QUOTE(SKY 1809 @ Jan 12 2008, 07:10 PM)

I believe one should argue :-

a) basing the facts rather assumptions. For example if oil palm price is on high side, then you should not assume� plantation companies will make less money at the end of the day ( growth factor)

b) GDP or forecasted consensus GDP figure. Support with facts if you do not agree.

c) Track Records. If fund managers have good track records, respect them rather than passing unjust statements . Better if you provide your own investment track records here. A person with a small fund can always manage better than fund managers with billions of funds. But The freedom of webs do not give you right to criticise other people especially the specialists.

d) If you say either share mkt will go up or come down� anyway . Then you are protecting yourself without basis.

You should not give yourself the right to change the� future economy ( again assumptions) to� say� things according to your own ways.

If you change things here and there, basing on your own assumptions, then you are always right.

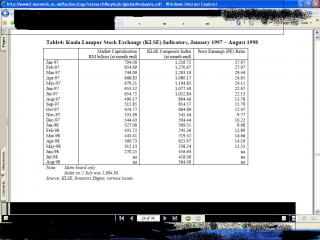

Added on January 12, 2008, 8:06 pmThe P/E of Year 1997 is based on Year 1996 earnings and not taking into accounts of currency losses. many companies have suffered huge losses during Year 1997. Companies at that times did not report Quarterly profits and biased. PE ratio as indicated showed highest 29 times acording to Year 1996 profits ? If adjusted to Year 1997 quarterly earnings, PE ratio of 40 times is justified. A lot of arguments over this area. Prudent is the key decision factor. Share prices do reflect the future earnings of companies such as palm oil prices. Some use adjusted pe and some use pure historical pe.� For example, last Year, there is an airline reported "wrong" profits, if you use adjusted pe, then you should come out with diff investment decisions.

If companies are to report better 2007 results and higher Year 2008 forecasts, then it is reasonable to use Year 2007 earnings. If companies forecast less favorable Year 2008 results, weight is also given here. Worst case or so called conservative approach.

US listed companies do have to provide earnings warnings to public, what about Malaysia ? Events such as Sub Prime issue will have impact not only the earnings and also can write off� the capital of listed companies. Hence the prices of shares drop. Likewise the CEO of US co could be forced out of office if show poor earnings. Hence, the Earnings and Price are well connected and important.

PM is only allowed to invest in Overseas from last year. Now the govenment again disallows fund fr EPf to be invested in Overseas, meaning their hands are tight. Therefore, it is fair to compare Apple with Apple, and do not� use foreign funds as the yardsticks. PM is prohibited from investing in Sub Prime sectors compared to US funds, but it is good for the interest of investors. PM do compare their returns with KLCI for local funds. It is only fair that you read before making a conclusion and passing general statements. And if think 5 years are not good enough, then take the 10 years returns.

One should take into the consideration of good and bad. If a fund could gain 200% a year, then it could suffer similar losses later, like funds invested in sub prime sector.

This part of discussion is related to PM or funds invested in unit trust. A DIY by yourself directly into KLSE should belong elsewhere.

I think you get me wrong here.

We just have the discussion of why I said (on my air view, nvm

) PE of 20-25 rather thn 40x issue. Nothing to do with funds or DIY investing which is just sub-part of discussion.

Another point is that for 1998, there is no PE, as most companies in KLSE are making a loss. That's why gov announced there is no income tax for corporate at that year.

Yup, historical data of PE can be useless, it is the future PE that's matter the most, but general market out there is using historical PE as future PE is largely depends on investment house estimation (can be varied quite significantly sometimes which led to different TP), which whether can materiliase as predicted still remains unknown, so there is generally practice (newspaper, magazine, research report) using historical PE (last financial year) then estimate the growth room for the earning in the future to justify it. Like that everyone across will seeing the same PE, if using future earning projection then it will become one report say PE 20, another one prints 15, the other one list as 10 due to different earning projection which only will lead to more confusion. So generally, people will list out the historical PE + future earning growth to justify the level of 'cheap or expensive'. That's why plantation stocks now are trading at 20+x PE mostly as future earning will grow significantly.

I don't make any assumption on company earning will go down nor plantation company will reporting lower earning (instead it would be signficant higher based in CPO price), while I don't make assumption GDP won't growth at 5-6% (instead mostly will be around that) nor discredit the PM or any funds.

Instead I view PM is one of the top fund out. I do invest in UT also, bare in mind.

Anyway out of topic too much as this thread should discuss about PM issue.

Cheers

This post has been edited by cherroy: Jan 13 2008, 07:27 AM

Jan 12 2008, 06:13 PM

Jan 12 2008, 06:13 PM

Quote

Quote

0.0336sec

0.0336sec

1.08

1.08

7 queries

7 queries

GZIP Disabled

GZIP Disabled