Beli rumah 35k bayar 17 thn balance masih 23k lagi

|

|

Apr 21 2025, 06:40 AM, updated 8 months ago Apr 21 2025, 06:40 AM, updated 8 months ago

Show posts by this member only | IPv6 | Post

#1

|

Senior Member

3,562 posts Joined: Sep 2005 From: Shenzhen Bahru |

I think the math checks out no?

|

Quote

Quote|

|

|

|

|

Apr 21 2025, 06:56 AM

Show posts by this member only | Post

#2

|

Moderator

9,275 posts Joined: Jan 2005 From: KL. Best place in Malaysia. Nuff said |

QUOTE(knwong @ Apr 21 2025, 06:40 AM) I think the math checks out no? interest tak masuk? lordgamer3, Quazacolt, and 4 others liked this post

|

|

|

Apr 21 2025, 06:59 AM

Show posts by this member only | Post

#3

|

|

Junior Member

535 posts Joined: Apr 2012 |

They dont know 70:30. But suprising withdraw 11k kwsp still left so much balance, he didnt instruct the bank to allocate to pay principle. lordgamer3, MasBoleh!, and 3 others liked this post

|

|

|

Apr 21 2025, 07:12 AM

Show posts by this member only | IPv6 | Post

#4

|

|

Junior Member

323 posts Joined: Sep 2022 |

LOL at the comments. Say cannot have interest. Then can buy ASNB and expect untung

|

|

|

Apr 21 2025, 07:14 AM

Show posts by this member only | Post

#5

|

Junior Member

189 posts Joined: Jan 2009 |

Ehh. Kamu kena bayar bank interest. Macam pinjam 35k then bayar 35k Kah? kylehudsons94, lordgamer3, and 1 other liked this post

|

|

|

Apr 21 2025, 07:16 AM

Show posts by this member only | IPv6 | Post

#6

|

Junior Member

93 posts Joined: Jan 2011 |

Rumah 35k ??

|

|

|

|

|

|

Apr 21 2025, 07:20 AM

Show posts by this member only | IPv6 | Post

#7

|

Senior Member

544 posts Joined: Aug 2007 |

what kind of rumah 35k i take 2 pay cash Imbi Plaza Lot 1.28 liked this post

|

|

|

Apr 21 2025, 07:25 AM

Show posts by this member only | Post

#8

|

|

Senior Member

2,115 posts Joined: Apr 2013 |

is like that lo, last time help my dad pay for the 42k flat, montly pay 300, after 10 years already paid 30k+, but still have 30k to pay off after 10 years. QUOTE(lahart @ Apr 21 2025, 07:16 AM) Rumah 35k ?? low cost flat 20 years ago is that price.This post has been edited by anakkk: Apr 21 2025, 07:25 AM yunxiangsgh liked this post

|

|

|

Apr 21 2025, 07:29 AM

Show posts by this member only | Post

#9

|

Senior Member

1,374 posts Joined: Feb 2016 From: Milky Way |

That’s why full flexi housing loan was best, ayam clear 30yrs loan in 7 years.

|

|

|

Apr 21 2025, 07:39 AM

Show posts by this member only | IPv6 | Post

#10

|

Senior Member

4,357 posts Joined: Oct 2010 From: KL |

*removed*

This post has been edited by cempedaklife: Apr 21 2025, 07:41 AM |

|

|

Apr 21 2025, 08:05 AM

Show posts by this member only | IPv6 | Post

#11

|

Senior Member

4,403 posts Joined: Jan 2007 From: Johor Bahru |

When sign agreement and bank loan hentam Signature only is it?

|

|

|

Apr 21 2025, 08:08 AM

|

Junior Member

933 posts Joined: Jul 2005 |

QUOTE(iGamer @ Apr 21 2025, 07:29 AM) That’s why full flexi housing loan was best, ayam clear 30yrs loan in 7 years. what difference full flexi and semi flexi? |

|

|

Apr 21 2025, 08:13 AM

|

Junior Member

257 posts Joined: Dec 2008 From: Malaysia |

hmmm, is a common thing -- the ratio like 20% to principal, while 70% to interest -- correct me if i am wrong, and slowly increase the 20% to like ? finish interest hahaha  lordgamer3 liked this post

|

|

|

|

|

|

Apr 21 2025, 08:15 AM

|

Junior Member

70 posts Joined: Aug 2014 |

kesimpulan: mathematic gagal

|

|

|

Apr 21 2025, 08:17 AM

Show posts by this member only | IPv6 | Post

#15

|

Senior Member

4,060 posts Joined: Dec 2007 From: クアラルンプール > 日本 |

Bayar Bulan only Rm200....WTF.....Rm150 are bank intrest...Rm50 are house Installment.....Rm50 per month..you pay 17 years sure still kanasai.... mudkipryan94 and ktek liked this post

|

|

|

Apr 21 2025, 08:19 AM

|

All Stars

17,021 posts Joined: Jan 2005 |

QUOTE(azbro @ Apr 21 2025, 08:05 AM) When sign agreement and bank loan hentam Signature only is it? B40 don't no math la. mudkipryan94, Quazacolt, and 3 others liked this post

|

|

|

Apr 21 2025, 08:23 AM

|

Senior Member

1,759 posts Joined: Mar 2007 From: _|_ |

QUOTE(ozak @ Apr 21 2025, 08:19 AM) B40 don't no math la. B40 mindset is expect loan 30 years, but finish pay in 10 years with minimum installment. if more, then meroyan. |

|

|

Apr 21 2025, 08:25 AM

Show posts by this member only | IPv6 | Post

#18

|

Senior Member

1,774 posts Joined: Nov 2007 From: Planet Earth |

I wish I can find a house in kl with that price.

|

|

|

Apr 21 2025, 08:30 AM

|

Junior Member

469 posts Joined: Sep 2009 From: under your bed |

you can check wif bank for clarification no?

|

|

|

Apr 21 2025, 08:31 AM

Show posts by this member only | IPv6 | Post

#20

|

Junior Member

140 posts Joined: Jul 2007 From: Puchong |

bank is just legal ah long

interest cekik darah |

|

|

Apr 21 2025, 08:32 AM

Show posts by this member only | IPv6 | Post

#21

|

|

Senior Member

3,562 posts Joined: Sep 2005 From: Shenzhen Bahru |

QUOTE(RegentCid @ Apr 21 2025, 08:17 AM) Bayar Bulan only Rm200....WTF.....Rm150 are bank intrest...Rm50 are house Installment.....Rm50 per month..you pay 17 years sure still kanasai.... If based on your RM50 principle payment for 17 years + the guy already dump 11k EPF into his loan…the guy should left with 13k principle left to clear lordgamer3 liked this post

|

|

|

Apr 21 2025, 08:34 AM

|

Senior Member

1,045 posts Joined: Jan 2003 From: gombak, subang, setapak, canberra, |

tu baru bayar interest kot..

|

|

|

Apr 21 2025, 08:37 AM

Show posts by this member only | IPv6 | Post

#23

|

Senior Member

3,642 posts Joined: Jul 2014 |

This kind of ppl, calling them maths gagal is an understatement. More like otak gagal

|

|

|

Apr 21 2025, 08:37 AM

|

|

Junior Member

70 posts Joined: Aug 2014 |

QUOTE(smallcrab @ Apr 21 2025, 08:31 AM) bank is just legal ah long tolong rekomen kalau ade org lain yg sanggup pinjam 500k dan bayar ansuran 30thn.interest cekik darah tqvm |

|

|

Apr 21 2025, 08:38 AM

Show posts by this member only | IPv6 | Post

#25

|

Senior Member

2,256 posts Joined: Feb 2012 |

Late payment, compounded late payment interest

Owed fire Insurance for years Malaysia, even 30+ still think like 6 years old |

|

|

Apr 21 2025, 08:39 AM

|

Senior Member

2,402 posts Joined: Jun 2007 |

not even worth a facepalm. there's many of those out there.

moving along now... |

|

|

Apr 21 2025, 08:40 AM

Show posts by this member only | IPv6 | Post

#27

|

Junior Member

752 posts Joined: Jun 2012 |

Nasib bail kurang bkan tambah 😂

|

|

|

Apr 21 2025, 08:41 AM

Show posts by this member only | IPv6 | Post

#28

|

Senior Member

5,614 posts Joined: Jun 2006 From: Cyberjaya, Shah Alam, Ipoh |

35k loan i assume if loan 30 years gonna end up pay 2.5 times of the total house price.

87.5k total if you pay on time. |

|

|

Apr 21 2025, 08:42 AM

|

|

Senior Member

1,374 posts Joined: Feb 2016 From: Milky Way |

QUOTE(soul78 @ Apr 21 2025, 08:08 AM) what difference full flexi and semi flexi? Full flexi u can take out money or pay extra whenever u want, no need inform bank in advance.The way my previous full flexi work is I just dump all my salary into the current account, the balance in current account will offset the loan principal automatically. I can withdraw from this current account any time or any amount as I wish. That way your uninvested money will always work for you to reduce loan interest. Even when your deposit already fully cover the loan balance, it’s up to you whether u wish to officially clear the loan or just leave it as is (loan still exist but zero interest charged). |

|

|

Apr 21 2025, 08:43 AM

Show posts by this member only | IPv6 | Post

#30

|

Junior Member

76 posts Joined: Jun 2019 |

that's y must watch videos cara orang cina beli rumah by FF.

|

|

|

Apr 21 2025, 08:45 AM

Show posts by this member only | IPv6 | Post

#31

|

Junior Member

994 posts Joined: May 2010 From: Cheras For PPL to Live 1 |

QUOTE(lahart @ Apr 21 2025, 07:16 AM) Rumah 35k ?? Like some1 comment.Also back then 25 years alot landed double storeh at cheras/kl area below 50k only |

|

|

Apr 21 2025, 08:46 AM

|

|

Senior Member

2,672 posts Joined: Sep 2006 |

Put signatures on so many papers and yet don't understand a thing. So many of them

|

|

|

Apr 21 2025, 08:47 AM

Show posts by this member only | IPv6 | Post

#33

|

Senior Member

5,974 posts Joined: Jan 2003 From: KL, Malaysia |

QUOTE(Manuk1188 @ Apr 21 2025, 08:13 AM) hmmm, is a common thing -- the ratio like 20% to principal, while 70% to interest -- correct me if i am wrong, and slowly increase the 20% to like ? finish interest hahaha Your interest is based on how much you owe, after settle interest, remaining installment goes to principal.In the beginning it appears all installment went to interest cause the amount you owe in beginning is high. If you park cash into loan 100%, your interest is 0. |

|

|

Apr 21 2025, 08:48 AM

|

|

Moderator

6,181 posts Joined: Oct 2004 |

QUOTE(lawliet88 @ Apr 21 2025, 08:45 AM) Like some1 comment. cannot be 25 years.Also back then 25 years alot landed double storeh at cheras/kl area below 50k only in 1990s cheras/ampang area still around 70k to 100k. in 2000s norm is around 200k. in 2010 it is around 300k in 2020s it become 500k and above. it has be 40 years before, then maybe 35k |

|

|

Apr 21 2025, 08:48 AM

Show posts by this member only | IPv6 | Post

#35

|

Junior Member

327 posts Joined: Nov 2008 |

QUOTE(ifourtos @ Apr 21 2025, 08:38 AM) Late payment, compounded late payment interest This make sense.Owed fire Insurance for years Malaysia, even 30+ still think like 6 years old There may be yearly fire insurance auto renewal + other additional insurance which the homeowner didn't pay extra and let it park under the loan. Another things is MRTA/MLTA which add-up all the loan amount. No wonder FinancialFaiz pissed-off with this kind of news. Always blame banks but not the loantaker ownself. All his effort to educate ppl about loans like throwing water onto the floor. |

|

|

Apr 21 2025, 08:50 AM

Show posts by this member only | IPv6 | Post

#36

|

|

Senior Member

3,562 posts Joined: Sep 2005 From: Shenzhen Bahru |

QUOTE(ifourtos @ Apr 21 2025, 08:38 AM) Late payment, compounded late payment interest Ok late payment makes a lot sense thenOwed fire Insurance for years Malaysia, even 30+ still think like 6 years old |

|

|

Apr 21 2025, 08:53 AM

|

|

Junior Member

171 posts Joined: Dec 2006 |

QUOTE(kons @ Apr 21 2025, 08:48 AM) cannot be 25 years. the 35K is likely refer to low cost apartmentin 1990s cheras/ampang area still around 70k to 100k. in 2000s norm is around 200k. in 2010 it is around 300k in 2020s it become 500k and above. it has be 40 years before, then maybe 35k |

|

|

Apr 21 2025, 08:54 AM

|

Junior Member

900 posts Joined: Oct 2009 |

QUOTE(iGamer @ Apr 21 2025, 07:29 AM) That’s why full flexi housing loan was best, ayam clear 30yrs loan in 7 years. how much was your loan? |

|

|

Apr 21 2025, 08:56 AM

|

|

Junior Member

171 posts Joined: Dec 2006 |

QUOTE(iGamer @ Apr 21 2025, 08:42 AM) Full flexi u can take out money or pay extra whenever u want, no need inform bank in advance. old flexi loan can have zero interest if money dumped =/> loan balance, new flexi loan will only offset 70% loan balance as bank realized the disadvantage of old flexi loanThe way my previous full flexi work is I just dump all my salary into the current account, the balance in current account will offset the loan principal automatically. I can withdraw from this current account any time or any amount as I wish. That way your uninvested money will always work for you to reduce loan interest. Even when your deposit already fully cover the loan balance, it’s up to you whether u wish to officially clear the loan or just leave it as is (loan still exist but zero interest charged). |

|

|

Apr 21 2025, 08:58 AM

Show posts by this member only | IPv6 | Post

#40

|

|

Senior Member

4,060 posts Joined: Dec 2007 From: クアラルンプール > 日本 |

QUOTE(kons @ Apr 21 2025, 07:48 AM) cannot be 25 years. About 30 Years ago. in 1990s cheras/ampang area still around 70k to 100k. in 2000s norm is around 200k. in 2010 it is around 300k in 2020s it become 500k and above. it has be 40 years before, then maybe 35k Rumah Low Cost during Mahathir time. My House at Lorong Nipah 6. Lorong Nipah 7 - 15 are those Rm35k low cost house. My Father that time also interest to buy but not qualified, his Salary was too high. |

|

|

Apr 21 2025, 09:00 AM

Show posts by this member only | IPv6 | Post

#41

|

Senior Member

3,703 posts Joined: Oct 2005 |

QUOTE(JasonthegreatTWO @ Apr 21 2025, 07:12 AM) LOL at the comments. Say cannot have interest. Then can buy ASNB and expect untung Lol I immediately think about this because interest = haram. Ku9 liked this post

|

|

|

Apr 21 2025, 09:00 AM

Show posts by this member only | IPv6 | Post

#42

|

Senior Member

1,360 posts Joined: Oct 2009 |

must be do not aware about the rate changes due to OPR and still paid with an old amount.

|

|

|

Apr 21 2025, 09:02 AM

|

Senior Member

1,523 posts Joined: Apr 2005 From: too far to see |

35k loan is definitely non flexi loan Aduhai Amortization chart definitely check out correctly And yes, he hasnt instruct bank to deduct principle, and maybe his term loan cant clear principle only https://www.calculator.net/amortization-cal...ulate#calresult This post has been edited by taitianhin: Apr 21 2025, 09:10 AM jessicakoh and eyerule liked this post

|

|

|

Apr 21 2025, 09:02 AM

|

Senior Member

622 posts Joined: Jun 2007 |

QUOTE(a13solut3 @ Apr 21 2025, 08:23 AM) B40 mindset is expect loan 30 years, but finish pay in 10 years with minimum installment. if more, then meroyan. you are wrong. true B40 mindset is take loan already then don't pay back. then when bank/ahlong come and collect money or confiscate assets, they cry father cry mother then ask for a certain religious group to help nego  |

|

|

Apr 21 2025, 09:03 AM

Show posts by this member only | IPv6 | Post

#45

|

|

Senior Member

3,562 posts Joined: Sep 2005 From: Shenzhen Bahru |

QUOTE(theozis @ Apr 21 2025, 08:56 AM) old flexi loan can have zero interest if money dumped =/> loan balance, new flexi loan will only offset 70% loan balance as bank realized the disadvantage of old flexi loan In the end bank still smarter |

|

|

Apr 21 2025, 09:03 AM

Show posts by this member only | IPv6 | Post

#46

|

|

Senior Member

3,703 posts Joined: Oct 2005 |

QUOTE(azbro @ Apr 21 2025, 08:05 AM) When sign agreement and bank loan hentam Signature only is it? This is the same gang as the PTPTN whom borrow and don't pay.... |

|

|

Apr 21 2025, 09:03 AM

|

Senior Member

2,491 posts Joined: Dec 2004 From: initrd |

QUOTE(JasonthegreatTWO @ Apr 21 2025, 07:12 AM) LOL at the comments. Say cannot have interest. Then can buy ASNB and expect untung Interest in another way.Loop hole. Topkek ariba riba anggallelelele |

|

|

Apr 21 2025, 09:09 AM

|

|

Senior Member

1,374 posts Joined: Feb 2016 From: Milky Way |

QUOTE(theozis @ Apr 21 2025, 08:56 AM) old flexi loan can have zero interest if money dumped =/> loan balance, new flexi loan will only offset 70% loan balance as bank realized the disadvantage of old flexi loan Too bad for new borrower, that’s why ayam said full flexi WAS the best.  |

|

|

Apr 21 2025, 09:15 AM

|

|

Newbie

3 posts Joined: Jun 2017 |

QUOTE(lawliet88 @ Apr 21 2025, 08:45 AM) Like some1 comment. Also back then 25 years alot landed double storeh at cheras/kl area below 50k only QUOTE(kons @ Apr 21 2025, 08:48 AM) cannot be 25 years. Dad bought double story house for around 60k-70k in the early 90s.in 1990s cheras/ampang area still around 70k to 100k. in 2000s norm is around 200k. in 2010 it is around 300k in 2020s it become 500k and above. it has be 40 years before, then maybe 35k Can't say exactly where, but its a 15-20 drive to KLCC if there is zero jam (impossible nowadays la). The houses in my area, if you tried to buy second hand are worth 500k to 1 mil. No joke. 60k-70k jump to 500k-1 mil. QUOTE(kons @ Apr 21 2025, 08:48 AM) cannot be 25 years. Also, like what happened with these years. 70k to 200k+ is an insane jump for 10 years.in 1990s cheras/ampang area still around 70k to 100k. in 2000s norm is around 200k. This post has been edited by gamehype: Apr 21 2025, 09:23 AM |

|

|

Apr 21 2025, 09:16 AM

Show posts by this member only | IPv6 | Post

#50

|

Junior Member

221 posts Joined: Jan 2019 From: Earth |

That is why financial literacy very important...

|

|

|

Apr 21 2025, 09:24 AM

Show posts by this member only | IPv6 | Post

#51

|

Junior Member

346 posts Joined: May 2005 |

When BLR/interest rate turun, need to apply to decrease interest rate with bank. When naik, bank send you letter stated they will increase the loan repayment.

So everytime you need to apply to decrease in accordance to BLR/interest rate. Is this apply to all loan types? |

|

|

Apr 21 2025, 09:25 AM

Show posts by this member only | IPv6 | Post

#52

|

Junior Member

70 posts Joined: Nov 2014 From: The 10th Dimension |

QUOTE(Ickythump @ Apr 21 2025, 07:20 AM) what kind of rumah 35k i take 2 pay cash low cost flat ler bro...my father has 2, both priced 30+k 20 years ago. now one 100k kekpot but the other one....bulan2 rm700 sewa i mean rm700 for a fucking cage is kinda ok...but i tell ya, these "low cost" ones sure byk porblem and very slow one to sell cost need approval to sell from gov that includes "low cost terrace" built years ago max_cavalera liked this post

|

|

|

Apr 21 2025, 09:25 AM

|

|

Moderator

6,181 posts Joined: Oct 2004 |

QUOTE(gamehype @ Apr 21 2025, 09:15 AM) Dad bought double story house for around 60k-70k in the early 90s. now the houses here likely around 700k ~ 800k.Can't say exactly where, but its a 15-20 drive to KLCC if there is zero jam (impossible nowadays la). The houses in my area, if you tried to buy second hand are worth 500k to 1 mil. No joke. 60k-70k jump to 500k-1 mil. Also, like what happened with these years. 70k to 200k+ is an insane jump for 10 years. mine corner lot should be around 1m plus |

|

|

Apr 21 2025, 09:29 AM

|

Junior Member

150 posts Joined: Oct 2009 From: Klang, Selangor D.E Status: Work Everyday |

Okla, baik lagi bayar Rm300 until hhnngghh, then get 50K

|

|

|

Apr 21 2025, 09:31 AM

Show posts by this member only | IPv6 | Post

#55

|

Senior Member

2,834 posts Joined: Jul 2006 From: here |

QUOTE(ifourtos @ Apr 21 2025, 09:38 AM) Late payment, compounded late payment interest Coz expect to be treated like 6 year old. Owed fire Insurance for years Malaysia, even 30+ still think like 6 years old want something?... simply cry and throw tantrum. ifourtos liked this post

|

|

|

Apr 21 2025, 09:31 AM

|

Junior Member

763 posts Joined: Jan 2003 |

QUOTE(gamehype @ Apr 21 2025, 09:15 AM) Dad bought double story house for around 60k-70k in the early 90s. I always feel property was never cheap or affordable in any era. For majority, yes can afford but not like the kind that can afford 10-20 properties kind. Can't say exactly where, but its a 15-20 drive to KLCC if there is zero jam (impossible nowadays la). The houses in my area, if you tried to buy second hand are worth 500k to 1 mil. No joke. 60k-70k jump to 500k-1 mil. Also, like what happened with these years. 70k to 200k+ is an insane jump for 10 years. Thats y most majority of us don't inherit 10-20 properties hahahahaa. If it was that affordable, majority of us would be sitting on 20-30 properties from our grandparents, then our parents etc. This post has been edited by cms: Apr 21 2025, 09:32 AM |

|

|

Apr 21 2025, 09:34 AM

Show posts by this member only | IPv6 | Post

#57

|

Senior Member

1,943 posts Joined: Apr 2005 |

When there's 120iq people there are also the 80iq people that we rarely mention, now we are looking at one.

|

|

|

Apr 21 2025, 09:35 AM

Show posts by this member only | IPv6 | Post

#58

|

Junior Member

569 posts Joined: Jul 2007 |

B40 fail in math.

Pergi tengok building bank yang beasr dan cangih tu. You faham wang dah pergi mana. RM200 per month, better than bayar sewa. |

|

|

Apr 21 2025, 09:36 AM

|

Junior Member

213 posts Joined: Jan 2006 From: kuala lumpur |

house interest is pay 2house price one

|

|

|

Apr 21 2025, 09:38 AM

|

Senior Member

1,709 posts Joined: Jan 2003 From: Kedah Khap Khoun Khap (4K) |

QUOTE(kcchong2000 @ Apr 21 2025, 07:14 AM) Ehh. Kamu kena bayar bank interest. this is the way.Macam pinjam 35k then bayar 35k Kah? no riba. no interest. fair & square. ayam sure you also want this kind loan scheme yes? |

|

|

Apr 21 2025, 09:38 AM

|

|

Junior Member

66 posts Joined: Jan 2011 |

Checks out.

It is frustrating, but Bank Negara and other banks are seriously worst than Arlong when it comes to House Loan, more than half of the loan period are majority you're paying the interests 1st, and because of that, the interests keep piling up because your principal only decrease only a small amount each year. This post has been edited by hteekay: Apr 21 2025, 09:41 AM |

|

|

Apr 21 2025, 09:41 AM

|

|

Junior Member

486 posts Joined: Dec 2013 |

Win win laa..bank get profit RM 50k..his house 17 years MV now how much? Must be more than 100k.

|

|

|

Apr 21 2025, 09:44 AM

|

|

Senior Member

1,922 posts Joined: Feb 2016 |

QUOTE(knwong @ Apr 21 2025, 06:40 AM) I think the math checks out no? Why never consult FF? |

|

|

Apr 21 2025, 09:47 AM

Show posts by this member only | IPv6 | Post

#64

|

Junior Member

216 posts Joined: Sep 2015 |

QUOTE(kons @ Apr 21 2025, 09:48 AM) cannot be 25 years. my father bought a subang condo unit for about ~30k during 1980s before construction, now if want to buy the same unit it's already ~250k in 1990s cheras/ampang area still around 70k to 100k. in 2000s norm is around 200k. in 2010 it is around 300k in 2020s it become 500k and above. it has be 40 years before, then maybe 35k if it's the terrance house / link house even worse, 70k~100k, now it's already at least 750k, some if refurbished fully can go to 1mil |

|

|

Apr 21 2025, 09:50 AM

|

Junior Member

535 posts Joined: Oct 2010 From: 4:44 am |

Don't complain bank itu ah long when you no money to buy house/car. Kalau capable fork out itu 35k sendiri.

House loan is mortgage amortisation. Masa sign loan document itu hentam sign saja? Topkek. |

|

|

Apr 21 2025, 09:51 AM

|

|

Junior Member

59 posts Joined: Mar 2011 |

pay loan for 17 years never once look at the bank statement

|

|

|

Apr 21 2025, 10:05 AM

Show posts by this member only | IPv6 | Post

#67

|

|

Junior Member

93 posts Joined: Jan 2011 |

QUOTE(chinteck79 @ Apr 21 2025, 09:51 AM) pay loan for 17 years never once look at the bank statement More like when sign loan agreement buta buta |

|

|

Apr 21 2025, 10:06 AM

|

|

Newbie

3 posts Joined: Jun 2017 |

QUOTE(cms @ Apr 21 2025, 09:31 AM) I always feel property was never cheap or affordable in any era. For majority, yes can afford but not like the kind that can afford 10-20 properties kind. No one talking about buying 10-20 properties.Thats y most majority of us don't inherit 10-20 properties hahahahaa. If it was that affordable, majority of us would be sitting on 20-30 properties from our grandparents, then our parents etc. But let just take my father example. He bought a double story house for 60k-70k in the 1990s The houses in my taman now is going for 500k to even 1 mil. That is a 10x increase in price. But has salary increase x10? I don't think sooo. This post has been edited by gamehype: Apr 21 2025, 10:20 AM nightzstar liked this post

|

|

|

Apr 21 2025, 10:08 AM

|

Junior Member

303 posts Joined: Aug 2005 |

QUOTE(hteekay @ Apr 21 2025, 09:38 AM) Checks out. yes and i am wondering why cant the bank negara instruct local banks to have 50% principal and 50% interest from the beginning until to the end. if cant 50/50 at least 40/60 lolIt is frustrating, but Bank Negara and other banks are seriously worst than Arlong when it comes to House Loan, more than half of the loan period are majority you're paying the interests 1st, and because of that, the interests keep piling up because your principal only decrease only a small amount each year. |

|

|

Apr 21 2025, 10:17 AM

Show posts by this member only | IPv6 | Post

#70

|

Junior Member

86 posts Joined: Jul 2006 |

tats y at least spm is important

|

|

|

Apr 21 2025, 10:19 AM

|

|

Newbie

3 posts Joined: Jun 2017 |

QUOTE(Zaryl @ Apr 21 2025, 09:38 AM) this is the way. You loan me RM100k now.no riba. no interest. fair & square. ayam sure you also want this kind loan scheme yes? I pay you back RM100k 50 years later. If you and me pass away, I ask my son to pay your son RM100k 50 years later  |

|

|

Apr 21 2025, 10:36 AM

|

Junior Member

336 posts Joined: Mar 2017 |

QUOTE(JasonthegreatTWO @ Apr 21 2025, 07:12 AM) LOL at the comments. Say cannot have interest. Then can buy ASNB and expect untung Naise one bruhhhhh  Nihonmaru liked this post

|

|

|

Apr 21 2025, 10:37 AM

|

Senior Member

2,162 posts Joined: Sep 2004 |

Banks are licensed ah longs kek

|

|

|

Apr 21 2025, 10:39 AM

|

|

Junior Member

336 posts Joined: Mar 2017 |

QUOTE(ifourtos @ Apr 21 2025, 08:38 AM) Late payment, compounded late payment interest That's how PuAS succeed in kelate Owed fire Insurance for years Malaysia, even 30+ still think like 6 years old  |

|

|

Apr 21 2025, 10:41 AM

|

|

Junior Member

88 posts Joined: Feb 2011 |

never check just blindly pay assuming its only 200 oer month without taking in the interest then blame the bank always salah orang

|

|

|

Apr 21 2025, 10:41 AM

|

|

Junior Member

336 posts Joined: Mar 2017 |

QUOTE(theozis @ Apr 21 2025, 08:56 AM) old flexi loan can have zero interest if money dumped =/> loan balance, new flexi loan will only offset 70% loan balance as bank realized the disadvantage of old flexi loan Ohh really??? That's sadding news. |

|

|

Apr 21 2025, 10:42 AM

Show posts by this member only | IPv6 | Post

#77

|

|

Junior Member

189 posts Joined: Jan 2009 |

QUOTE(Zaryl @ Apr 21 2025, 09:38 AM) this is the way. As if bank will do it lor.no riba. no interest. fair & square. ayam sure you also want this kind loan scheme yes? |

|

|

Apr 21 2025, 10:47 AM

|

|

Junior Member

336 posts Joined: Mar 2017 |

QUOTE(Zaryl @ Apr 21 2025, 09:38 AM) this is the way. Butbutbut ayam want high interest on FD juga.no riba. no interest. fair & square. ayam sure you also want this kind loan scheme yes? How ar? Bank get moneh from sky? This post has been edited by Ayambetul: Apr 21 2025, 10:48 AM |

|

|

Apr 21 2025, 10:48 AM

|

|

Senior Member

1,922 posts Joined: Feb 2016 |

QUOTE(bill11 @ Apr 21 2025, 10:08 AM) yes and i am wondering why cant the bank negara instruct local banks to have 50% principal and 50% interest from the beginning until to the end. if cant 50/50 at least 40/60 lol Min instalment ✅Longest tenure ✅ Binggung✅ Win liow lo This post has been edited by jojolicia: Apr 21 2025, 11:08 AM |

|

|

Apr 21 2025, 10:53 AM

|

Senior Member

975 posts Joined: Aug 2007 From: Lokap Polis |

11k masuk advance payment la tu or not yet disburse.

|

|

|

Apr 21 2025, 11:04 AM

|

|

Senior Member

1,709 posts Joined: Jan 2003 From: Kedah Khap Khoun Khap (4K) |

QUOTE(gamehype @ Apr 21 2025, 10:19 AM) You loan me RM100k now. I pay you back RM100k 50 years later. If you and me pass away, I ask my son to pay your son RM100k 50 years later QUOTE(Ayambetul @ Apr 21 2025, 10:47 AM) Butbutbut ayam want high interest on FD juga. I did ask this question to the anti Islamic Bank / anti riba dudes on FB & on TikTok.How ar? Bank get moneh from sky? i was labelled as kafir/munafiqun because I toyed with what has been written in the Quran. i asked them: which part is riba if i borrow RM100k then later payback exactly RM100k? But the loan repayment tenure is UP TO ME, for as long I try to fulfill the loan repayment. TROLOLOLOL. I really hate these anti riba hyprocytes. The only solution is Islamic Bank but they say it's backdoor riba. From which source will bank able to sustain/make profit you ask if borrow RM100k, payback RM100k? that one I don't care LOL. |

|

|

Apr 21 2025, 11:09 AM

|

|

Senior Member

3,562 posts Joined: Sep 2005 From: Shenzhen Bahru |

QUOTE(bill11 @ Apr 21 2025, 10:08 AM) yes and i am wondering why cant the bank negara instruct local banks to have 50% principal and 50% interest from the beginning until to the end. if cant 50/50 at least 40/60 lol Becareful what you wish for |

|

|

Apr 21 2025, 11:10 AM

|

|

Junior Member

336 posts Joined: Mar 2017 |

QUOTE(Zaryl @ Apr 21 2025, 11:04 AM) I did ask this question to the anti Islamic Bank / anti riba dudes on FB & on TikTok. Want anti riba kena borrow moneh from holier than thou peoplei was labelled as kafir/munafiqun because I toyed with what has been written in the Quran. i asked them: which part is riba if i borrow RM100k then later payback exactly RM100k? But the loan repayment tenure is UP TO ME, for as long I try to fulfill the loan repayment. TROLOLOLOL. I really hate these anti riba hyprocytes. The only solution is Islamic Bank but they say it's backdoor riba. From which source will bank able to sustain/make profit you ask if borrow RM100k, payback RM100k? that one I don't care LOL. Bebawang |

|

|

Apr 21 2025, 11:16 AM

|

|

Senior Member

1,288 posts Joined: Sep 2012 |

young time teacher ask to study math properly dont want...wanna become lalabeng mat rempit

grown up become bodo dunno calculate loan...amortization...knnmcb |

|

|

Apr 21 2025, 11:19 AM

Show posts by this member only | IPv6 | Post

#85

|

Senior Member

2,096 posts Joined: Oct 2007 |

-

This post has been edited by cmk96: Apr 21 2025, 11:26 AM |

|

|

Apr 21 2025, 11:20 AM

|

|

Senior Member

8,652 posts Joined: Sep 2005 From: lolyat |

Normal lah, 17 years ago at year 2008 probably housing loan interest around 5-6%, house 35k, 35 years loan instalment total RM84k.

For the first 10 years, majority of the instalment are serving the interest |

|

|

Apr 21 2025, 11:31 AM

|

Junior Member

295 posts Joined: Jun 2006 From: JB |

QUOTE(knwong @ Apr 21 2025, 06:40 AM) I think the math checks out no? too many people dont know how compound interest in home loans work. |

|

|

Apr 21 2025, 11:32 AM

|

|

Senior Member

3,562 posts Joined: Sep 2005 From: Shenzhen Bahru |

QUOTE(shadow_walker @ Apr 21 2025, 11:16 AM) young time teacher ask to study math properly dont want...wanna become lalabeng mat rempit Don’t remember calculating home loan is part of math classgrown up become bodo dunno calculate loan...amortization...knnmcb |

|

|

Apr 21 2025, 11:34 AM

Show posts by this member only | IPv6 | Post

#89

|

Senior Member

4,254 posts Joined: Nov 2011 |

this is why every month i see bank transaction for my house its damn tiok. i pay RM2.8k/mth, then interest RM2.1k/mth. so basically im only clearing RM700/mth in principal zzzz

thats why my pama back then offered to give me some cash to reduce the principal back then. i need to throw in more monies inside principal to reduce the interest ed  |

|

|

Apr 21 2025, 11:34 AM

Show posts by this member only | IPv6 | Post

#90

|

|

Junior Member

695 posts Joined: Nov 2010 |

35k can straight pay lump sum

|

|

|

Apr 21 2025, 11:35 AM

|

|

Senior Member

3,562 posts Joined: Sep 2005 From: Shenzhen Bahru |

QUOTE(marfccy @ Apr 21 2025, 11:34 AM) this is why every month i see bank transaction for my house its damn tiok. i pay RM2.8k/mth, then interest RM2.1k/mth. so basically im only clearing RM700/mth in principal zzzz Take their offer. Pay them interest is better than letting bank shareholders richthats why my pama back then offered to give me some cash to reduce the principal back then. i need to throw in more monies inside principal to reduce the interest ed |

|

|

Apr 21 2025, 11:38 AM

|

|

Junior Member

303 posts Joined: Aug 2005 |

QUOTE(jojolicia @ Apr 21 2025, 10:48 AM) Min instalment ✅ Where got min installment, the installment amount will be same, just the allocation for the principal is higher compare to lower as per current ratio. Longest tenure ✅ Binggung✅ Win liow lo secondly, bank can have tongkat for the longest period until when ? |

|

|

Apr 21 2025, 11:39 AM

Show posts by this member only | IPv6 | Post

#93

|

|

Senior Member

4,254 posts Joined: Nov 2011 |

QUOTE(knwong @ Apr 21 2025, 11:35 AM) Take their offer. Pay them interest is better than letting bank shareholders rich yeah but i feel damn bad la, like stealing their retirement money so i declined their offer last time. so now i just pay more every month so the principal reduce faster (but obviously not fast enough) |

|

|

Apr 21 2025, 11:41 AM

|

|

Senior Member

3,562 posts Joined: Sep 2005 From: Shenzhen Bahru |

QUOTE(marfccy @ Apr 21 2025, 11:39 AM) yeah but i feel damn bad la, like stealing their retirement money so i declined their offer last time. so now i just pay more every month so the principal reduce faster (but obviously not fast enough) Just ask them again. The fact they can offer it means they don't urgently need that money |

|

|

Apr 21 2025, 11:54 AM

|

|

Junior Member

763 posts Joined: Jan 2003 |

QUOTE(gamehype @ Apr 21 2025, 10:06 AM) No one talking about buying 10-20 properties. Yeah i get it. So lets find ways to make more money or just use less. Else it would be worst in the future.But let just take my father example. He bought a double story house for 60k-70k in the 1990s The houses in my taman now is going for 500k to even 1 mil. That is a 10x increase in price. But has salary increase x10? I don't think sooo. |

|

|

Apr 21 2025, 12:06 PM

Show posts by this member only | IPv6 | Post

#96

|

|

Junior Member

70 posts Joined: Nov 2014 From: The 10th Dimension |

QUOTE(iGamer @ Apr 21 2025, 08:42 AM) Full flexi u can take out money or pay extra whenever u want, no need inform bank in advance. So, example I use full flexi loan and buy a 300k house, I paid 30k dp and just need to have at least 270k in my current account. Then the loan interest will reduce a lot because I basically already have270k and can settle immediately or just leave it as it is?The way my previous full flexi work is I just dump all my salary into the current account, the balance in current account will offset the loan principal automatically. I can withdraw from this current account any time or any amount as I wish. That way your uninvested money will always work for you to reduce loan interest. Even when your deposit already fully cover the loan balance, it’s up to you whether u wish to officially clear the loan or just leave it as is (loan still exist but zero interest charged). |

|

|

Apr 21 2025, 12:11 PM

|

|

Junior Member

223 posts Joined: Dec 2006 |

masa sekolah minta belajar lebih .. tak nak.

pastu speaking pulak. dengki pada kawan yang speaking. salah siapa kalau tak pandai masa buat keputusan |

|

|

Apr 21 2025, 12:12 PM

|

|

Senior Member

1,374 posts Joined: Feb 2016 From: Milky Way |

QUOTE(FappyBird @ Apr 21 2025, 12:06 PM) So, example I use full flexi loan and buy a 300k house, I paid 30k dp and just need to have at least 270k in my current account. Then the loan interest will reduce a lot because I basically already have270k and can settle immediately or just leave it as it is? Yes, but from what I heard nowadays most banks no longer provide full flexi housing loan. The second best choice would be semi flexi loan (terms may differ among different banks, so must ask or read their terms clearly). |

|

|

Apr 21 2025, 12:14 PM

Show posts by this member only | IPv6 | Post

#99

|

Senior Member

1,534 posts Joined: Jul 2006 |

QUOTE(Zaryl @ Apr 21 2025, 12:04 PM) I did ask this question to the anti Islamic Bank / anti riba dudes on FB & on TikTok. Kek..nobody knows what is inside a stupid person mind..loli was labelled as kafir/munafiqun because I toyed with what has been written in the Quran. i asked them: which part is riba if i borrow RM100k then later payback exactly RM100k? But the loan repayment tenure is UP TO ME, for as long I try to fulfill the loan repayment. TROLOLOLOL. I really hate these anti riba hyprocytes. The only solution is Islamic Bank but they say it's backdoor riba. From which source will bank able to sustain/make profit you ask if borrow RM100k, payback RM100k? that one I don't care LOL. |

|

|

Apr 21 2025, 12:17 PM

Show posts by this member only | IPv6 | Post

#100

|

|

Junior Member

70 posts Joined: Nov 2014 From: The 10th Dimension |

QUOTE(iGamer @ Apr 21 2025, 12:12 PM) Yes, but from what I heard nowadays most banks no longer provide full flexi housing loan. The second best choice would be semi flexi loan (terms may differ among different banks, so must ask or read their terms clearly). Currently, mine was semi flexiI asked my banker and she said this is provided by bank side. Never asked me if I want what kind loan or what. I also forgot I got ask can change or not but I guess might just settle quickly after 3year limit. |

|

|

Apr 21 2025, 12:38 PM

|

|

Senior Member

1,374 posts Joined: Feb 2016 From: Milky Way |

QUOTE(FappyBird @ Apr 21 2025, 12:17 PM) Currently, mine was semi flexi U never compare different banks when taking housing loan? If compare sure need to ask for clarification. I asked my banker and she said this is provided by bank side. Never asked me if I want what kind loan or what. I also forgot I got ask can change or not but I guess might just settle quickly after 3year limit. Last time when I get different banks offer, MBB officer said my PBB full flexi not worth it as it charges RM10/month for the facility. But I did my calculations and it’s totally worth it for amount of interest I could save, and ultimately actually saved. Cannot just trust bank officer, they tokok just promote own bank only. |

|

|

Apr 21 2025, 12:41 PM

|

|

Junior Member

171 posts Joined: Dec 2006 |

QUOTE(sykz @ Apr 21 2025, 09:24 AM) When BLR/interest rate turun, need to apply to decrease interest rate with bank. When naik, bank send you letter stated they will increase the loan repayment. no, the BLR up or down is only impacted those flexi or semi flexi loan. the rate will be adjusted by bank automatically but bear in mind that some bank will not do it immediatelySo everytime you need to apply to decrease in accordance to BLR/interest rate. Is this apply to all loan types? there are some old loan typically before 2007 which is term loan that its interest rate is fixed. |

|

|

Apr 21 2025, 12:41 PM

Show posts by this member only | IPv6 | Post

#103

|

|

Junior Member

70 posts Joined: Nov 2014 From: The 10th Dimension |

QUOTE(iGamer @ Apr 21 2025, 12:38 PM) U never compare different banks when taking housing loan? If compare sure need to ask for clarification. It was all done through poorpety agent Last time when I get different banks offer, MBB officer said my PBB full flexi not worth it as it charges RM10/month for the facility. But I did my calculations and it’s totally worth it for amount of interest I could save, and ultimately actually saved. Cannot just trust bank officer, they tokok just promote own bank only. |

|

|

Apr 21 2025, 12:44 PM

|

|

Junior Member

171 posts Joined: Dec 2006 |

QUOTE(Ayambetul @ Apr 21 2025, 10:41 AM) Ohh really??? That's sadding news. As I know, it is applicable to most bank.anyway, please cross check with your bank. they shall provide the details. |

|

|

Apr 21 2025, 12:44 PM

|

|

Senior Member

1,374 posts Joined: Feb 2016 From: Milky Way |

QUOTE(FappyBird @ Apr 21 2025, 12:41 PM) It was all done through poorpety agent Aiyoyo if like that they probably push u to the bank with best commission to them instead of best bank offer…. |

|

|

Apr 21 2025, 12:45 PM

Show posts by this member only | IPv6 | Post

#106

|

Newbie

32 posts Joined: Jun 2011 |

QUOTE(JasonthegreatTWO @ Apr 21 2025, 07:12 AM) LOL at the comments. Say cannot have interest. Then can buy ASNB and expect untung Pay to me can.Pay to you cannot. Bestest liligen they said. |

|

|

Apr 21 2025, 12:47 PM

|

|

Junior Member

171 posts Joined: Dec 2006 |

QUOTE(FappyBird @ Apr 21 2025, 12:06 PM) So, example I use full flexi loan and buy a 300k house, I paid 30k dp and just need to have at least 270k in my current account. Then the loan interest will reduce a lot because I basically already have270k and can settle immediately or just leave it as it is? personal opinion is dont settle the flexi loan even have the money to offset the whole loan balance.the reason to do so is because we not sure when we will need to use that money in future once u settle the loan, means all the money cannot be used flexibly anymore. This post has been edited by theozis: Apr 21 2025, 12:48 PM |

|

|

Apr 21 2025, 12:54 PM

|

|

Junior Member

171 posts Joined: Dec 2006 |

QUOTE(marfccy @ Apr 21 2025, 11:34 AM) this is why every month i see bank transaction for my house its damn tiok. i pay RM2.8k/mth, then interest RM2.1k/mth. so basically im only clearing RM700/mth in principal zzzz if your parents money is placed in bank saving acc or FD which the interest rate is lower than your mortgage rate , then you might consider to use their money to offset the loan balance by paying the interest gap to your parents.thats why my pama back then offered to give me some cash to reduce the principal back then. i need to throw in more monies inside principal to reduce the interest ed No points to use your parents' money if their money is inside EPF or ASNB etc which have higher interest rate |

|

|

Apr 21 2025, 01:09 PM

|

|

Junior Member

535 posts Joined: Apr 2012 |

QUOTE(smallcrab @ Apr 21 2025, 08:31 AM) bank is just legal ah long Huh? 4-5% per annum cekik darah? How much is your yearly inflation?interest cekik darah |

|

|

Apr 21 2025, 01:20 PM

Show posts by this member only | IPv6 | Post

#110

|

|

Senior Member

4,254 posts Joined: Nov 2011 |

QUOTE(theozis @ Apr 21 2025, 12:54 PM) if your parents money is placed in bank saving acc or FD which the interest rate is lower than your mortgage rate , then you might consider to use their money to offset the loan balance by paying the interest gap to your parents. its ready to be used, since its just one of the investment returns they closed off recentlyNo points to use your parents' money if their money is inside EPF or ASNB etc which have higher interest rate |

|

|

Apr 21 2025, 01:46 PM

|

|

Newbie

3 posts Joined: Jun 2017 |

QUOTE(cms @ Apr 21 2025, 11:54 AM) Yeah i get it. So lets find ways to make more money or just use less. Else it would be worst in the future. Of course individual should try to make/save more money...But these kinda trend should be also be controlled by government... Cannot be always up to individual responsibility Government is also responsible. If what the other guy said is true, in the 90s house prices 70k to 100k, in 2000s become 200k, then government has answer why price can x2 in a decade, but salary remain stagnant. |

|

|

Apr 21 2025, 02:11 PM

Show posts by this member only | IPv6 | Post

#112

|

|

Senior Member

3,562 posts Joined: Sep 2005 From: Shenzhen Bahru |

QUOTE(gamehype @ Apr 21 2025, 01:46 PM) Of course individual should try to make/save more money... I prefer government to regulate and control number of properly launches. No need to regulate interest rate. That one let banks to fight along themBut these kinda trend should be also be controlled by government... Cannot be always up to individual responsibility Government is also responsible. If what the other guy said is true, in the 90s house prices 70k to 100k, in 2000s become 200k, then government has answer why price can x2 in a decade, but salary remain stagnant. |

|

|

Apr 21 2025, 02:14 PM

Show posts by this member only | IPv6 | Post

#113

|

|

Newbie

5 posts Joined: Oct 2016 |

The golden rule is when u see house price 30k it’s actually 60k |

|

|

Apr 21 2025, 02:15 PM

Show posts by this member only | IPv6 | Post

#114

|

|

Senior Member

3,562 posts Joined: Sep 2005 From: Shenzhen Bahru |

QUOTE(AgogoLatoto @ Apr 21 2025, 02:14 PM) The golden rule is when u see house price 30k it’s actually 60k For someone that bought RM1mil property and intend to sell after 30 years…you reckon he can sell the old house for >RM2mil? To recoup his “investment” |

|

|

Apr 21 2025, 02:17 PM

|

Senior Member

3,833 posts Joined: Oct 2006 From: Shah Alam |

rumah apa harga 35k

|

|

|

Apr 21 2025, 02:19 PM

|

|

Newbie

3 posts Joined: Jun 2017 |

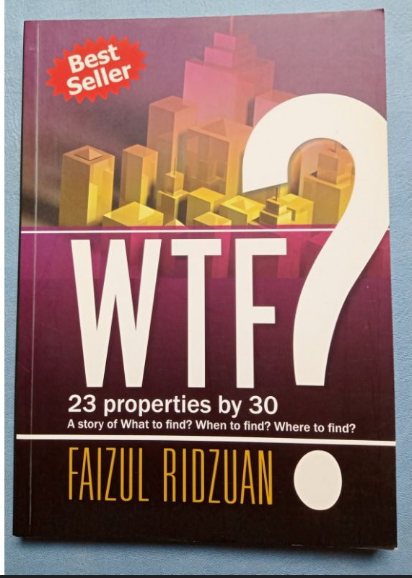

QUOTE(knwong @ Apr 21 2025, 02:11 PM) I prefer government to regulate and control number of properly launches. No need to regulate interest rate. That one let banks to fight along them I want government to control how many units 1 person can ownRemember this book  I don't know if this guy really had 23 property by 30, but this is what government should control. No one should have 23 property or even 13 property no matter how rich they are. It is these kinda people that drive up our property prices. |

|

|

Apr 21 2025, 02:21 PM

Show posts by this member only | IPv6 | Post

#117

|

|

Senior Member

3,562 posts Joined: Sep 2005 From: Shenzhen Bahru |

QUOTE(gamehype @ Apr 21 2025, 02:19 PM) I want government to control how many units 1 person can own This one I disagree. If I have big piece of land and I want to build many houses on it…to house my workers…government shouldn’t regulate thatRemember this book I don't know if this guy really had 23 property by 30, but this is what government should control. No one should have 23 property or even 13 property no matter how rich they are. It is these kinda people that drive up our property prices. |

|

|

Apr 21 2025, 02:22 PM

Show posts by this member only | IPv6 | Post

#118

|

|

Newbie

5 posts Joined: Oct 2016 |

QUOTE(knwong @ Apr 21 2025, 02:15 PM) For someone that bought RM1mil property and intend to sell after 30 years…you reckon he can sell the old house for >RM2mil? To recoup his “investment” After 30 years baru habis bayar? Hell no.If u finish pay earlier than maybe can cover the loss from interest, make small money from that amt. otherwise, no. Who wanna buy 2mil property? |

|

|

Apr 21 2025, 02:23 PM

Show posts by this member only | IPv6 | Post

#119

|

Newbie

16 posts Joined: Jun 2009 |

Tu la, sekolah tak mau pigi

|

|

|

Apr 21 2025, 02:29 PM

Show posts by this member only | IPv6 | Post

#120

|

|

Newbie

16 posts Joined: Jun 2009 |

QUOTE(gamehype @ Apr 21 2025, 02:19 PM) I want government to control how many units 1 person can own If gomen introduce inheritance tax, increase property tax. Habis diaRemember this book I don't know if this guy really had 23 property by 30, but this is what government should control. No one should have 23 property or even 13 property no matter how rich they are. It is these kinda people that drive up our property prices. He is smart if make use of the bumi discounts and loans loopholes |

|

|

Apr 21 2025, 02:34 PM

|

|

Newbie

3 posts Joined: Jun 2017 |

QUOTE(knwong @ Apr 21 2025, 02:21 PM) This one I disagree. If I have big piece of land and I want to build many houses on it…to house my workers…government shouldn’t regulate that Then he can build worker hostel. Not buy property from open market.I am very specific here. I am talking about people who buy property from the open market to speculate. Also. If. If la. Meaning you don't have that big piece of land la brother. Bro, there is no need to argue on behalf of the rich people. They won't fight on your behalf. This post has been edited by gamehype: Apr 21 2025, 02:36 PM |

|

|

Apr 21 2025, 02:43 PM

|

Senior Member

3,599 posts Joined: Jun 2009 From: MYBoleh.NET |

QUOTE(Freshmeat21 @ Apr 21 2025, 02:29 PM) If gomen introduce inheritance tax, increase property tax. Habis dia just use loophole to avoid inheritance tax easy peasy. This tax is pretty old and many riches edi avoiding it with loopholesHe is smart if make use of the bumi discounts and loans loopholes |

|

|

Apr 21 2025, 03:22 PM

Show posts by this member only | IPv6 | Post

#123

|

|

Junior Member

70 posts Joined: Nov 2014 From: The 10th Dimension |

QUOTE(iGamer @ Apr 21 2025, 12:44 PM) Aiyoyo if like that they probably push u to the bank with best commission to them instead of best bank offer…. Yes it was my first time, and these humgarchan squeezed me kao²But well...the house luckily only 100k so yea sadding really QUOTE(theozis @ Apr 21 2025, 12:47 PM) personal opinion is dont settle the flexi loan even have the money to offset the whole loan balance. I know, need to calculate the value lothe reason to do so is because we not sure when we will need to use that money in future once u settle the loan, means all the money cannot be used flexibly anymore. |

|

|

Apr 21 2025, 03:31 PM

|

Senior Member

1,256 posts Joined: Dec 2013 |

QUOTE(Freshmeat21 @ Apr 21 2025, 02:29 PM) If gomen introduce inheritance tax, increase property tax. Habis dia Make use? How?He is smart if make use of the bumi discounts and loans loopholes |

|

|

Apr 21 2025, 03:34 PM

|

|

Senior Member

1,374 posts Joined: Feb 2016 From: Milky Way |

QUOTE(theozis @ Apr 21 2025, 12:47 PM) personal opinion is dont settle the flexi loan even have the money to offset the whole loan balance. Yes, but for some time there were many news of people’s bank account money being stolen. the reason to do so is because we not sure when we will need to use that money in future once u settle the loan, means all the money cannot be used flexibly anymore. So when we can settle the loan and still have more than enough for any emergency, then it’s peace of mind to just clear the loan. jojolicia liked this post

|

|

|

Apr 21 2025, 03:35 PM

Show posts by this member only | IPv6 | Post

#126

|

All Stars

10,477 posts Joined: Jan 2003 From: Sarawak |

QUOTE(kcchong2000 @ Apr 21 2025, 07:14 AM) Ehh. Kamu kena bayar bank interest. I normally just double the house price and keep it in my mind before I buy the house. loan interest is not for peasants.Macam pinjam 35k then bayar 35k Kah? |

|

|

Apr 21 2025, 03:39 PM

Show posts by this member only | IPv6 | Post

#127

|

|

Junior Member

76 posts Joined: Jun 2019 |

banks: dont joke la. lu mau pakai cash beli civic and houses?

|

|

|

Apr 21 2025, 03:42 PM

Show posts by this member only | IPv6 | Post

#128

|

Junior Member

863 posts Joined: Apr 2019 |

QUOTE(iGamer @ Apr 21 2025, 07:29 AM) That’s why full flexi housing loan was best, ayam clear 30yrs loan in 7 years. not possible anymore , because in your boomer time central bank interest started at 15% and gradually decreasing every year to eventually fed zero percent. now interest rate rising, banks will rugi if they let you redeem early. |

|

|

Apr 21 2025, 03:46 PM

|

|

Senior Member

1,374 posts Joined: Feb 2016 From: Milky Way |

QUOTE(diffyhelman2 @ Apr 21 2025, 03:42 PM) not possible anymore , because in your boomer time central bank interest started at 15% and gradually decreasing every year to eventually fed zero percent. now interest rate rising, banks will rugi if they let you redeem early. Ayam not boomer lah |

|

|

Apr 21 2025, 03:47 PM

Show posts by this member only | IPv6 | Post

#130

|

|

Junior Member

863 posts Joined: Apr 2019 |

QUOTE(iGamer @ Apr 21 2025, 03:46 PM) Ayam not boomer lah I know. but basically worldwide interest rates was decreasing from 80s to 2020. so it was OK for banks to let you redeem early, as their bond portfolio assets would be increasing in price. now that interest rates are going to be same or higher, they wont let ppl redeem old loans early unless you pay a penalty which would basically wipe out any savings you get.This post has been edited by diffyhelman2: Apr 21 2025, 03:48 PM |

|

|

Apr 21 2025, 03:50 PM

|

|

Junior Member

65 posts Joined: Apr 2022 |

QUOTE(Ickythump @ Apr 21 2025, 07:20 AM) what kind of rumah 35k i take 2 pay cash this place i bet you don't wanna stay. |

|

|

Apr 21 2025, 03:54 PM

Show posts by this member only | IPv6 | Post

#132

|

|

Junior Member

863 posts Joined: Apr 2019 |

QUOTE(cooldog_777 @ Apr 21 2025, 03:50 PM) this place i bet you don't wanna stay. PPR type flat? in before developer offer to buy over and give you replacement |

|

|

Apr 21 2025, 04:03 PM

|

Senior Member

7,938 posts Joined: Mar 2014 |

When you take loan with such and such interest rate, you imagine like buying car where your premium decreased with each payment.

In reality, most of our payment each month goes to the interest part and small percentage goes to the loan principle. After so many years you found out the loan decrement is only very little. I think you just use Islamic banking when you know from day one how much you need to pay. It is like they buy the house first and you agree to buy at selling price and pay the bank gradually. |

|

|

Apr 21 2025, 05:12 PM

|

|

Senior Member

3,562 posts Joined: Sep 2005 From: Shenzhen Bahru |

QUOTE(iGamer @ Apr 21 2025, 03:34 PM) Yes, but for some time there were many news of people’s bank account money being stolen. I heard of people bank account money kena stolenSo when we can settle the loan and still have more than enough for any emergency, then it’s peace of mind to just clear the loan. Haven't heard of home loan flexi account kena withdrawn or stolen...FYI you need to pay a fee to withdraw |

|

|

Apr 21 2025, 05:18 PM

|

|

Senior Member

1,374 posts Joined: Feb 2016 From: Milky Way |

QUOTE(knwong @ Apr 21 2025, 05:12 PM) I heard of people bank account money kena stolen Not with my full flexi, My PBB full flexi is just a current account. No fees needed to move funds. Bank won’t ask any question even if the account is emptied.Haven't heard of home loan flexi account kena withdrawn or stolen...FYI you need to pay a fee to withdraw Edit: for example, loan balance RM200k, so if I have RM200k in this current account, the outstanding loan principal that will be charged interest is zero. Any money put into this current account will automatically offset loan principal, no need inform bank no matter how we put in or withdraw money. This post has been edited by iGamer: Apr 21 2025, 05:37 PM |

|

|

Apr 21 2025, 06:02 PM

Show posts by this member only | IPv6 | Post

#136

|

Senior Member

1,692 posts Joined: Mar 2009 From: Probation? |

3.75 interest ?

|

|

|

Apr 21 2025, 06:09 PM

Show posts by this member only | IPv6 | Post

#137

|

|

Junior Member

190 posts Joined: Oct 2020 |

QUOTE(samftrmd @ Apr 21 2025, 07:25 AM) I wish I can find a house in kl with that price. don’t mention house, flat also cannot get la.. |

|

|

Apr 21 2025, 06:14 PM

Show posts by this member only | IPv6 | Post

#138

|

Junior Member

235 posts Joined: Feb 2017 |

Another entitled mindset joker

|

|

|

Apr 21 2025, 06:16 PM

Show posts by this member only | IPv6 | Post

#139

|

|

Junior Member

235 posts Joined: Feb 2017 |

QUOTE(iGamer @ Apr 21 2025, 05:18 PM) Not with my full flexi, My PBB full flexi is just a current account. No fees needed to move funds. Bank won’t ask any question even if the account is emptied. Full flexi instead rate better than semi flexi?Edit: for example, loan balance RM200k, so if I have RM200k in this current account, the outstanding loan principal that will be charged interest is zero. Any money put into this current account will automatically offset loan principal, no need inform bank no matter how we put in or withdraw money. If no, go for semi. U will think twice before withdraw since it come with rm50 processing fee |

|

|

Apr 21 2025, 06:17 PM

Show posts by this member only | IPv6 | Post

#140

|

|

Junior Member

235 posts Joined: Feb 2017 |

QUOTE(Zot @ Apr 21 2025, 04:03 PM) When you take loan with such and such interest rate, you imagine like buying car where your premium decreased with each payment. Flexi loan provide flexibility compared to fixed loanIn reality, most of our payment each month goes to the interest part and small percentage goes to the loan principle. After so many years you found out the loan decrement is only very little. I think you just use Islamic banking when you know from day one how much you need to pay. It is like they buy the house first and you agree to buy at selling price and pay the bank gradually. Can pay more to reduce principal and withdrawal when needed |

|

|

Apr 21 2025, 06:18 PM

|

Newbie

23 posts Joined: Mar 2018 |

sudah bayar lebih 40 k

|

|

|

Apr 21 2025, 06:26 PM

|

|

Senior Member

1,374 posts Joined: Feb 2016 From: Milky Way |

QUOTE(abelyap @ Apr 21 2025, 06:16 PM) Full flexi instead rate better than semi flexi? Back then I never heard of semi-flexi, only conventional housing loan or full flexi loan from the banks that I applied. If no, go for semi. U will think twice before withdraw since it come with rm50 processing fee There’s only one fee, RM10/month for this full flexi facility. No other charges, we are free to move money in and out as we like. Iinm my interest was BLR+1.x% back then. |

|

|

Apr 21 2025, 06:28 PM

Show posts by this member only | IPv6 | Post

#143

|

|

Junior Member

190 posts Joined: Oct 2020 |

QUOTE(iGamer @ Apr 21 2025, 05:26 PM) Back then I never heard of semi-flexi, only conventional housing loan or full flexi loan from the banks that I applied. my loan was done in 2010, semi flexi…so should have existed before that.. There’s only one fee, RM10/month for this full flexi facility. No other charges, we are free to move money in and out as we like. Iinm my interest was BLR+1.x% back then. |

|

|

Apr 21 2025, 06:30 PM

Show posts by this member only | IPv6 | Post

#144

|

|

Junior Member

235 posts Joined: Feb 2017 |

QUOTE(iGamer @ Apr 21 2025, 06:26 PM) Back then I never heard of semi-flexi, only conventional housing loan or full flexi loan from the banks that I applied. When the loan? Back in 2010 i already use semi flexi under PBB There’s only one fee, RM10/month for this full flexi facility. No other charges, we are free to move money in and out as we like. Iinm my interest was BLR+1.x% back then. |

|

|

Apr 21 2025, 06:35 PM

|

Senior Member

937 posts Joined: Jun 2006 |

QUOTE(smallcrab @ Apr 21 2025, 08:31 AM) bank is just legal ah long lu geng lu pay cash lo.interest cekik darah xCM liked this post

|

|

|

Apr 21 2025, 06:36 PM

|

|

Senior Member

1,374 posts Joined: Feb 2016 From: Milky Way |

QUOTE(KenM @ Apr 21 2025, 06:28 PM) my loan was done in 2010, semi flexi…so should have existed before that.. QUOTE(abelyap @ Apr 21 2025, 06:30 PM) When the loan? Back in 2010 i already use semi flexi under PBB I checked my statement, I took the loan from PBB on 2013. So, it seems they started to offer full flexi by the time I borrowed |

|

|

Apr 21 2025, 06:38 PM

|

Junior Member

94 posts Joined: Sep 2020 |

pls keep more bifoti unaware of how bank interests works

my bank stocks dividend will thank them for many years just received 14k from rhb few days ago.. hnghhhh now waiting for dividends from other banks (bimb, mbb, cimb) |

|

|

Apr 21 2025, 06:40 PM

Show posts by this member only | IPv6 | Post

#148

|

|

Junior Member

235 posts Joined: Feb 2017 |

QUOTE(iGamer @ Apr 21 2025, 06:36 PM) I checked my statement, I took the loan from PBB on 2013. So, it seems they started to offer full flexi by the time I borrowed I got another loan under PBB in 2023, still hv semi flexiFull flexi with monthly rm10 does not make sense unless ur saved interest from money moving in out is so much that it cover rm10 fee Every rm1000 will caused rough 10 cents interest per day So rm10 mean rm100000 over the 30 days. Average 3k |

|

|

Apr 21 2025, 06:45 PM

Show posts by this member only | IPv6 | Post

#149

|

|

Junior Member

140 posts Joined: Jul 2007 From: Puchong |

QUOTE(abelyap @ Apr 21 2025, 06:40 PM) I got another loan under PBB in 2023, still hv semi flexi Is accountancy your profession?Full flexi with monthly rm10 does not make sense unless ur saved interest from money moving in out is so much that it cover rm10 fee Every rm1000 will caused rough 10 cents interest per day So rm10 mean rm100000 over the 30 days. Average 3k |

|

|

Apr 21 2025, 06:48 PM

|

|

Senior Member

1,374 posts Joined: Feb 2016 From: Milky Way |

QUOTE(abelyap @ Apr 21 2025, 06:40 PM) I got another loan under PBB in 2023, still hv semi flexi RM2.8k x 4.3% = RM120.40Full flexi with monthly rm10 does not make sense unless ur saved interest from money moving in out is so much that it cover rm10 fee Every rm1000 will caused rough 10 cents interest per day So rm10 mean rm100000 over the 30 days. Average 3k So by having around RM2.8k in the account, that already offset the interest as much.  The flexibility/liquidity that I get over the years, surely I saved much more than that petty Rm120/year. Edit: without such convenient flexibility, surely u will also keep a few thousand somewhere else like saving account that pay no interest just for normal spending. So why not just keep in this current account and as u can still spend it as u need?  This post has been edited by iGamer: Apr 21 2025, 06:53 PM gobiomani liked this post

|

|

|

Apr 21 2025, 06:49 PM

Show posts by this member only | IPv6 | Post

#151

|

|

Junior Member

190 posts Joined: Oct 2020 |

QUOTE(iGamer @ Apr 21 2025, 05:36 PM) I checked my statement, I took the loan from PBB on 2013. So, it seems they started to offer full flexi by the time I borrowed 2010, they had full flexibility but business was just starting, didn’t take the risk.. |

|

|

Apr 21 2025, 06:50 PM

|

Senior Member

1,420 posts Joined: Nov 2013 |

35k i bayar cash je dey

|

|

|

Apr 21 2025, 08:21 PM

Show posts by this member only | IPv6 | Post

#153

|

|

All Stars

17,021 posts Joined: Jan 2005 |

QUOTE(sihamsedap @ Apr 21 2025, 06:38 PM) pls keep more bifoti unaware of how bank interests works The bank should explain to every person that success make a loan. my bank stocks dividend will thank them for many years just received 14k from rhb few days ago.. hnghhhh now waiting for dividends from other banks (bimb, mbb, cimb) Doesn’t need complicated but simple write down. That should prevent such idiot b40 from posting stupid thing. |

|

|

Apr 21 2025, 10:07 PM

|

|

Junior Member

171 posts Joined: Dec 2006 |

so far , there were full flexi, semi-flexi and fixed rate mortgage offered in the past. but I believe nowadays, only full flexi and semi-flexi available in the market. as I know, most of mortgage before 2005 was fixed rate. so, when that time BLR came down due to 2008 US stock crisis, those smart will engage with the bank to lower the rate. else jump ship to other bank which ppl called it refinance meanwhile, semi-flexi and full flexi become popular after 2006. typical features of full flexi is no need inform bank regarding money deposit or withdrawal. As a compensation to bank, a monthly fee of RM10 is imposed. For a short period, CIMB offered no fee charges. for semi-flexi, additional deposit has to trigger bank earlier as advance payment , pre-payment or you name it (different name with different purpose). Same goes to withdrawal. No monthly fee required but bank charge withdrawal fee of RM50 each time. During the market promo, there was some lucky peoples managed to grab bank promo with withdrawal fee of RM25 (unsure any lower fee that time) in 2015, BLR evolved to BR subsequently again to SBR in 2022. Anyway, actual rate is around 4.3-4.5% currently, depends on many factors like loan amount, tenure , DSR etc. This post has been edited by theozis: Apr 21 2025, 10:15 PM iGamer liked this post

|

|

|

Apr 21 2025, 11:06 PM

Show posts by this member only | IPv6 | Post

#155

|

Senior Member

7,066 posts Joined: Sep 2019 From: South Klang Valley suburb |

QUOTE(lurkingaround @ Oct 10 2023, 03:20 PM) . https://forum.lowyat.net/index.php?showtopi...ost&p=108293530Seems, the Rule Of 78 is still being applied by Malaysian banks for long term housing loans. ....... https://www.investopedia.com/terms/r/ruleof78.asp - Rule of 78: Definition, How Lenders Use It, and Calculation By CAROLINE BANTON Updated March 06, 2021 Reviewed by THOMAS J. CATALANO What Is the Rule of 78? The Rule of 78 is a method used by some lenders to calculate interest charges on a loan. The Rule of 78 requires the borrower to pay a greater portion of interest in the earlier part of a loan cycle, which decreases the potential savings for the borrower in paying off their loan. ... In 1992, the legislation made this type of financing illegal for loans in the United States with a duration of greater than 61 months. .... . QUOTE(knwong @ Apr 21 2025, 06:40 AM) I think the math checks out no? QUOTE(hteekay @ Apr 21 2025, 09:38 AM) Checks out. .It is frustrating, but Bank Negara and other banks are seriously worst than Arlong when it comes to House Loan, more than half of the loan period are majority you're paying the interests 1st, and because of that, the interests keep piling up because your principal only decrease only a small amount each year. My repost above fyi. Pro-business politics has allowed this "ahlongness" by banks in Malaysia to continue. . |

|

|

Apr 21 2025, 11:16 PM

Show posts by this member only | IPv6 | Post

#156

|

|

Junior Member

284 posts Joined: Aug 2021 |

QUOTE(ozak @ Apr 21 2025, 08:21 PM) The bank should explain to every person that success make a loan. reading and understand the Co tract isn't a culture to MalaysiansDoesn’t need complicated but simple write down. That should prevent such idiot b40 from posting stupid thing. |

|

|

Apr 22 2025, 08:27 AM

|

|

Senior Member

3,562 posts Joined: Sep 2005 From: Shenzhen Bahru |

QUOTE(elloy @ Apr 21 2025, 06:18 PM) sudah bayar lebih 40 k 40k +11k (KWSP) jadi dah lebih 51k |

|

|

Apr 22 2025, 08:35 AM

|

|

Senior Member

1,922 posts Joined: Feb 2016 |

QUOTE(lurkingaround @ Apr 21 2025, 11:06 PM) https://forum.lowyat.net/index.php?showtopi...ost&p=108293530 Nothing wrong with interest levied to amount drawndown. It's daily rest, monthly rest all levied to principal owing. . My repost above fyi. Pro-business politics has allowed this "ahlongness" by banks in Malaysia to continue. . You don't want incur/ tanggung interest you pare down your principal owing at early stage la. There is no free money. Bank money drawndown for you is money loan to you, owned by someone. Nothing is free, except gov loan maybe This post has been edited by jojolicia: Apr 22 2025, 03:03 PM |

|

|

Apr 22 2025, 08:40 AM

|

|

Senior Member

7,938 posts Joined: Mar 2014 |

QUOTE(abelyap @ Apr 21 2025, 06:17 PM) Flexi loan provide flexibility compared to fixed loan Even the fixed loan also can pay lump sum to reduce loan principle. Not sure about current practice but last time you need to notify bank that you want to pay lump sum off the monthly installment. This will deduct the loan principle.Can pay more to reduce principal and withdrawal when needed Flexi loan is something different last time I understood. Say that you paid huge sum to reduce principle but later you run short of money and you can even reduce monthly payment when required. I don't know the detail because never use that kind of facility. |

|

|

Apr 22 2025, 08:44 AM

|

|

Senior Member

2,672 posts Joined: Sep 2006 |

The ignorants should at least play this calculator:

https://www.calculator.net/amortization-calculator.html |

|

|

Apr 22 2025, 08:48 AM

Show posts by this member only | IPv6 | Post

#161

|

|

Senior Member

5,974 posts Joined: Jan 2003 From: KL, Malaysia |

With flexi loan account, you can take all FD 3% and put in flexi can save 4.5%… assuming you are not renting the property else will be taxed higher (not worth it)… if own stay then okay … even better make the account your saving account or salary account

|

|

|

Apr 22 2025, 09:16 AM

|

|

Senior Member

3,562 posts Joined: Sep 2005 From: Shenzhen Bahru |

QUOTE(p4n6 @ Apr 22 2025, 08:48 AM) With flexi loan account, you can take all FD 3% and put in flexi can save 4.5%… assuming you are not renting the property else will be taxed higher (not worth it)… if own stay then okay … even better make the account your saving account or salary account Even if FD & home loan interest is the same %, the calculations are different....it is always makes for sense to pay off the home loan as the savings are huge |

|

|

Apr 22 2025, 09:20 AM

|

|

Senior Member

1,922 posts Joined: Feb 2016 |

QUOTE(knwong @ Apr 22 2025, 09:16 AM) Even if FD & home loan interest is the same %, the calculations are different....it is always makes for sense to pay off the home loan as the savings are huge You cannot out speak the ones who say opportunity cost. Lol, as if opportunities come knocking day and night, end up spent day and night. This post has been edited by jojolicia: Apr 22 2025, 09:20 AM |

|

|

Apr 22 2025, 09:22 AM

Show posts by this member only | IPv6 | Post

#164

|

Senior Member

1,902 posts Joined: Sep 2012 |

QUOTE(wanted111who @ Apr 21 2025, 06:59 AM) They dont know 70:30. MOST OF THEM dunno about this I tell youBut suprising withdraw 11k kwsp still left so much balance, he didnt instruct the bank to allocate to pay principle. banks purposedly make it difficult for normies "just follow the instruction " the bank says  |

|

|

Apr 22 2025, 09:26 AM

Show posts by this member only | IPv6 | Post

#165

|

|

Senior Member

1,902 posts Joined: Sep 2012 |

QUOTE(lahart @ Apr 21 2025, 07:16 AM) Rumah 35k ?? QUOTE(Ickythump @ Apr 21 2025, 07:20 AM) what kind of rumah 35k i take 2 pay cash  all these from 1995 punya . rumah murah under PKNS. you need to be b40, never buy property before in malaysia |

|

|

Apr 22 2025, 01:22 PM

Show posts by this member only | IPv6 | Post

#166

|

|

Senior Member

5,974 posts Joined: Jan 2003 From: KL, Malaysia |

QUOTE(knwong @ Apr 22 2025, 09:16 AM) Even if FD & home loan interest is the same %, the calculations are different....it is always makes for sense to pay off the home loan as the savings are huge No. Pay off not beneficial. Put money in to reduce interests make sense. Cash flow is important. If got better opportunities can switch instantly. No point to pay off if no benefit. |

|

|

Apr 22 2025, 01:25 PM

Show posts by this member only | IPv6 | Post

#167

|

|

Junior Member

16 posts Joined: Feb 2022 |

Who ask to pay rm200, try RM 2000, or cash buy, RM 35k only.

|

|

|

Apr 22 2025, 01:31 PM

|

|

Senior Member

1,922 posts Joined: Feb 2016 |

QUOTE(JimbeamofNRT @ Apr 22 2025, 09:26 AM) all these from 1995 punya . rumah murah under PKNS. you need to be b40, never buy property before in malaysia Many renovated, extended 2 sty lol |

|

|

Apr 22 2025, 01:34 PM

Show posts by this member only | IPv6 | Post

#169

|

|

Junior Member

235 posts Joined: Feb 2017 |

QUOTE(smallcrab @ Apr 21 2025, 06:45 PM) Is accountancy your profession? No why?Just typical property buyer |

|

|

Apr 22 2025, 01:38 PM

|

|

Senior Member

1,053 posts Joined: Jan 2008 |

Tak sekolah macam ni lah jadinya. Forever B40

|

|

|

Apr 22 2025, 01:39 PM

Show posts by this member only | IPv6 | Post

#171

|

|

Junior Member

235 posts Joined: Feb 2017 |