Aug 9 2020, 12:08 PM

Aug 9 2020, 12:08 PM

QUOTE(Macy Insurance Advisor @ Aug 9 2020, 12:00 PM)

Its better to have your own medical card, because if you resign or terminated from the company, then you may not entitle to have coverage in another company. and company provides insurance may low coverage. and medical cost goes up by the time and your age goes up.

on that, i think i read many times in here....that they mentioned the money spend on buying in the younger age (where the probability of claiming is much lower) can well be channeled into investment

then buy only when older age,...yes, the premium may be higher when older, but the amount of money generated from investment from using the premium to invest instead of buying med insurance at younger age would be more

also when you buy medical insurance at younger age,...will it be fixed premium through out the lifespan?

or the medical insurance premium will continue to go up every few years from XX age? (example from age 45?)

This post has been edited by MUM: Aug 9 2020, 12:28 PM

Quote

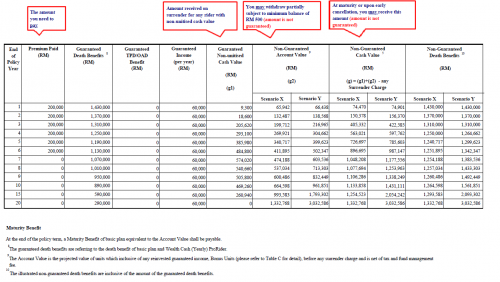

Quote May be try different scenario as conclusion.

May be try different scenario as conclusion.

that is "BAD"

that is "BAD"

0.1444sec

0.1444sec

0.45

0.45

7 queries

7 queries

GZIP Disabled

GZIP Disabled