May 7 2021, 12:40 PM

May 7 2021, 12:40 PM

QUOTE(ryan18 @ May 7 2021, 12:00 PM)

My prudential medical ILP bought 5 years ago the reprice will happen this year from 132 per month to 150 per month about 13% increase seems reasonable right?

looking at the post below...looks like 13% increase per year

so do take note of it and be expected of it....your premium will rise 100% in the next few years....thus do proper budget planning in advance and avoid unnecessary stress

QUOTE(lifebalance @ May 7 2021, 12:26 PM)

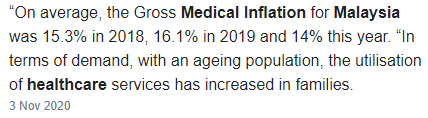

Medical inflation keep increasing, if insurance company don't keep up with the inflation, how to pay for all the claims?

Seems pretty normal to me adjusted to the inflation.

Quote

Quote

your argument applies to all things that has monetary value, inflation isn't just applied to insurance. Even your property / stocks / FD / UT is subject to inflation.

your argument applies to all things that has monetary value, inflation isn't just applied to insurance. Even your property / stocks / FD / UT is subject to inflation. 0.0188sec

0.0188sec

0.53

0.53

6 queries

6 queries

GZIP Disabled

GZIP Disabled