Apr 17 2017, 08:02 AM

Apr 17 2017, 08:02 AM

QUOTE(adrianccseng @ Apr 15 2017, 11:08 PM)

1.

Oct * rm1347

Nov * rm1254

Dec * rm1300

Jan * rm1460

Feb * rm899

March * rm942

there's a restructure from 2017 tho. so the comm gets lesser compare to last yr

no assets no FD just saving account

oh wow, didn't knew that.

haven't contact the remaining 5 panel banks yet.

hopefully affin would approve then

Dear,Oct * rm1347

Nov * rm1254

Dec * rm1300

Jan * rm1460

Feb * rm899

March * rm942

there's a restructure from 2017 tho. so the comm gets lesser compare to last yr

no assets no FD just saving account

oh wow, didn't knew that.

haven't contact the remaining 5 panel banks yet.

hopefully affin would approve then

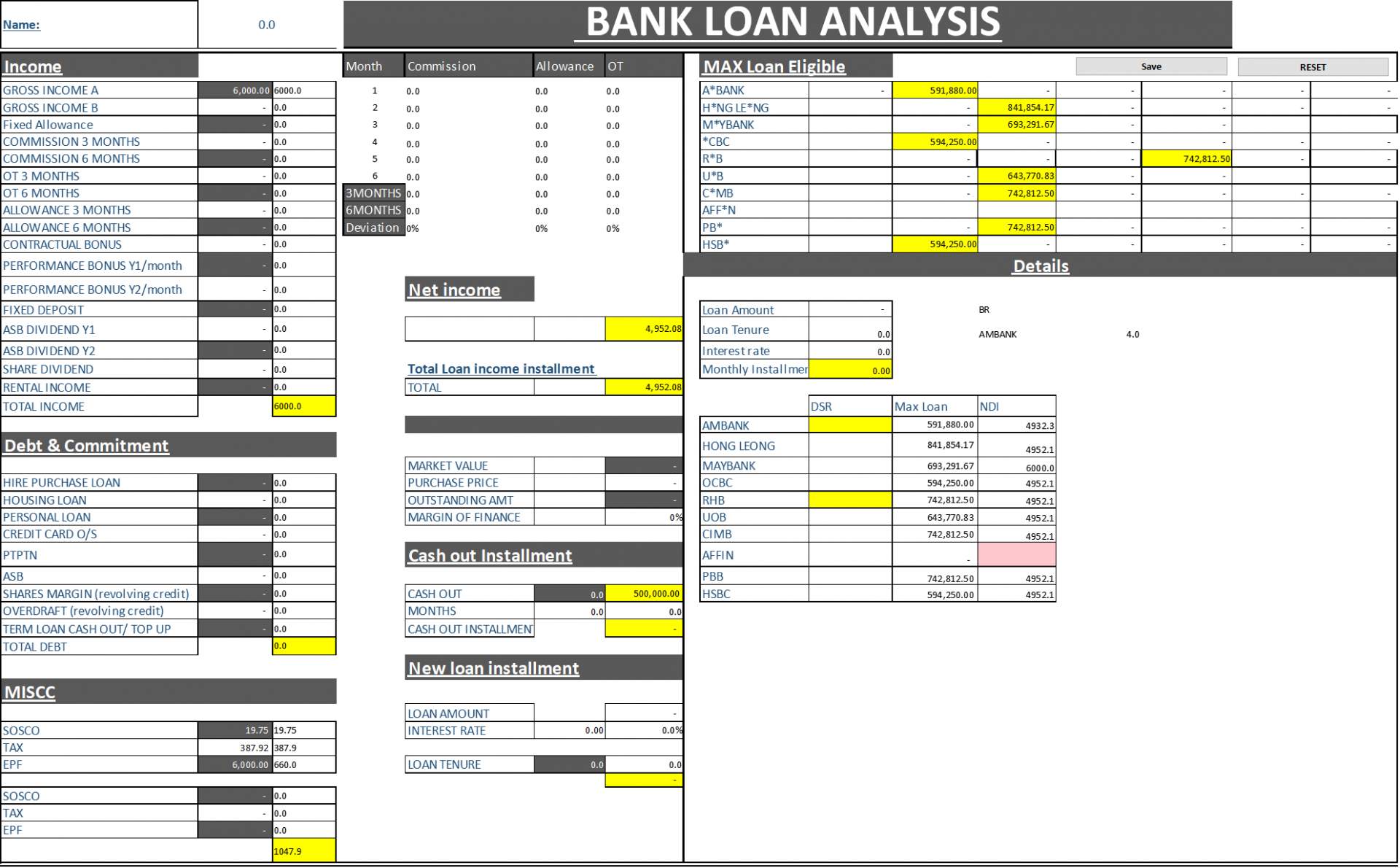

1. Based on the details given by you, Your max loan eligibility for each bank is as follow:

Bank Rm

A*BANK 328,078.67

H*NG LE*NG 539,285.33

M*YBANK 294,013.73

*CBC 352,816.48

R*B 309,338.33

U*B 352,816.48

C*MB 511,850.00

AFF*N -

PB* 511,850.00

HSB* 352,816.48

2. However, no ccris, it's subjective. If could show high saving $$$ in her account, there's a chance for 90% approval, else might drop to 80% margin of finance.

QUOTE(jordanseow @ Apr 16 2017, 04:34 PM)

Hi guys ,

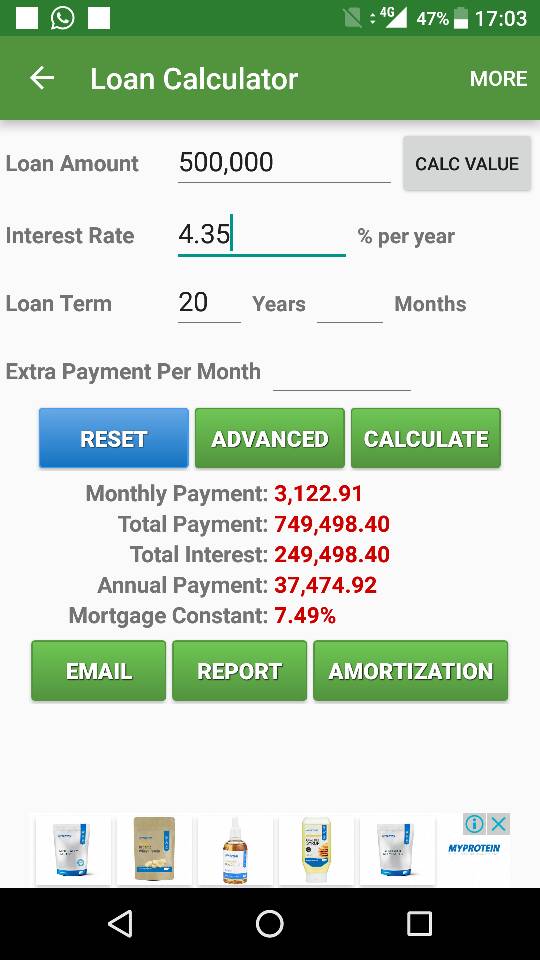

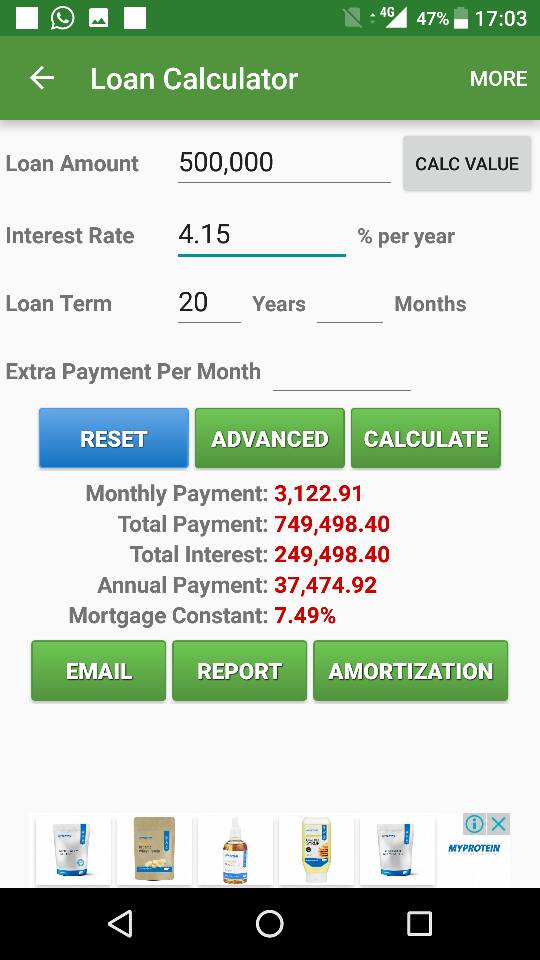

i want to loan a mortgage loan around 590K

1)I am struggling about whether choose OCBC or Maybank to apply the loan

2) normally loan more than 500K , ocbc or maybank provide better offer ?

Net income : RM3900 after epf

No commitment at all.

No car loan , no cc outstanding.

i want to loan a mortgage loan around 590K

1)I am struggling about whether choose OCBC or Maybank to apply the loan

2) normally loan more than 500K , ocbc or maybank provide better offer ?

Net income : RM3900 after epf

No commitment at all.

No car loan , no cc outstanding.

QUOTE(jordanseow @ Apr 16 2017, 04:49 PM)

I just finish my car loan last year 2016 August with pbb car loan.

Yeah I have saving around RM200K , the house value is 760K, so I planning to throw 170-180K as my first downpayment .

29 this year , working sdn bhd. This year bonus is 2 month. Working with this company 4 years already

Dear jordanseow,Yeah I have saving around RM200K , the house value is 760K, so I planning to throw 170-180K as my first downpayment .

29 this year , working sdn bhd. This year bonus is 2 month. Working with this company 4 years already

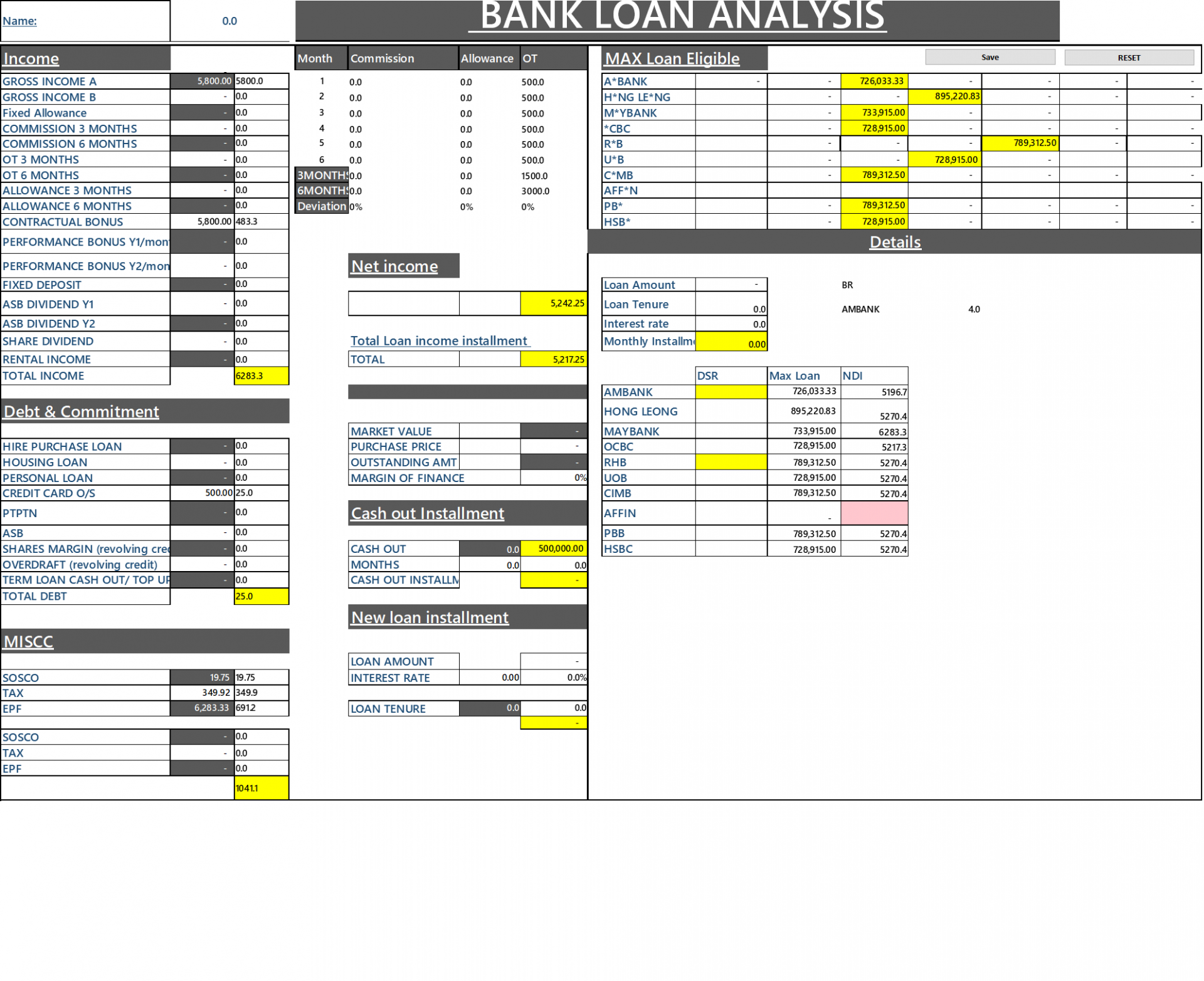

1. Based on the details given by you, Your max loan eligibility for each bank is as follow:

Bank Rm

A*BANK 404,543.60

H*NG LE*NG 576,460.93

M*YBANK 339,094.67

*CBC 406,913.60

R*B 508,642.00

U*B 440,823.07

C*MB 508,642.00

AFF*N -

PB* 508,642.00

HSB* 406,913.60

Things to take note of based onmy max loan calculation

" -The best bank to get the highest loan would be HLBB . However, each bank has it's own ball game

Different bank will calculate your income and debt accordingly based on each bank's different policy. Hence,

I would need to do a due diligence on your profile before suggesting the best bank to proceed with."

" - I would need to check you CCRIS, CTOS and income documentation before giving you any assurance.

If everything goes fine, 90% shouldn't be a problem for you."

2. above haven't added your bonus yet.

3. YOu have high saving, that will be a good credit score boost

4. Why don't you try other bank than the 2 banks you mentioned?

Cheers mate

Quote

Quote

so sorry to hear this. Hopefully you'll get this sorted out soonest.

so sorry to hear this. Hopefully you'll get this sorted out soonest. 0.1583sec

0.1583sec

0.60

0.60

7 queries

7 queries

GZIP Disabled

GZIP Disabled