Oct 28 2010, 05:33 PM

Oct 28 2010, 05:33 PM

QUOTE(MNet @ Oct 28 2010, 05:01 PM)

Let say i take TH400 plan and now i'm 23 yr old.

So i will still pay RM1813 when I at age 50 ?

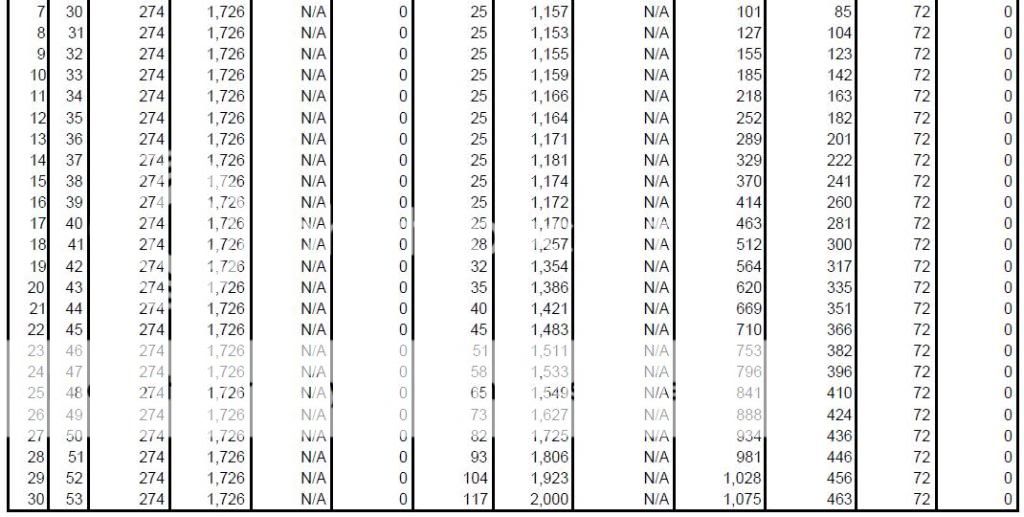

http://flare.me/images/7s0o7alv.jpg

Yup. You still pay RM1813 p.a. at age 50 even at age 70 - provided that there is enough fund in your account to pay for Takaful Health Tabaru'.So i will still pay RM1813 when I at age 50 ?

http://flare.me/images/7s0o7alv.jpg

Added on October 28, 2010, 5:36 pm

QUOTE(raph @ Oct 28 2010, 05:21 PM)

Nope,

Its RM4812 (because of next birthday, you have to pay for age 51). Its a age-band, not level premium

thanks

raph. You are wrong. The contribution is based on entry age. Not at your current age.Its RM4812 (because of next birthday, you have to pay for age 51). Its a age-band, not level premium

thanks

There is different between contribution and tabaru'. The tabaru' is based on your current age - which is the real charges for having the medical card

Added on October 28, 2010, 5:42 pm

QUOTE(MNet @ Oct 28 2010, 05:26 PM)

I find it hard to get such quotation at the website of insurance company.

Usually you cannot get quotation from website of insurance company. You need to get from an agent especially with the product that can be customized as per your need. From the discussion with the agent, and from the fact finding about yourself, the agent will propose or you can discuss what kind of protection that you need.What you can get from the website usually the premium or contribution of certain benefit.

If you want a quotation from Prudential or PruBSN, you can get it from me. Don't worry. No commitment. Let me know your birthday, smoking status, gender and probably your email address so I can email to you. You can pm me your detail. If you can specify what kind of benefit you want and your budget that will be better.

This post has been edited by ajau: Oct 28 2010, 05:42 PM

Quote

Quote

0.0411sec

0.0411sec

0.58

0.58

7 queries

7 queries

GZIP Disabled

GZIP Disabled