or wait for 2016 & purchase when you are back in Malaysia. Insurance charges for 35 / 37 will not increase as much as what you have describe but in order to get a medical card you have to make sure you stay healthy for the 2 years . . . |

|

|

Jan 18 2014, 12:38 AM

|

|

Senior Member

2,479 posts Joined: Jan 2003 From: Cheras |

QUOTE(MNet @ Jan 17 2014, 11:49 PM) why u take bonus then resign from ur company? Sorry I don't get you. What bonus you talking about? This is purely about medical card. |

|

|

Jan 18 2014, 12:44 AM

|

|

Senior Member

2,479 posts Joined: Jan 2003 From: Cheras |

QUOTE(Colaboy @ Jan 17 2014, 11:58 PM) its up to you . . . you can sign up a basic plan while maintain it for 2 years until you are back in Malaysia or wait for 2016 & purchase when you are back in Malaysia. Thanks for the opinion. By "basic plan", what does it entail? More importantly, the estimated annual premium for 35-yr-old male like me. QUOTE(Colaboy @ Jan 17 2014, 11:58 PM) Insurance charges for 35 / 37 will not increase as much as what you have describe but in order to get a medical card you have to make sure you stay healthy for the 2 years . . . By "not much", can you say the increase is probably around RM20-RM30 per month from 35 age to 37 age? Also, is there some sort of medical checkup before I can get a medical card in Malaysia at the age of 37? |

|

Topic ClosedOptions

|

| Change to: |  0.0320sec 0.0320sec

0.75 0.75

6 queries 6 queries

GZIP Disabled GZIP Disabled

Time is now: 4th December 2025 - 10:13 AM |

Quote

Quote