With the rising cost of living due to GST, your medical cost will just follow to go up!!

Have you prepare enough in case of any emergency need for medical?? Please don't forget there is a deposit before admission to hospital.

ALLIANZ Medical Card- We take care of your hospital bills for your family members...

With Allianz the protection starts from as low as RM 150 monthly**

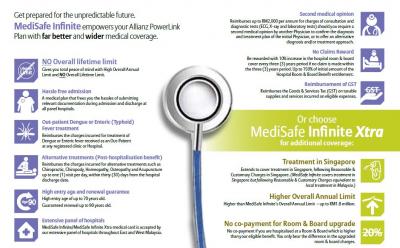

ALLIANZ Medical Card with No Lifetime Limit and High Annual Limit up to RM1.8mil with affordable premium. The Benefit are as:

- No Overall Lifetime limit - Overall Annual limit up to RM1.8mil - No Co-Insurance and no deductible - Guaranteed Renewal Coverage up to 91 years old with no additional cost - High entry age of up to 70 years old - Out-patient benefits for emergency treatment of accidents, cancer as well as kidney dialysis. (As Charge, No lifetime limit) - Refund of unutilized Room and Board entitlement upon hospitalisation - No claim reward for increase of R&B - Outpatient Dengue and Enteric (Typhoid) Fever Treatment Claim - Second Medical Opinion - comprehensive benefit ranging from reimbursement for specific pre and post hospitalisation treatments to home nursing care and ambulance fees - Hassle-free hospital admission and discharge from Our approved network of hospitals with your Medical Card (up to 46 Panel Hospitas in KL-Selangor) And etc..

**PowerLink product comes with :

Premium Medical Card Life Insurance Health Cover- 36 Critical Illness Prime Care- Early Critical Illness Payor Cover (Premium Wavier) Personal Accident Investment Link / Returns / Savings

With Allianz Premier Link Plan high sum assured of Life/TPD RM500,000 from as low as RM100 monthly Time to change your MLTA to Allianz Premier Link Plan

Allianz PremierLink offers a plan that can help stretch your ringgit to protect yourself and the people who rely on you. It features a high sum assured of a minimum RM500,000 at affordable premiums to suit your financial situation.

High death and Total and Permanent Disability (TPD) coverage. Flexibility to suit your financial situation. Pay-out of both the coverage amount and the balance in the investment account in the event of death or TPD. Receive an additional 1% of your insurance premium starting on the 11th year of your policy.

» Click to show Spoiler - click again to hide... «

Allianz SE is a German multinational financial services company headquartered in Munich. Its core business and focus is insurance.

As of 2014, it is the world's largest insurance company, the largest financial services group and the largest company according to a composite measure by Forbes magazine, as well as the largest financial services company when measured by 2013 revenue.

Its Allianz Global Investors division ranks as a top-five global active investment manager, having €1,933 billion of assets under management (AuM), of which €1,408 billion are third-party assets (as of 2015-03-31), with specialized asset managers including PIMCO (bonds), RCM (equities) and Degi (real estate).

Allianz AG was founded in Berlin on 5 February 1890 by then director of the Munich Reinsurance Company Carl von Thieme (a native of Erfurt, whose father was the director of Thuringia) and Wilhelm von Finck (co-owner of the Merck Finck & Co bank). The joint company was listed in Berlin's trade register under the name Allianz Versicherungs-Aktiengesellschaft. The first Allianz products were marine and accident policies first sold only in Germany, however in 1893 Allianz opened its first international branch office in London. It distributed marine insurance coverage to German clientele looking for coverage abroad.

Allianz provided naming rights for the Allianz Arena, a football stadium in the north of Munich, Germany. The two professional Munich football clubs Bayern Munich and TSV 1860 München have played their home games at Allianz Arena since the start of the 2005–06 season. Other stadiums owned by Allianz include the Allianz Parque soccer stadium in Sao Paulo, Brazil, the Allianz Riviera soccer stadium in Nice, France, the Allianz Park rugby stadium in London, UK, and the Allianz Stadion, the new home of Rapid Vienna, a club from the Austrian Football Bundesliga.

The company has also been the sponsor of others sports, including the Women’s British Open (golf), Allianz Open de Lyon (golf), Allianz Championship (golf), Allianz Golf Open du Grand Toulouse (golf), Allianz Suisse Open Gstaad (tennis), Allianz Cup (tennis), Allianz Championship (golf), La Liga (football) and FINA Swimming World Cup (swimming) events. The National Football League of Ireland is named the Allianz National Football League for its sponsorship.

What is Powerlink (Investment Linked Plan)

» Click to show Spoiler - click again to hide... «

PowerLink gives you the flexibility you want for your coverage: Comprehensive all-in-one insurance coverage Comes with a personalized investment account for your potential investment returns It’s easy and convenient to add extra coverage at anytime, to cover your changing needs and budgets. You do not need to go through hassle of buying a new policy for these additional coverage. Just add on what you need to your existing policy.

Why Investment Linked Plan? 1. Transparency – Unlike the traditional policy such as whole life or endowment plan, an investment-linked policy reveals all your premium allocation clearly. This is what I call transparent policy – you can actually understand and see where your premium is used. Policy holder will receive a periodic statement that clearly and precisely lists all the premium allocation, relevant insurance charges, investment value and fund unit price. Insurer will get the investment-linked fund performance report annually.

2. Low insurance charges - For fresh graduates, age around 21-30, it is normal for them to seek their first insurance agent and also the first insurance policy. When you are young, insurance charges are very cheap. Investment-linked policy calculates the insurance charges based on your age. They use a mortality table and clearly provide the insurance charges table in the policy. This means you can purchase high coverage with low premium when you are still young. Sometimes, the premium is even lower than a term policy.

3. Flexibility – Once you get older, promoted, married, have kids, your protection needs eventually increase. When you retire, your kids are independent, your protection needs eventually decrease. Looking at this circumstances, investment-linked policy provides the flexibility to increase or reduce the premium, include or exclude certain coverage rider, supplementary benefits and sum assured. Put it simple, you can modify this policy whenever and however you want it to be.

4. Integrated better health card - it provide better hospitalization and surgical benefits only for investment-linked policy holder. A standalone card which is higher in premium and normally comes with co-insurance payment (means patient have to share the medical bill), annual limit and some other charges limit (Kidney Dialysis & Cancer Treatment).

5. All-in-one benefits – All sorts of coverage can be included into your investment-linked policy. This includes accidental benefit, hospitalization income benefit, living assurance, critical illnesses benefit, health card benefit, lady care benefit etc. Almost all available protection riders can be included. You will find it easier and cheaper to have one insurance plan that can give you all the possible benefits you need.

6. You control the investment strategy – Did you ever think that investment-linked policy is risky because it involves investment? Actually, you have the right to control the risk you can bear for your investment. You can choose which fund to invest, which strategy to use, which portfolio allocation to apply, and even when to do the switching from fund to fund which is normally free of charge. If you are skeptical about investment risk, just put all your premium into a fixed-income fund!

Allianz Panel Hospitals for KL/Selangor are as follow:

» Click to show Spoiler - click again to hide... «

1. Damai Service Hospital (HQ) 2. Gleneagles Intan Medical Centre 3. Hospital Pusrawi (Pusat Rawatan Islam) 4. Institut Jantung Negara 5. Al-Islam Specialist Hospital 6. Lourdes Medical Centre 7. Pantai Hospital Cheras 8. Pantai Hospital Kuala Lumpur 9. KPJ Tawakkal Specialist Hospital 10. Sentosa Medical Centre 11. Taman Desa Medical Centre 12. Tung Shin Hospital 13. Universiti Malaya Specialist Centre 14. Pantai Hospital Ampang 15. KL Eye Specialist Centre 16. Columbia Asia Hospital - Setapak 17. Damai Service Hospital (Melawati) 18. Sime Darby Medical Centre 19. KPJ Ampang Puteri Specialist Hospital 20. Arunamari Specialist Hospital 21. Assunta Hospital 22. KPJ Damansara Specialist Hospital 23. DEMC Specialist Hospital 24. Kajang Plaza Medical Centre 25. Kajang Plaza Medical Centre, Puchong 26. Kelana Jaya Medical Centre 27. KPJ Kajang Specialist Hospital 28. Pantai Hospital Klang 29. KPJ Selangor Specialist Hospital 30. Sri Kota Speceialist Medical Centre 31. Subang Jaya Medical Centre(Sime Darby Medical Centre Subang Jaya) 32. Sunway Medical Centre 33. The Tun Hussein Onn National Eye Hospital 34. Columbia Asia Hospital - Bukit Rimau 35. Columbia Asia Hospital - Cheras 36. Columbia Asia Hospital - Puchong 37. Sentosa Specialist Hospital - Klang 38. Tropicana Medical Centre 39. Pusat Pakar Mata Center for Sight 40. Sime Darby Medical Centre (Ara Damansara Medical Centre) 41. Hospital Sungai Long 42. KPJ Klang Specialist Hospital 43. Beacon International Specialist Centre - Special Panel and more

How the new GST impact Insurance?

» Click to show Spoiler - click again to hide... «

For Insurance has its own set of GST rules. Life insurance is classified as exempt rated (i.e. no GST) while the non-life or General insurance is classified as standard rate (i.e. subject to GST). However, government has indicated that the definition of life insurance will include only Life, Total & Permanent Disablement (TPD) and critical illness with death benefit. All other policies (e.g. hopitalisation & surgical, personal accident and critical illness without death benefit) will be standard rated 6%.

This mean insurance company will require to charge GST at 6% on the non-life or general insurance elements (Motor, Travel, Fire & etc) of the policy contract.

For GST payment, it really depends on whether the policy holder whether are in Investment link Plan, Transitional Plan or standard alone plan.

For Standalone plan (Premium Paying Rider), 6% GST will direct add to the cost of insurance and he/she will need to add 6% of GST to the premium.

Where as for Investment Link Plan are base on Unit Deduction Rider, mean the policy holder will no have top up the additional 6% GST to their premium, unless the premium and cash value available not enough for the additional 6% GST cost. Then top up of premium will be require and should be inform via letter by insurance company.

Any new application during the transition period or after 1st April 2015 will need to submit with new GST details and the premium with 6% GST.

[b]Kindly PM/email me your name, date of birth, gender, smoker/non-smoker, occupation & contact no. for quotation.

This post has been edited by conqu3ror: Dec 4 2017, 05:46 PM

When we are young we sacrifice our health for a bit of wealth, when we are old we spend all our wealth to gain back a bit of health. Life must be balance, nothing is more important then our health.

Normal medicover is old plan with annual limit, but Powerlink's Enhanced Medicover are new plan with no annual limit.

Sorry, we can't compare the cost for apple with orange (eg. old model car with new feature model car). I can show you both quotation if you interested.

Actually I have this medic card already (PLAN 200)

Do/How much we get from this and how long is this plan?

Can I know your medical card also from Allianz?

Allianz medical card coverage up to 91 years old with no additional cost, with Allianz 200 plan, there is no annual limit, and life limit RM1,000,000.

No annual limit mean you can claim up to RM1mil in single/multiple claim within the year. Never worry the medical cost will exceed the annual limit. You can refer the brochure for detail.

I am under Powerlink 200, i would like to know how much we can get back from this, as it is a 3 in 1 plan?

Sorry that I'm really don't understand your question. Also you provide very little info and what you mean by 3 in 1 plan? You can come to my office with your policy for further explanation.

» Click to show Spoiler - click again to hide... «

The incidence of cancer in Malaysia increased from 32,000 new cases in 2008 to 37,400 in 2012. This number is expected to rise to 56,932 by 2025 if no action is taken.

Mortality due to cancer stood at 20,100 deaths in 2008 and has increased to 21,700 deaths in 2012, according to the International Agency for Research on Cancer (IARC) Globocan of the World Health Organisation (WHO).

Building on this, the National Cancer Society of Malaysia (NCSM) is organising the World Cancer Day Conference and Expo 2014 on Feb 22 to advocate the need for prevention and early detection of the disease.

The WCD Conference and Expo 2014 will carry two main themes, namely Oncology in General Practice for medical practitioners and Cancer – Prevention, Early Diagnosis and Treatment Options for the public, as well as a few sessions for cancer survivors.

The conference aims to educate the public and expand on the knowledge of medical practitioners in the country and serve as an exchange dialogue on how cancer affects societies, and how patients can deal with cancer.

Among the highlights of the WCD Conference and Expo2014 include targeted therapies in clinical development; antibody, vaccines and cell-based therapies, the role of genetics in screening, diagnosis and treatment of cancer as well as updates on new technologies on imaging for early detection, diagnosis, treatment and rehabilitation on cancer.

New insights on nutrition and the treatment of oncology patients, symptoms of lung cancer, the effectiveness of vaccination campaigns, child cancers and surviving cancer are also part of the topics to be presented.

Worldwide, new cancer incidences over four years increased by 11% to an estimated 14.1 million cases in 2012 — equal to the population of India’s largest city Mumbai.

Based on statistics released by Globoscan 2012, cancer cases worldwide are forecast to rise by 75% and reach close to 25 million over the next two decades.

Cancer was the biggest cause of mortality worldwide — there were an estimated 8.2 million deaths from cancer in 2012.

Specifically, by 2025, almost 80% of the increase in the number of all cancer deaths will occur in less developed regions.

By 2030, developing countries will bear the brunt of the estimated 21.4 million new cancer cases per year.

To fight against the global cancer epidemic, World Cancer Day is observed yearly on Feb 4 as a reminder that everyone can take action to dispel the myths about cancer and work together to reduce the burden of the disease.

The international day marks the unlimited opportunities for societies to be part of the continued progress and advocacy in the field of oncology.

It aims to save millions of preventable deaths each year by raising awareness and education about cancer, and pressing governments and individuals across the world to take action against the disease.

This year, World Cancer Day focuses on reducing stigma and dispelling myths about cancer through the theme ‘Debunk the Myths.’

Debunking the myths include:

Myth 1: We don’t need to talk about cancer

Truth: Whilst cancer can be a difficult topic to address, particularly in some cultures and settings, dealing with the disease openly can improve outcomes at an individual, community and policy level.

Myth 2: There are no signs or symptoms of cancer

Truth: For many cancers, there are warning signs and symptoms and the benefits of early detection are indisputable.

Myth 3: There is nothing I can do about cancer

Truth: There is a lot that can be done at an individual, community and policy level and with the right strategies; a third of the most common cancers can be prevented.

Myth 4: I don’t have the right to cancer care

Truth: All people have the right to access proven and effective cancer treatments and services on equal terms, and without suffering hardship as a consequence.

NCSM is organising the conference in partnership with Infomed Malaysia and Clinical Research Malaysia, supported by the Malaysian Oncological Society.

Sep 19 2013, 11:32 AM, updated 8y ago

Sep 19 2013, 11:32 AM, updated 8y ago

Allianz_Premier_Link.pdf ( 2.75mb )

Number of downloads: 227

Allianz_Premier_Link.pdf ( 2.75mb )

Number of downloads: 227

Quote

Quote

0.0291sec

0.0291sec

0.35

0.35

7 queries

7 queries

GZIP Disabled

GZIP Disabled