QUOTE(adccs @ May 3 2019, 10:01 AM)

But i don't think is possible to open a/c for non-bumi, but at least could joint name..if possible or something to that effect.

noonly individual name if adult

if child yeah can join name as parent

Ultimate Discussions of ASB1/2-Financing, questions/comments/criticisms welcome

|

|

May 3 2019, 10:05 AM May 3 2019, 10:05 AM

|

Senior Member

3,129 posts Joined: Jun 2011 From: Melaka/Kuching |

QUOTE(adccs @ May 3 2019, 10:01 AM) But i don't think is possible to open a/c for non-bumi, but at least could joint name..if possible or something to that effect. noonly individual name if adult if child yeah can join name as parent |

|

|

|

|

|

May 3 2019, 10:07 AM

Show posts by this member only | IPv6 | Post

#222

|

Senior Member

1,099 posts Joined: Jan 2019 |

QUOTE(wild_card_my @ May 2 2019, 11:56 PM) Yes you could! That is just cash investment, with a lump sum amount. Not everyone has the opportunity to do this, if you have RM200k to spare, that is good for you. May i know what app / website are you using to calculate? Mind sharing?As for the duration, using a simple capital appreciation would do. 332 months to get your RM200k to become RM1m at 6% p.a.  Now just use NRIC and thumbprint to withdraw. No need books/certificates anymore You are a sharp one - I mean it. You are asking the right questions. No, they do not publicly disclose the fund's Net-Asset-Value. The SC knows about it, but they have their reasons to not disclose them, I can probably speculate - you may come to the same conclusion anyway. In any case, at the point of purchase (say, today) you would be paying RM1 per share, but you do not know the actual value of the share. Could it be RM0.80 per share (which means you are over paying) or is it RM1.20 per share (which means you are underpaying, which is good)? |

|

|

May 3 2019, 10:13 AM

|

Senior Member

6,562 posts Joined: Jan 2003 From: Kuala Lumpur |

QUOTE(adccs @ May 3 2019, 10:01 AM) But i don't think is possible to open a/c for non-bumi, but at least could joint name..if possible or something to that effect. If you are non bumi but married to a Bumi, yes you can do a joint ASB-financing account with your spouseYou supply the income statements, spouse supply the account. She would be the main applicant QUOTE(JoeK @ May 3 2019, 10:07 AM) May i know what app / website are you using to calculate? Mind sharing? Android app, "financial calculator" |

|

|

May 3 2019, 10:32 AM

|

Junior Member

74 posts Joined: Jan 2013 |

So let's say if your total cap is RM250k with RM50k being your softcap. Earlier in the year you need some cash and you withdraw RM50k from your account, then next year after bonus for example, can you put RM50k back into your account which would bring your total cap back to RM250k?

|

|

|

May 3 2019, 11:04 AM

|

Senior Member

758 posts Joined: Aug 2008 |

parking

This post has been edited by mousqy: May 3 2019, 11:04 AM |

|

|

May 3 2019, 11:14 AM

|

|

Newbie

32 posts Joined: Jan 2018 |

QUOTE(HolySatan @ May 2 2019, 08:01 PM) ASB > AHB > ASB2 > TH TH is crap nowadays, better park at FD instead... TH just park minimum amount for haji and that's it. If already go for haji just close it down instead |

|

|

|

|

|

May 3 2019, 11:20 AM

|

Newbie

25 posts Joined: Oct 2018 |

U can make utube video series abt this since its valid argument, opinion on risks etc.. sure many ppl comments n monetise it lolz

|

|

|

May 3 2019, 11:55 AM

|

Junior Member

405 posts Joined: Oct 2007 |

good thread, TT!

|

|

|

May 3 2019, 01:54 PM

Show posts by this member only | IPv6 | Post

#229

|

Senior Member

2,731 posts Joined: Dec 2005 From: Hell |

wild_card_my

Where is the asb soft cap? Thanks  |

|

|

May 3 2019, 02:31 PM

|

Junior Member

51 posts Joined: Mar 2013 |

wild_card_my

Sent you PM on ASB loan inquiry. Do have a look and feedback. TQ |

|

|

May 3 2019, 02:55 PM

|

|

Senior Member

6,562 posts Joined: Jan 2003 From: Kuala Lumpur |

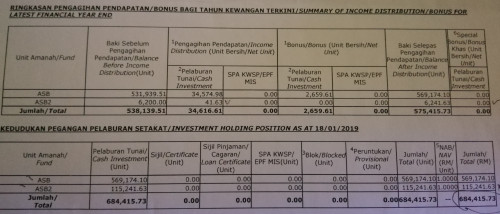

QUOTE(lagista @ May 3 2019, 11:20 AM) U can make utube video series abt this since its valid argument, opinion on risks etc.. sure many ppl comments n monetise it lolz I have made a few, will continue to make them.QUOTE(robeng @ May 3 2019, 11:55 AM) good thread, TT! Thank youQUOTE(Mooneyes @ May 3 2019, 01:54 PM) wild_card_my This is not it. This is a Summary of distribution. I can't remember which statement it was, but my client printed it out and we managed to see it. Where is the asb soft cap? Thanks QUOTE(sanwaltz @ May 3 2019, 02:31 PM) wild_card_my Sorry for the late reply. Just got back to you.Sent you PM on ASB loan inquiry. Do have a look and feedback. TQ |

|

|

May 3 2019, 02:59 PM

|

|

Senior Member

6,562 posts Joined: Jan 2003 From: Kuala Lumpur |

QUOTE(4Z7 @ May 3 2019, 10:32 AM) So let's say if your total cap is RM250k with RM50k being your softcap. Earlier in the year you need some cash and you withdraw RM50k from your account, then next year after bonus for example, can you put RM50k back into your account which would bring your total cap back to RM250k? You got the idea!But what you mean to say in the last part is actually "can you put RM50k back into your account which would bring your total HOLDING back to RM250k?" And the answer is yes. Your total capping will NEVER decrease. Your holding may increase or lower as you deposit and withdraw you cash investments (including the received distributions), but the capping remain as it was, until it gets increased again. Hope this is clear, but if it isn't I guess... I would have to make a video about this to explain it using pen and paper  QUOTE(80ers @ May 3 2019, 11:14 AM) TH is crap nowadays, better park at FD instead... I agree. I would avoid funds that are always in the news for the wrong reasons.TH just park minimum amount for haji and that's it. If already go for haji just close it down instead |

|

|

May 3 2019, 03:11 PM

|

|

Junior Member

74 posts Joined: Jan 2013 |

QUOTE(wild_card_my @ May 3 2019, 02:59 PM) You got the idea! This is clear enough, thank you. For the benefit of others, you may want to make a video about this though But what you mean to say in the last part is actually "can you put RM50k back into your account which would bring your total HOLDING back to RM250k?" And the answer is yes. Your total capping will NEVER decrease. Your holding may increase or lower as you deposit and withdraw you cash investments (including the received distributions), but the capping remain as it was, until it gets increased again. Hope this is clear, but if it isn't I guess... I would have to make a video about this to explain it using pen and paper I agree. I would avoid funds that are always in the news for the wrong reasons.  |

|

|

|

|

|

May 3 2019, 03:12 PM

|

|

Senior Member

6,562 posts Joined: Jan 2003 From: Kuala Lumpur |

QUOTE(4Z7 @ May 3 2019, 03:11 PM) This is clear enough, thank you. For the benefit of others, you may want to make a video about this though I thought I would. But my schedule  Feel free to ask anything here though, I enjoy responding to them |

|

|

May 3 2019, 03:16 PM

|

Senior Member

1,152 posts Joined: Jun 2007 From: Kuala Lumpur |

QUOTE(wild_card_my @ May 2 2019, 11:56 PM) Yes you could! That is just cash investment, with a lump sum amount. Not everyone has the opportunity to do this, if you have RM200k to spare, that is good for you. Firstly, thanks for the compliment. I also greatly appreciate the discussions and information that you shared. Thanks again.As for the duration, using a simple capital appreciation would do. 332 months to get your RM200k to become RM1m at 6% p.a. Now just use NRIC and thumbprint to withdraw. No need books/certificates anymore You are a sharp one - I mean it. You are asking the right questions. No, they do not publicly disclose the fund's Net-Asset-Value. The SC knows about it, but they have their reasons to not disclose them, I can probably speculate - you may come to the same conclusion anyway. In any case, at the point of purchase (say, today) you would be paying RM1 per share, but you do not know the actual value of the share. Could it be RM0.80 per share (which means you are over paying) or is it RM1.20 per share (which means you are underpaying, which is good)? I usually don't take things at face value as I believe in finding out the truth and understanding how things work. I consider myself an armchair economist and a hobby investor. Frankly, I have been discussing this ASB financing and PNB offerings with my financial buddies infrequently during our get-togethers. With your confirmation of their not revealing the NAV of ASB, it seems like it works like a high coupon sovereign bond. If the fund managers can continue providing the returns, then everything is good. I'm just wary of the fact that if they can't, and things go south, the fallout may be devastating to our economy especially our ringgit. High returns mean nothing if there is no value to the currency. Some risks that I see. 1) PNB has 98%(!) invested locally, with 70% in the stock market and equities, representing 10% of the market cap of our local stock market! (Source: https://www.theedgemarkets.com/article/pnbs...e-grows-rm279b). If our economy slows down and if ASB is unwilling to reduce their distributions, the only way is for BNM to increase liquidity which will have an adverse effect on our currency. The fund size is RM279b (as of Mar 2018), which is more than half the size of BNM's international reserves (USD1=RM4.14). As you and I know, our stock market performance is practically flat past 5 years (excl. dividends) and is even underperforming regionally YTD. That's why after seeing your table of the distribution history, warning bells went off in my mind. Either the fund managers are oracles that can time the market, trading with insider info or something fishy is going on. I tend to believe the latter two. 2) The push for ASB financing. This is increasing liquidity by borrowing from banks and putting the faith on the people. In other words, use future money now from private banks, in the faith that the people will work to repay it and get rewarded. This is all good except that there is crazy pressure on PNB to continue delivering market-beating returns. And since ASB is so liquid, it could also be its downfall in case of a bank run of sorts. And if PNB can sorta "guarantee" these kinda returns, why don't they cut out the middle man (aka bumis) and just borrow from private banks? Yeah, this will then look bad on the affirmative action part, but it just seems inefficient to me as an economic-minded person. This is the main reason we (my friends and I) feel there must be some risk we don't know. All in all, just my two cents. I really hope that everything is above board and PNB is truly doing an amazing job (nothing short of a miracle) to have such market beating returns year in year out (for 40 years mind you). I, myself have a small fortune in ASM and ASW2020 but the big bulk of my investments are in the global markets (non RM). |

|

|

May 3 2019, 04:21 PM

Show posts by this member only | IPv6 | Post

#236

|

|

Newbie

25 posts Joined: Oct 2018 |

Let say borrow RM100k for 10 yrs, repayment around RM2k monthly (example)

So just standby RM24k-48k, auto debit for 1 yr or 2 yrs, next 8 yrs just use interest to pay the rest of loan Possible issit? Let money pay by itself for long term So what is the ideal tenure for RM200k actually so as not too burden (prefer RM2-3k monthly)...15 yrs ? Btw grace period/cut off is 2 yrs before its worth the interest used for loan repayment rite ? |

|

|

May 3 2019, 08:36 PM

|

|

Senior Member

6,562 posts Joined: Jan 2003 From: Kuala Lumpur |

QUOTE(kelvinlym @ May 3 2019, 03:16 PM) Firstly, thanks for the compliment. I also greatly appreciate the discussions and information that you shared. Thanks again. ASB has recently changed it fund category from EQUITY to MIXED ASSET, although I have not see much changes reflected in its holdings. Perhaps the returns wont be as aggressive as it had been in the past. I usually don't take things at face value as I believe in finding out the truth and understanding how things work. I consider myself an armchair economist and a hobby investor. Frankly, I have been discussing this ASB financing and PNB offerings with my financial buddies infrequently during our get-togethers. With your confirmation of their not revealing the NAV of ASB, it seems like it works like a high coupon sovereign bond. If the fund managers can continue providing the returns, then everything is good. I'm just wary of the fact that if they can't, and things go south, the fallout may be devastating to our economy especially our ringgit. High returns mean nothing if there is no value to the currency. Some risks that I see. 1) PNB has 98%(!) invested locally, with 70% in the stock market and equities, representing 10% of the market cap of our local stock market! (Source: https://www.theedgemarkets.com/article/pnbs...e-grows-rm279b). If our economy slows down and if ASB is unwilling to reduce their distributions, the only way is for BNM to increase liquidity which will have an adverse effect on our currency. The fund size is RM279b (as of Mar 2018), which is more than half the size of BNM's international reserves (USD1=RM4.14). As you and I know, our stock market performance is practically flat past 5 years (excl. dividends) and is even underperforming regionally YTD. That's why after seeing your table of the distribution history, warning bells went off in my mind. Either the fund managers are oracles that can time the market, trading with insider info or something fishy is going on. I tend to believe the latter two. 2) The push for ASB financing. This is increasing liquidity by borrowing from banks and putting the faith on the people. In other words, use future money now from private banks, in the faith that the people will work to repay it and get rewarded. This is all good except that there is crazy pressure on PNB to continue delivering market-beating returns. And since ASB is so liquid, it could also be its downfall in case of a bank run of sorts. And if PNB can sorta "guarantee" these kinda returns, why don't they cut out the middle man (aka bumis) and just borrow from private banks? Yeah, this will then look bad on the affirmative action part, but it just seems inefficient to me as an economic-minded person. This is the main reason we (my friends and I) feel there must be some risk we don't know. All in all, just my two cents. I really hope that everything is above board and PNB is truly doing an amazing job (nothing short of a miracle) to have such market beating returns year in year out (for 40 years mind you). I, myself have a small fortune in ASM and ASW2020 but the big bulk of my investments are in the global markets (non RM). 2. As for the "market-beating" returns, it is clear if we look at the annualized returns of ASB, they are not the market beater. Other unit trusts can beat them but due to the fact that their NAV is declared each day, thus the changes of NAV/unit on a daily basis, everyone's returns would be different from each other, even if the entry and exits are made just a single day apart QUOTE(lagista @ May 3 2019, 04:21 PM) Let say borrow RM100k for 10 yrs, repayment around RM2k monthly (example) Yeah, this is called the auto rolling method. You would not end up with RM1.8M as I mentioned in the first thread, but in the end you would still end up with with "free" money. I dislike this method since you are incurring opportunity cost going forwardSo just standby RM24k-48k, auto debit for 1 yr or 2 yrs, next 8 yrs just use interest to pay the rest of loan Possible issit? Let money pay by itself for long term So what is the ideal tenure for RM200k actually so as not too burden (prefer RM2-3k monthly)...15 yrs ? Btw grace period/cut off is 2 yrs before its worth the interest used for loan repayment rite ? There are no hard and fast rule about the best time to cancel the loan. You have to look at: 1. the best current market interest rate over the effective rate you are paying now 2. the capital that you would have been returned to you once you close the loan account. This capital can be further invested as cash investment |

|

|

May 3 2019, 08:38 PM

|

Senior Member

2,003 posts Joined: Mar 2009 |

So you can increase your financing but can you reduce it?

Lets say take 100k loan then you want to reduce it 50k some years later, is that possible? How much can you salvage? |

|

|

May 3 2019, 08:48 PM

|

Senior Member

1,062 posts Joined: May 2008 |

On top of the interest, do banks charge for insurance and sijil asb?

|

|

|

May 3 2019, 08:49 PM

|

|

Newbie

3 posts Joined: Sep 2017 |

Its just one of the money u can commit.....

|

|

Topic ClosedOptions

|

| Change to: |  0.0244sec 0.0244sec

0.60 0.60

6 queries 6 queries

GZIP Disabled GZIP Disabled

Time is now: 11th December 2025 - 06:53 AM |

Quote

Quote