Mar 15 2017, 10:18 AM

Mar 15 2017, 10:18 AM

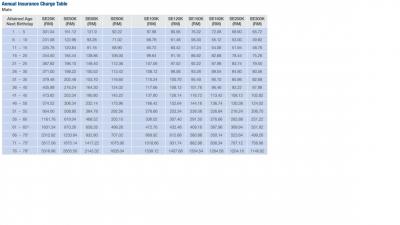

Hi Gurus, not sure if this is relevant question, no intention to compare different provider, but there's been one single question that troubling me.... Just comparison sake let say between medical plan from GE and Prudential e.g. Smartmedic + Smartmedic Extender vs PruValue Med, let say taking example of non-smoking male, NB 41, R&B 300, expiry age 80, Class 2 ..... When consider in-par plan e.g. GE with SM300 + SE300K while Prudential with Med Point 1.5 mil & med saver 300, just comparing the premium for ONLY medical card portion, what is the reason that difference could go way beyond two or even three fold.

My limited insurance knowledge, but could all insurance guru out there enlighten me what's the catch / distinct difference to look out for in considering such plan with hefty premium differences. Two plans looks almost identical (main benefit per say) from my limited knowledge.

Thank you so much.

Insurance Talk V4!, Anything and everything about Insurance

Quote

Quote

0.0212sec

0.0212sec

0.41

0.41

7 queries

7 queries

GZIP Disabled

GZIP Disabled