QUOTE(alexkos @ Feb 26 2019, 10:15 PM)

Bacalah “你能吗" in the attached pdf. Good luck!

so US total bond market index fund is replaced by Amanah saham?? is Amanah Saham better than bond market index?

[DIY] S&P 500 Index w/ 0.07% Annual Fee, Buy the best companies in the world

|

|

Oct 30 2019, 06:47 PM Oct 30 2019, 06:47 PM

Return to original view | Post

#1

|

Senior Member

1,917 posts Joined: Sep 2012 |

QUOTE(alexkos @ Feb 26 2019, 10:15 PM) Bacalah “你能吗" in the attached pdf. Good luck! so US total bond market index fund is replaced by Amanah saham?? is Amanah Saham better than bond market index? |

|

|

|

|

|

Oct 30 2019, 06:58 PM

Return to original view | Post

#2

|

|

Senior Member

1,917 posts Joined: Sep 2012 |

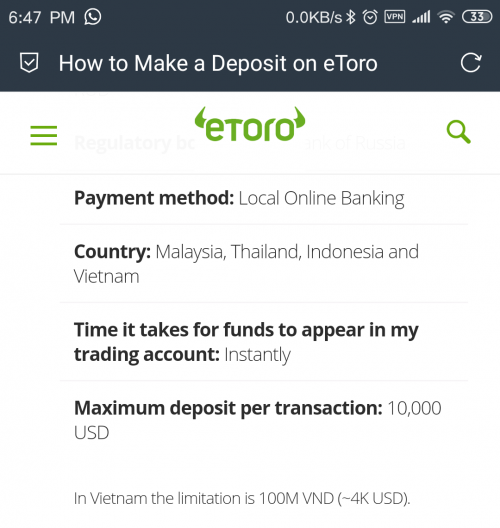

QUOTE(dwRK @ Oct 18 2019, 07:14 PM) Any etoro ppl here?... is etoro better than ibkr? Etf 0.09% commission US stocks 0% commission Withdrawal fee $25 |

|

|

Oct 30 2019, 07:02 PM

Return to original view | Post

#3

|

|

Senior Member

1,917 posts Joined: Sep 2012 |

QUOTE(alexkos @ Oct 30 2019, 06:59 PM) Can try ambank bond fund also. Asnb is quite unique for Malaysian. U won't lose principal in Asnb fixed price, that fulfills one major point of bond (security) but bond prices can go up in value, ASNB cannot.  so the potential upside for bonds is higher, no? during recessions when stocks go down, bond prices go up. But ASNB doesn't, dividend might actually go down. |

|

|

Nov 4 2019, 06:51 PM

Return to original view | Post

#4

|

|

Senior Member

1,917 posts Joined: Sep 2012 |

there are so many S&P500 ETF domiciled in Ireland.

Why TS chose that one specifically? |

|

|

Nov 5 2019, 12:35 PM

Return to original view | Post

#5

|

|

Senior Member

1,917 posts Joined: Sep 2012 |

QUOTE(roarus @ Nov 5 2019, 10:39 AM) More concise answer - decision would be depending on: say, for simplicity sake, i. How much one would periodically like to invest (CapTrader vs TradeStation Global decision) ii. If one readily holds EUR/GBP/USD currency and can transfer over (EUR/GBP/USD denominated fund decision) iii. If one believes S&P500 will continue to outperform others like Nikkei and Euro indexes (just throwing a curveball) 1. monthly USD 1k. 2. holds readily USD and EUR. For now, I avoid GBP. Really don't know what's gonna happen after Brexit. 3. I think I'll choose S&P500 and Euronext 100. Ratio 9:1. |

|

|

Nov 5 2019, 06:44 PM

Return to original view | Post

#6

|

|

Senior Member

1,917 posts Joined: Sep 2012 |

QUOTE(roarus @ Nov 5 2019, 05:50 PM) 1. monthly USD 1k. Thanks for the info! TradeStation Global (https://www.tradestation-international.com/pricing/): USD denominated: 0.12% or minimum USD1.91-1.95 (GBP1.5 equivalent) ~USD1,590 before 0.12% exceeds GBP1.5 equivalent EUR denominated: 0.12% or minimum EUR1.71 ~EUR1425 before 0.12% exceeds EUR1.71 CapTrader (https://www.captrader.com/en/account/commissions/) 0.1% or EUR2 - 4 depending on exchange. No mention of USD denominated listed on London Stock Exchange 2. holds readily USD and EUR. For now, I avoid GBP. Really don't know what's gonna happen after Brexit. Both can accept USD (Citibank NY) or EUR (Citibank Germany). Doesn't matter if you have a USD S&P500 fund mixed with EUR S&P500 fund. Once you've paid for units of a fund you're holding the value the underlying companies instead of denomination currency. If you're OCD enough you can spend USD2 (TradeStation) to convert and buy only 1 denomination fund. CapTrader conversion fee depends on which currency you're selling (https://www.captrader.com/en/account/commissions) 3. I think I'll choose S&P500 and Euronext 100. Ratio 9:1. Won't comment on allocation, everyone has a preference/region specific bet. You can go crazy with the ETF screener here: https://www.justetf.com/en/find-etf.html?groupField=index From there you can copy the ISIN code and look it up in https://www.investing.com and check out the cross listing on other exchanges + other info like denomination and volume If it's domiciled in Ireland + physical replication + issued by iShares/Vanguard/SPDR it's safe enough. I have personal preference of accumulating funds  |

|

|

|

|

|

Nov 5 2019, 06:47 PM

Return to original view | Post

#7

|

|

Senior Member

1,917 posts Joined: Sep 2012 |

Btw, have we established that 15% WHT for Irish domiciled S&P500 ETF is better than the US ETF for us non-US residents??

QUOTE(roarus @ Nov 5 2019, 05:50 PM) If you're OCD enough you can spend USD2 (TradeStation) to convert and buy only 1 denomination fund. CapTrader conversion fee depends on which currency you're selling (https://www.captrader.com/en/account/commissions) 3. I think I'll choose S&P500 and Euronext 100. Ratio 9:1. Won't comment on allocation, everyone has a preference/region specific bet. You can go crazy with the ETF screener here: https://www.justetf.com/en/find-etf.html?groupField=index From there you can copy the ISIN code and look it up in https://www.investing.com and check out the cross listing on other exchanges + other info like denomination and volume If it's domiciled in Ireland + physical replication + issued by iShares/Vanguard/SPDR it's safe enough. I have personal preference of accumulating funds QUOTE(dwRK @ Nov 5 2019, 06:43 PM) Euronext 100 should be all in EUR... I am sadly quite OCD about the currency of the ETF.  ...and If super OCD... then need to consider hedging currency drop also... assuming wanna repat funds lah...  |

|

|

Nov 5 2019, 10:17 PM

Return to original view | Post

#8

|

|

Senior Member

1,917 posts Joined: Sep 2012 |

QUOTE(Yggdrasil @ Nov 5 2019, 08:39 PM) 1) Buying S&P 500 in Euro vs USD - aka buying the same asset using 2 different currencies.[/size] for now, I'm thinking of liquidating in USD or JPY or EUR. ETF currency does not matter because it is the NAV of the asset which matters. However, it does matter if the ETF managers hold cash. Almost all hold a small % of cash depending on the currency. Furthermore, you should be more concerned about the exchange rate when you decide to liquidate, not when you buy. As you average down, the currency fluctuations will cause you to buy more units when it depreciates and buy less when it appreciates. In the long run, you will return to the 'average' exchange rate and it only matters when you sell. When you sell, the exchange will decide whether you earn more or less. This is very important because it will decide whether your compounded return is higher or lower. Because of exchange rate, you may make a gain 3% gain in USD terms but a 2% loss in MYR terms. E.g. 1 USD : 4 MYR, you convert RM1000 into $250 to invest. (Just once, no dollar cost average) 1 year later, your $250 grew by 6% p.a. for 2 years to $280.90 [250 x 1.06^2] You decide to liquidate, MYR appreciated against USD. 1 USD : 3.5 MYR. You get back RM983.15 [$280.90 x 3.5]. You made a loss. Why loss? You put in RM1000 and get back RM983.15. Your return p.a. is -0.84% [(983.15/1000)^(1/2)-1]. Usually by a few % so it's best to liquidate when MYR is weak not when it is strong. Technically, you should buy more S&P 500 when MYR is strong not weak. If on the other hand, MYR depreciates when you liquidate and convert back: Say, 1 USD : 4.5 MYR. Your investment after 2 years is still $280.90 remember? But when you convert back, you get RM1264.05 [$280.90 x 4.5] Your return p.a. is 12.4% [(1264.05/1000)^(1/2)-1]. See now currency is more important when you liquidate? yeah, my question referred to the 1st scenario, different currency of the same asset class. ok. So the base currency doesn't matter. Just the asset.  QUOTE(roarus @ Nov 5 2019, 08:44 PM) You really shouldn't be. If you go to the airport and buy a box of chocolate and it costs GBP1 / USD1.3 / EUR1.15 it doesn't matter which currency you pay for it - in the end you end up with a box of chocolates, not GBP or USD or EUR. when I'm offered to pay either GBP1 / USD1.3 / EUR1.15, I would look through the app and check. If the exchange rate is GBP 1 / USD 1.5 / EUR 1.10, I'd pay with USD.  |

|

|

Nov 5 2019, 10:47 PM

Return to original view | Post

#9

|

|

Senior Member

1,917 posts Joined: Sep 2012 |

questions about WHT, I got confused.

A Malaysian citizen buying Irish domiciled ETF, WHT is 15%. What if, a US citizen buying Irish domiciled ETF, is the WHT 15% or 30%? A Japanese citizen buying Irish domiciled ETF, is the WHT 15% or 30%? |

|

|

Nov 5 2019, 11:05 PM

Return to original view | Post

#10

|

|

Senior Member

1,917 posts Joined: Sep 2012 |

QUOTE(dwRK @ Nov 5 2019, 11:01 PM) It's not citizenship but tax residency...and tax treaty or not but we pay 15% because it's in Ireland, no? if US residents bought irish domiciled ETF, the WHT should also be 15%, no? |

|

|

Nov 6 2019, 12:43 PM

Return to original view | Post

#11

|

|

Senior Member

1,917 posts Joined: Sep 2012 |

when you guys buy ETF, do you buy 1 unit or can you buy a fixed amount currency of ETF?

say, 500 EUR. Then you'll receive 1.xxxxx unit ETF?? How do you sell then? |

|

|

Nov 6 2019, 01:03 PM

Return to original view | Post

#12

|

|

Senior Member

1,917 posts Joined: Sep 2012 |

QUOTE(alexkos @ Nov 6 2019, 12:49 PM) 1unit but I thought ppl kept saying invest a fixed sum of money and DCA?? then it's not possible to invest a fixed sum? |

|

|

Nov 6 2019, 01:17 PM

Return to original view | Post

#13

|

|

Senior Member

1,917 posts Joined: Sep 2012 |

QUOTE(Yggdrasil @ Nov 6 2019, 01:11 PM) Not sure what you meant but.. each time only buy 1 unit ... life is so depressing. Example you have RM1000 to invest every month. QQQ is USD 200 per unit today. 1 USD: 4.15 MYR. You convert and get USD 240.96. You can buy 1 unit at USD 200. Means you left USD 40.96 not yet invest. You can use this money to top up with next month. Like StashAway, you can have 1.231241325 unit of an ETF, I think. No? ok, I thought DCA means a fixed sum every month; but since we cannot buy ETFs in fractions, then I guess cannot invest a fixed sum every time. |

|

|

|

|

|

Nov 6 2019, 04:14 PM

Return to original view | Post

#14

|

|

Senior Member

1,917 posts Joined: Sep 2012 |

QUOTE(Chounz @ Nov 6 2019, 02:42 PM) I think you didn't get my message, the dividend for this ETF will be reinvested in the ETF again. This is not correct lo .... the SXR8 that we talked about also auto reinvest, still got withholding tax. Meaning, there is no dividend from this ETF, hence, it should not subject to any WHT. Unless you are saying there is WHT attach to the capital gain subsequently when dispose the ETF. If don't want WHT, then don't declare dividend like Warren B. If declare, sure tax, doesn't matter auto re-invest or not. QUOTE Reinvesting dividends is the process of automatically using cash dividends to purchase additional stocks of the same company. If you choose to reinvest your dividends, you still have to pay taxes as though you actually received the cash. Source: Investopedia |

|

|

Nov 6 2019, 04:53 PM

Return to original view | Post

#15

|

|

Senior Member

1,917 posts Joined: Sep 2012 |

QUOTE(Yggdrasil @ Nov 6 2019, 04:36 PM) On the other hand, if you buy a US-domiciled ETF, dividends are paid to you. what if you buy US-domiciled ETF but auto reinvest (DRIP)?? |

|

|

Nov 6 2019, 08:36 PM

Return to original view | Post

#16

|

|

Senior Member

1,917 posts Joined: Sep 2012 |

sigh.... now I'm also very confused liao ..... nevermind lah....

by the way, if buy SXR8, then the intraday movement is not much since half of the time, it doesn't overlap with the NYSE? |

|

|

Nov 7 2019, 02:52 PM

Return to original view | Post

#17

|

|

Senior Member

1,917 posts Joined: Sep 2012 |

............

This post has been edited by moosset: Nov 7 2019, 03:00 PM |

|

|

Nov 7 2019, 03:13 PM

Return to original view | Post

#18

|

|

Senior Member

1,917 posts Joined: Sep 2012 |

QUOTE(alexkos @ Nov 7 2019, 03:08 PM) Careful bro must post content ya... If not mod cari I for justification I kantoi. I changed my mind about my post but there's no delete button.BTW those interested in more global index than sp500 can lookup EIMI... Emerging market exposure. But TER 0.18% I dun like.... |

|

|

Nov 8 2019, 07:28 AM

Return to original view | Post

#19

|

|

Senior Member

1,917 posts Joined: Sep 2012 |

Yggdrasil

any QQQ denominated in EUR? |

|

|

Nov 9 2019, 11:59 PM

Return to original view | Post

#20

|

|

Senior Member

1,917 posts Joined: Sep 2012 |

QUOTE(dwRK @ Nov 9 2019, 09:45 PM) Yes high yield products. I briefly saw a few usd etfs that's 7-10% so was thinking the dividend more than cover the loan 3%, 1.5% means what?? Isn't this rate compounded daily?The second point is instead of taking a usd margin loan at 3%... I take a eur loan at 1.5% and use that to buy usd... so effectively a usd loan at 1.5%. If usd strengthen its in my favor because I'm holding usd. Sounds simple so I don't know if I'm missing something tbh... that 7-10% is a yearly dividend yield, no? How to cover? |

| Change to: |  0.0525sec 0.0525sec

0.19 0.19

7 queries 7 queries

GZIP Disabled GZIP Disabled

Time is now: 27th November 2025 - 09:13 PM |

Quote

Quote