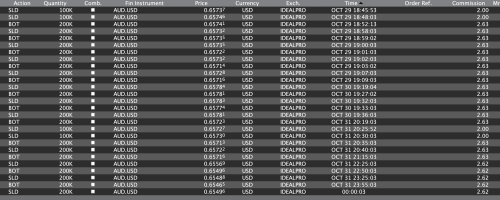

Wow, today's scalping profits set to break all records...

Sold 113 BIL at 91.79 this morning, and another 68 units at 91.75 this afternoon.

Sell-leg commissions = 0.66 + 0.51 USD = 1.17 USD

Now US premarket session suggests 91.69-91.70 is the correct range.

Suppose I were to buy back all 181 units of BIL at 91.69, with 0.36 USD commissions (prior to exchange liquidity discount), that would amount to a total profit of 13.85 USD... For one day!

This post has been edited by TOS: Oct 22 2024, 04:15 PM

Wow, today's scalping profits set to break all records...

Sold 113 BIL at 91.79 this morning, and another 68 units at 91.75 this afternoon.

Sell-leg commissions = 0.66 + 0.51 USD = 1.17 USD

Now US premarket session suggests 91.69-91.70 is the correct range.

Suppose I were to buy back all 181 units of BIL at 91.69, with 0.36 USD commissions (prior to exchange liquidity discount), that would amount to a total profit of 13.85 USD... For one day!

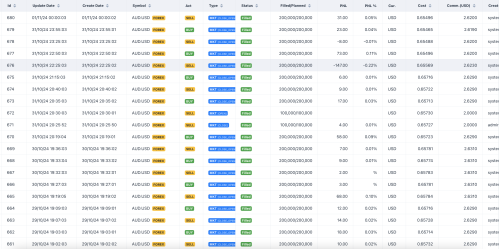

Trade closed early morning. It has been a long day...

Which US T-bills ETF is recommended for set and forget short to med term? And please elaborate how you are scalping for more yield? Also what do you mean by borrowing USD and trading in Asian hours?

Hi there. BIL ETF is recommended for short-term USD parking. As for how to scalp for more returns, I detailed the strategy in the previous posts.

In the future, I won't be sharing any more strategies... You guys just want to free-ride everything...

Now I know why top quant hedge funds jealously guard their "strategies"... I am gonna guard mine as well... proprietary secrets not to be revealed...

Bloomberg Markets: Top China Quant Offers Permanent Zero Fees After Market Losses

Shanghai Power Asset apologizes to investors upset by losses Case adds to Chinese quants’ setbacks from stocks rally

QUOTE

...

FuRao Arbitrage No. 3 mainly uses a strategy that exploits differences in implied volatility among options with different strike prices or expiration dates. Power Asset uses machine learning models to adjust its entry and exit points, according to PaiPaiWang.

The fund fell in each of the past four weeks, with combined losses of more than 16%, according to performance data seen by Bloomberg News. During the period, the CSI 300 Index jumped as much as 33% before retreating by up to 11% from the Oct. 8 peak.

Bankers Do Anything It Takes to Grab a Slice of Rare Buyout Deal CD&R’s unhappy Morrisons experience hasn’t stopped investment bankers from lining up in droves to get a piece of its debt-financing deal for Sanofi’s consumer drug offshoot.

Atlas of Finance — a visual aid to the global money maze An eclectic and ambitious series of maps, graphs and diagrams helps disclose the locations of hidden riches

These rumors are false. Samsung does not have a competitive 3nm/2nm process nor does it have the proper ecosystem. Intel 18A has a much better chance for the NOT TSMC business than Samsung. That is what I am hearing inside the ecosystem.

Samsung Foundry has burned many bridges with the leading edge customers which includes Qualcomm and Nvidia. Now that they are flying first class with TSMC I do not see them going back to Samsung. A good example is AMD. AMD used GlobalFoundries 14nm which was sourced from Samsung and from what I understand Samsung handled overflow business for AMD. Yet AMD has not engaged with Samsung since moving to TSMC in 2018. It really is all about trust to deliver the wafer on time and at respectable yields. Both of which Samsung has failed at with 5/4nm, and 3/2nm. I also know that the relationship between GF and Samsung for the 14nm process was not shall we say smooth which negatively affected AMD.

As it stands today I know of ZERO customers outside of Korea using Samsung 3/2nm. If I am wrong let me know because I do keep track of design starts. Keeping track of 3nm design starts turned out to be pretty easy since they were all at TSMC.

TSMC Expected To Bump Up 3nm & CoWoS Pricing Moving Into 2025 Amid Massive Market Demand & Supply Chain Bottlenecks

QUOTE

The Taiwan giant TSMC is reportedly considering raising prices for its in-demand 3nm and CoWoS processes in an attempt to cope with the gigantic demand.

TSMC Plans To Implement 3nm & CoWoS Price Increase Given The Tremendous Demand From The AI Markets

In the modern-day AI markets, TSMC is playing a pivotal role when it comes to providing the essentials in the realm of semiconductors, and the company's cutting-edge nodes are in significant demand from the markets. Companies like NVIDIA and AMD have their mainstream AI solutions utilizing TSMC's 3nm process, along with its CoWoS derivatives, so for the Taiwan giant, keeping up with the demand has been quite tricky, which is why a report from Ctee has disclosed that TSMC plans to bump up pricing of 3nm and CoWoS, citing that this move will maintain supply chain balance.

The report says that TSMC plans to implement the price hike in 2025 and has already received approval from NVIDIA, so ultimately, the price change will affect the whole supply chain. It is said that TSMC 3nm pricing is expected to receive a bump of up to 5%, while CoWoS packaging could rise by 10% to 20%, depending upon how the Taiwan giant expands production capacity for its advanced packaging processes.

TSMC has a strong future moving ahead, given that not only has the company "monopolized" the semiconductor markets, but with gigantic demand from the AI segment, TSMC has its production lines booked in the next year as well. The supply chain bottleneck is forcing the company to upscale existing facilities, so a price bump makes sense here.

Morgan Stanley says that TSMC's gross margins are expected to soar moving into 2025, ultimately translating into solid earnings for the company. In a recent coverage, we reported on how TSMC's 3nm and 5nm nodes are responsible for more than 52% of the company's revenue in Q3 2024, which shows the significance of these processes for the Taiwan giant. Apart from this, it is said that TSMC's next-gen 2nm will be much more disruptive in terms of market demand, so the future of TSMC and the semiconductor markets is indeed bright.

What is "accessible luxury"? Even the FTC doesn't understand...

Bloomberg Businessweek | Buying Power

What Everyone Gets Wrong About Luxury Handbags The scuttled merger between the owners of Coach and Michael Kors tells us the FTC doesn’t understand “accessible luxury.”

Oct 22 2024, 04:14 PM

Oct 22 2024, 04:14 PM

Quote

Quote

0.2195sec

0.2195sec

0.76

0.76

7 queries

7 queries

GZIP Disabled

GZIP Disabled