Nov 1 2010, 01:16 AM

Nov 1 2010, 01:16 AM

QUOTE(ajau @ Nov 1 2010, 12:46 AM)

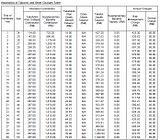

I already put the tabaru' for Takaful Health TH400 in my earlier post. I put it again here:

And this is insurance charges for PHL400

To get more detail, you better go visit a Pru agent. You can get more clear picture and better explanation on your query. For you

For your info, PRUlink One is a new ILP product from Prudential. Has been in the market since 16/08/2010

There are lots of PRUlink version and Medical Card (was known as PMM), going back to Nov 98.

Starting PMM3 (01/10/2003), there is an introduction of co-insurance

Starting PMM4 (09/04/2007), can opt for new rider to extend coverage until 80 years old

Starting PMM5 (15/10/2008), Prudential medical card starting having a minimum of RM500k lifetime limit. Previously the maximum lifetime limit was RM450k

PRUhealth was introduced on 08/06/2009 with an introduction of No Claim Bonus. Can opt to cover until 100 years old. Can opt for Annual Limit Waiver (No annual limit)

Hope this clarify some of your concern.

Added on November 1, 2010, 12:50 am

PRUlady still available.

You can have most of PRUlady benefit to be attached to PRUlink One (via PRUessential lady rider)

Added on November 1, 2010, 1:01 am

The idea is there.

But the actual medical card cost is not RM4582 (based on current charges). The cost is RM2000 when you are 53 years old (refer my posted table for PHL400). So the balance RM274 (RM 2000 - RM1726) will be deduct from your units (aka unit trust as MNet refer).

If you do not have enough units, you can top up your premium just like that without increasing any other benefit when you are 53 years old. So your annual premium got additional RM 274.

You may not have enough units if (but not limited to):

1. You are selling your units

2. Your unit's price at that time is very low compare earlier to purchase price

There are few to overcome unit price lower compare to purchase price.

1. Switch fund to bond fund. Bond fund usually will not be negative.

2. Sell the units while it high and you keep it in saving that will not reduce its value.

btw, i can't see till age 53..and how come from SS is 4k ++??

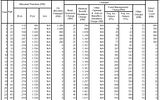

And this is insurance charges for PHL400

To get more detail, you better go visit a Pru agent. You can get more clear picture and better explanation on your query. For you

For your info, PRUlink One is a new ILP product from Prudential. Has been in the market since 16/08/2010

There are lots of PRUlink version and Medical Card (was known as PMM), going back to Nov 98.

Starting PMM3 (01/10/2003), there is an introduction of co-insurance

Starting PMM4 (09/04/2007), can opt for new rider to extend coverage until 80 years old

Starting PMM5 (15/10/2008), Prudential medical card starting having a minimum of RM500k lifetime limit. Previously the maximum lifetime limit was RM450k

PRUhealth was introduced on 08/06/2009 with an introduction of No Claim Bonus. Can opt to cover until 100 years old. Can opt for Annual Limit Waiver (No annual limit)

Hope this clarify some of your concern.

Added on November 1, 2010, 12:50 am

PRUlady still available.

You can have most of PRUlady benefit to be attached to PRUlink One (via PRUessential lady rider)

Added on November 1, 2010, 1:01 am

The idea is there.

But the actual medical card cost is not RM4582 (based on current charges). The cost is RM2000 when you are 53 years old (refer my posted table for PHL400). So the balance RM274 (RM 2000 - RM1726) will be deduct from your units (aka unit trust as MNet refer).

If you do not have enough units, you can top up your premium just like that without increasing any other benefit when you are 53 years old. So your annual premium got additional RM 274.

You may not have enough units if (but not limited to):

1. You are selling your units

2. Your unit's price at that time is very low compare earlier to purchase price

There are few to overcome unit price lower compare to purchase price.

1. Switch fund to bond fund. Bond fund usually will not be negative.

2. Sell the units while it high and you keep it in saving that will not reduce its value.

This post has been edited by [f]ireZz[kf]: Nov 1 2010, 01:24 AM

Quote

Quote 1.0550sec

1.0550sec

0.55

0.55

7 queries

7 queries

GZIP Disabled

GZIP Disabled