Outline ·

[ Standard ] ·

Linear+

MORATORIUM PEMBIAYAAN BANK SEMPENA WABAK COVID

|

gooroojee

|

Apr 5 2020, 11:28 AM Apr 5 2020, 11:28 AM

|

|

QUOTE(yklooi @ Apr 5 2020, 11:23 AM) on that, if one follows the thread, will have a clear answer by now. he/she will either get the answers or be more confused or be more doubtful. the more relevent one that could provide them with the peace of mind is as per below post. Linking to RP might confuse them more lol.. especially this old version before BNM's automatic moratorium. Some content still outdated. Plus their calculations also misleading. I hate it when half baked financial wannabes use the right formula and apply the wrong understanding to justify their recommendations. This post has been edited by gooroojee: Apr 5 2020, 11:31 AM |

|

|

|

|

|

gooroojee

|

Apr 5 2020, 11:33 AM

|

|

|

QUOTE(yklooi @ Apr 5 2020, 11:28 AM) yes, BUT if they did NOT ask and post here, they could NOT have gotten this reply which is very informative too. this is a very new info, which was not in this thread earlier,...thus, if those that read this thread earlier, do you think they would have gotten this tips? See below QUOTE(Human Nature @ Mar 27 2020, 12:41 PM) There is no interest accrued for HP. Just pay the installments as per normal after the 6 months period. |

|

|

|

|

|

gooroojee

|

Apr 5 2020, 11:52 AM

|

|

|

QUOTE(!@#$%^ @ Apr 5 2020, 11:33 AM) you are right, he tagged the wrong post. he indeed confused them now. haha And the one you retagged is the one I'm referring to with the misleading recommendations. Option 1, 2a, 2b and 3 are all different variations of early principal reduction vs. one that maintains the monthly payment amount. Obviously all early payments reduce interest. The one that completely removes all interest is if you paid the entire loan now. Mathematically correct, but defeats the purpose of the loan. What's worse, the writer takes the interest saved from a early principal reduction and claims it's interest saved from putting the money into a separate investment at 4%. Complete horseshit advice. |

|

|

|

|

|

gooroojee

|

Apr 5 2020, 12:05 PM

|

|

|

QUOTE(!@#$%^ @ Apr 5 2020, 11:54 AM) i think depends how your interpret the article. i think it's quite comprehensive. options given but ultimately up to loan takers to decide what is best for them. Hmm can't comment about your interpretation then. To each their own as they say. I would say if your loan was 4% , and there was an FD available at 4%... then if you don't have cash flow problems just keep paying off your loan, and opt out of the moratorium... do not follow RP advice to take the moratorium, and then put the 6 months of deferred payments into the FD and then expect to get RM22k more money. The RM22k comes from early principal reduction, not from the FD. The FD was irrelevant. Many RP readers will not understand this because even the RP writer confused himself when he was crunching too many numbers. |

|

|

|

|

|

gooroojee

|

Apr 5 2020, 02:24 PM

|

|

|

QUOTE(MUM @ Apr 5 2020, 01:53 PM) if those want to follow the above.....do take notes of these below too... Agreed. Always ask your own bank for the best advice. Here we can only help by trying to explain but sometimes even our explanations are understood in the wrong way. Now I understand why the experts keep their advice to a minimum, or only to those who pay good money for it. |

|

|

|

|

|

gooroojee

|

Apr 9 2020, 10:48 AM

|

|

|

QUOTE(AskarPerang @ Apr 9 2020, 10:24 AM) Good effort. Basically shows how to apply the calculations correctly based on available options made available by different banks. As mentioned before, anyone can use a calculator to get the right results, but still apply the wrong understanding. Some will look at that RM33k in the future after 30 years+ and feel like it's a lot more than the RM10k today. But the truth is they are actually the same. Those with the means of making more than 4% return will be happy to pay only rm33k in the future. Those who only know FD at 3% might be better off settling the RM10k debt now. |

|

|

|

|

|

gooroojee

|

Apr 25 2020, 01:30 AM

|

|

|

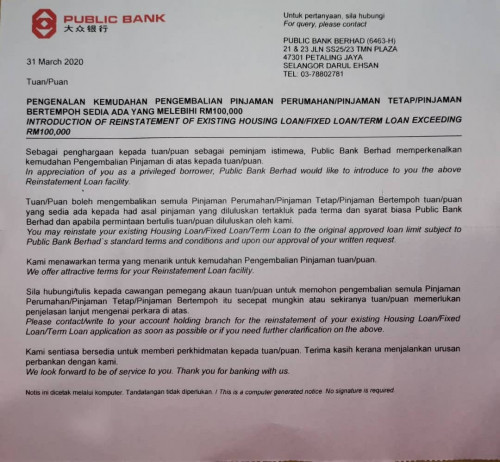

QUOTE(NoFrill @ Apr 25 2020, 01:01 AM)  I am actually opt-in for loan moratorium. Today received this letter dated 31 Mar which before moratorium officially start. Anybody received such letter from PBB? I don't understand what the reinstatement is about. It's not related. Just an offer for you to take out another loan with PBB and make them rich another time... and if you are actually looking for a loan, then could be useful for you too... |

|

|

|

|

|

gooroojee

|

May 3 2020, 12:30 AM

|

|

|

QUOTE(AskarPerang @ May 3 2020, 12:24 AM) Give one like. End of the day still up to bank if they want to impose or not .. |

|

|

|

|

|

gooroojee

|

May 7 2020, 08:47 AM

|

|

|

QUOTE(ipunk1026 @ May 7 2020, 08:08 AM) very confusing, my HP loan confirm not extra interest right? Confirm. |

|

|

|

|

|

gooroojee

|

Jul 6 2021, 07:40 PM

|

|

|

QUOTE(ronnie @ Jul 6 2021, 01:00 PM) MBB's Hire Purchase moratoriums is to extend the tenure by 12-24 months... #bodoh Extend but reduced payment amounts maybe? To ease the burden on rakyat? Not sure but would be useful to see the T&Cs and actual numbers. |

|

|

|

|

Quote

Quote 0.0391sec

0.0391sec

0.60

0.60

7 queries

7 queries

GZIP Disabled

GZIP Disabled