any specific BNM email ?

It seems to me that this business is a sure win, any mispricing then they pass on via premium increase, and if over-price they sit happy with the bumper profit, this makes no sense....

How to deal with medical insurance repricing?

|

|

Jan 19 2024, 11:21 AM Jan 19 2024, 11:21 AM

Return to original view | IPv6 | Post

#1

|

Junior Member

159 posts Joined: Jul 2005 |

May i know if there are avenues to voice out my anger on this steep premium increase of 56% from GE !!!????

any specific BNM email ? It seems to me that this business is a sure win, any mispricing then they pass on via premium increase, and if over-price they sit happy with the bumper profit, this makes no sense.... |

|

|

|

|

|

Jan 19 2024, 11:41 AM

Return to original view | IPv6 | Post

#2

|

|

Junior Member

159 posts Joined: Jul 2005 |

QUOTE(contestchris @ Jan 19 2024, 11:27 AM) First question, what is your medical card? You can check in the attachment on that page. Hi, i see my plan has Smart Medic, Smart Medic 99, Smart early payout critical care, Critical illness benefit rider, IL Waiver of premium plus rider. Based on the breakdown of my premium paid statement, about 80% of the premium is related to medical. I am just wondering how come the increase can be so ridiculous, 56% is no joke at all.... |

|

|

Jan 19 2024, 11:54 AM

Return to original view | IPv6 | Post

#3

|

|

Junior Member

159 posts Joined: Jul 2005 |

QUOTE(MUM @ Jan 19 2024, 11:46 AM) Could be just could due to coinside or combination of medical inflation rise PLUS your age moved your premium to pay bracket to a more costlier rate. I m 38 this year, still within the 36-40 age group, even if the policy increase is for next year, i will still be 39....( check you policy for the table to see if your age had "upgraded" to a next age grouping?) feel like there is no way for us to complain, either take it or leave it.....sigh.... |

|

|

Jan 19 2024, 03:08 PM

Return to original view | IPv6 | Post

#4

|

|

Junior Member

159 posts Joined: Jul 2005 |

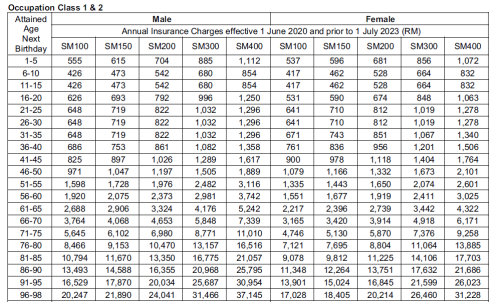

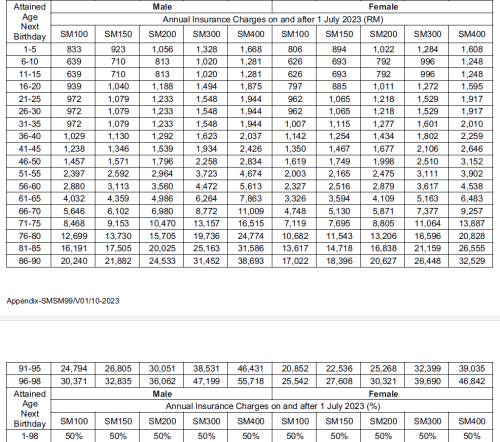

QUOTE(contestchris @ Jan 19 2024, 12:00 PM) From what I know, the quantum of increase for SmartMedic is 50% this time. In comparison, the quantum of increase for SmartMedic Xtra (which was launched after SmartMedic) is around 30%. i see 50% increase at the bottom of the appendix table. As to why the discrepancy, refer to the diagram in my first post. Your plan is older, hence it has more "bad risk". The average age would also be higher since it had closed to business earlier, and the healthier ones would've moved on to the newer (i.e. cheaper) plans. Generally, if you are healthy and have nothing wrong with your health, you should move to the newest plan, SmartMedic Shield. The medical plan's cost of insurance will be significantly lower and the benefits will be significantly better. Plus, with a deductible of RM300, the expectation is medical claims experience will be somewhat better contained. Can you share the quantum of increase from the PDF? At the bottom, they also share the % value in increase. Unfortunately, i have gastric problem and GE declined to cover that if i purchase a new plan, so i have to stick to this old and bad plan. I can only use company insurance for the time being to save personal medical plan for future. |

|

|

Jan 19 2024, 03:47 PM

Return to original view | IPv6 | Post

#5

|

|

Junior Member

159 posts Joined: Jul 2005 |

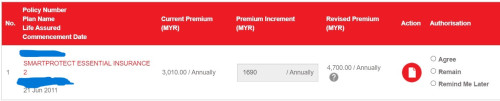

QUOTE(contestchris @ Jan 19 2024, 03:25 PM) How many repricing have you experienced? Any chance you can share the latest repriced rates table? Hi Chris, thanks so much for the suggestion. Any ballpark figure like how much lower the premium will be for like-for-like medical coverage?In any case, if you have pre-existing, you have 2 options: 1) Play it safe and maintain existing cover. Will be more expensive (and exponentially so as you get older as more and more repricings are done), but you will have certainty of cover. 2) Upgrade the medical plan with clearly disclosing your pre-existing. At this point, pre-existing illnesses will not be covered but at least your premiums will be lower. Under no circumstance should you upgrade your plan or buy a new plan without disclosing your pre-existing conditions, that's going to be a tough lesson to learn when they terminate your policy due to non-disclosure. please find below the revised table from the GE document   contestchris liked this post

|

| Change to: |  0.0236sec 0.0236sec

1.11 1.11

7 queries 7 queries

GZIP Disabled GZIP Disabled

Time is now: 13th December 2025 - 09:36 AM |

Quote

Quote