Apr 10 2019, 11:12 PM

Apr 10 2019, 11:12 PM

QUOTE(HotshotS @ Apr 10 2019, 08:28 PM)

Guys, how would you choose for a loan of 550K?

RHB Full Flexi

4.5%

Daily interest calculation (approximately how much can I save each day if I park my monthly salary in the account? Whenever I need to use money then only withdraw from it in order to save daily interest)

No maintenance fee, setup fee, withdrawal fee

HLB Semi Flexi

4.28% for the first 2 years, after that BR 4.13+0.37 = 4.5% (approximately how much can I save in the first 2 years?)

Daily interest calculation

Withdrawal fee of RM 25 each time

No maintenance fee, setup fee

since HLB does offer 2 years at a lower interest rate then you'll definitely save more than RHB.RHB Full Flexi

4.5%

Daily interest calculation (approximately how much can I save each day if I park my monthly salary in the account? Whenever I need to use money then only withdraw from it in order to save daily interest)

No maintenance fee, setup fee, withdrawal fee

HLB Semi Flexi

4.28% for the first 2 years, after that BR 4.13+0.37 = 4.5% (approximately how much can I save in the first 2 years?)

Daily interest calculation

Withdrawal fee of RM 25 each time

No maintenance fee, setup fee

Quote

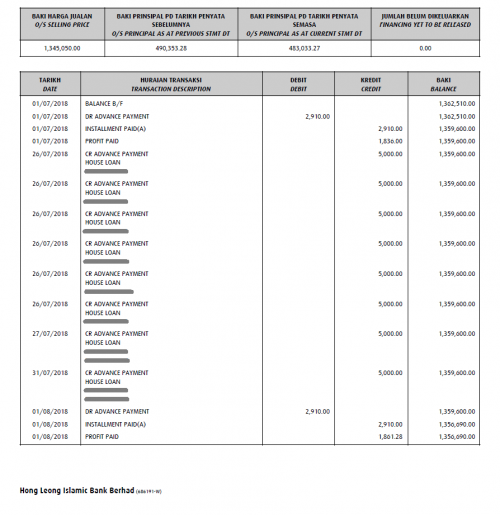

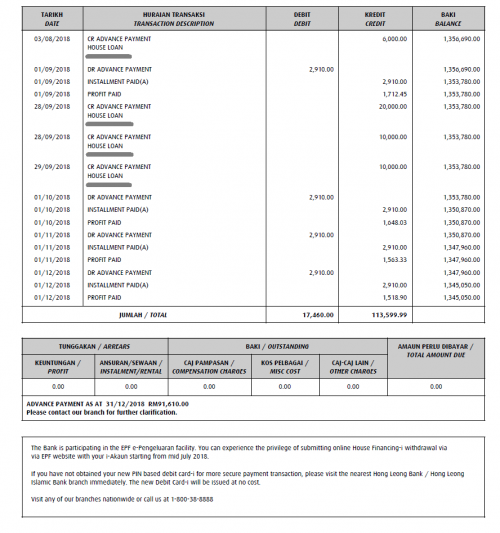

Quote I'm seeing it keep increasing through out the year. What's the best and suitable lowest rate for refinance?

I'm seeing it keep increasing through out the year. What's the best and suitable lowest rate for refinance? so is it worth consider refinance? Felt like this is a stupid question with that amount

so is it worth consider refinance? Felt like this is a stupid question with that amount

0.1146sec

0.1146sec

0.69

0.69

7 queries

7 queries

GZIP Disabled

GZIP Disabled