Hi both sifu, appreciate your time with my matters. I'd attached the policy for your better understanding.

However, just now i went to the OCBC branch and quarrel about the dispute.

The advisor should not recommend such kind of "retirement" product for "retired" women. What use for my mum to invest her retirement fund and get it at 75 years old as another retirement fund?

That is not professional at all.

After my dispute with the branch manager and the service advisor, we came into the outcome:-

First year 50k distribution had been made, can't do anything, they also strongly recommend not to surrender

Yesterday another RM50k of auto direct debit had been happened. Talked to branch manager that we are not intend for investment another RM50k for 2nd year.

They mentioned that this product , the contribution can be decrease to lowest amount that is RM6k per year (for year 2 to year 5)

We both agree with this outcome, but they need a week to work on my withdraw of the RM50k paid on the 2nd year, and continue with RM6k yearly contribution for 2nd year to 5th year, and they need to deal with Headquaters about re calculate the guarantee payout and other tables etc

If the branch manager can come out with this results, i think probably i will just left the monies RM74k in total there, and untouchable for 13 years until 75years old.

Just the matters of, the guarantee payout and total gain after maturity date. (awaiting them for calculation and outcome)

If it doesn't go into this way (RM50k for 2nd years cannot be reverse or etc), probably i will work on another direction, BNM telelink or ombudsman, but i think it's long and hassle way to go.

Appreciate sifu will give me advise after spending your free time on my attached policy table.

[attachmentid=10545719]

Add On: The branch manager and the advisor mentioned that it is possible to decrease the contribution as low as minimum RM6k per year. Now the main dispute is only for the RM50k had been auto debit yesterday, but the Due date is today, and they have to inform us before they done the transaction due to big amount that not everyone can afford

Jul 22 2020, 05:54 PM

Jul 22 2020, 05:54 PM

Quote

Quote

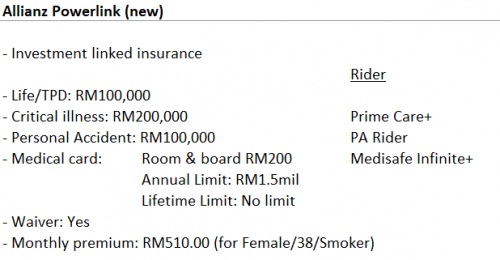

He did quote me a similar package for GE to match the coverage by Allianz but the monthly premium is higher at RM575 and I need to top up / pay extra since I wanted early payout for critical care, whereas Allianz already have payout at all stages.

He did quote me a similar package for GE to match the coverage by Allianz but the monthly premium is higher at RM575 and I need to top up / pay extra since I wanted early payout for critical care, whereas Allianz already have payout at all stages.

0.1364sec

0.1364sec

0.36

0.36

7 queries

7 queries

GZIP Disabled

GZIP Disabled