QUOTE(icemanfx @ May 12 2023, 03:08 PM)

Where are these better places? Klcc?

As most bought with bank loan, price rise slower than loan interest and expenses incurred is financial losses.

Where and which families?

Those have family office or with private bank are likely to invest in London, Dubai, sg, etc. Given opportunity available in other markets, this group keep very small portion of their portfolio here. In fact, many are exiting local poorperly market below peak valuation.

Klcc prices has come downed abit actually. survey around and you will notice the better areas with some hot money.

where and which family you have to dig yourself. most are not known publicly.

exited at peak now pending to make a kill again.

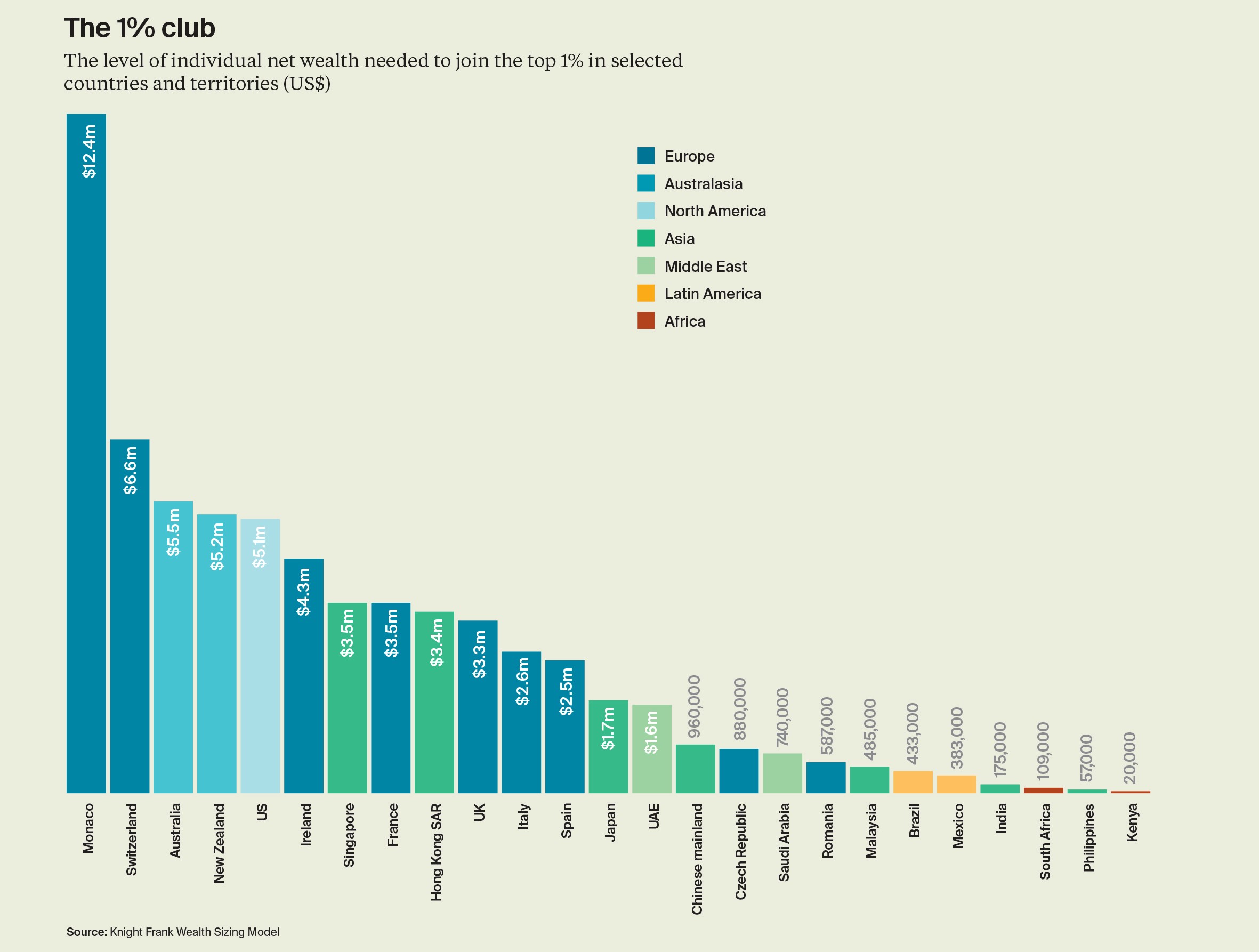

compared to london, more went to switzerland, ireland, netherlands and the likes. more on netherlands since demand there is crazy. UAE returns arent that great tbh.

however if you are okay with abit of corruption asean has a vast basket for you to grow money in property and create another bubble.

its abit off topic already.

that being said its unlikely malaysian property market will face a crash or fall anytime soon with so little rate hike, might happen if we see the % as per us. then things would be very interesting and a lot of opportunities are available for all.

May 12 2023, 12:24 PM

May 12 2023, 12:24 PM

Quote

Quote

0.0506sec

0.0506sec

0.69

0.69

7 queries

7 queries

GZIP Disabled

GZIP Disabled