Aug 26 2021, 12:32 PM

Aug 26 2021, 12:32 PM

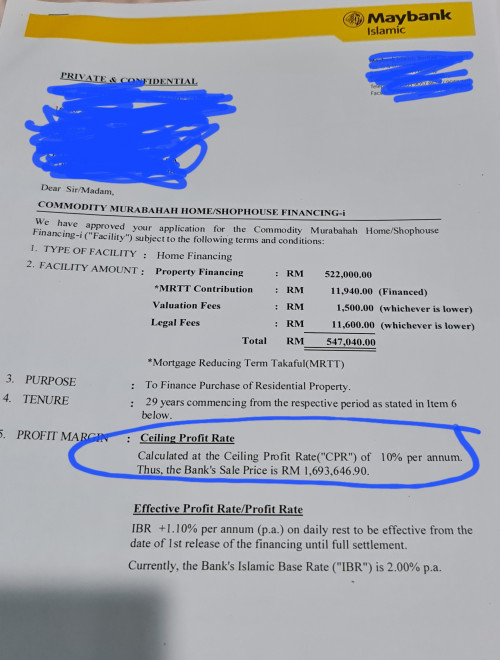

QUOTE(stevendefool @ Aug 26 2021, 10:51 AM)

Dear sifus, would like your input on the following matter.

Father wants to remortgage a property which is under his name. However, he’s retired and no more monthly income.

I’m currently working and have no commitments. Can me and my father do a joint loan where I will be responsible in paying the monthly repayments while the property is still under his name?

Would this be considered a 3rd party loan?

Father age? if above age 65, sorry your father tak boleh become borrower but he can still be a "KYC" customerFather wants to remortgage a property which is under his name. However, he’s retired and no more monthly income.

I’m currently working and have no commitments. Can me and my father do a joint loan where I will be responsible in paying the monthly repayments while the property is still under his name?

Would this be considered a 3rd party loan?

this

reason for remortgaging? renovation purposes? no commitment is actually not a good thing as bank do not know your repayment records, but it is not a bad thing la... with a low cash out ratio, you might still have a chance at approval

yes, this is a 3rd party loan

Quote

Quote

0.0648sec

0.0648sec

0.72

0.72

7 queries

7 queries

GZIP Disabled

GZIP Disabled