Depend what you want to look for. Original FIRE is getting there as soon as you can. That is what I follow.

If you want FAT FIRE and as fast as possible no choice.

If you want to take your time, it is not FIRE as likely normal retirement. FIRE means retire in your 30s or late 40s max.

If retire at 50 sorry la. That is not my definition of FIRE. I am already LEAN FIRE. I am aiming for FAT FIRE.

The point are 5 things

1. Get to the finish line as soon as possible. Do not enjoy the journey. Enjoy the very long finish line with the time you bought. Imagine retiring at 30+ FAT FIRE. You got a very long road ahead while your peers all slough and work like a donkey and you just be a unemployed person. Time kena owned by the company and not your own time. I don't want my time to be owned by anyone. If you live the life without it being own by anyone you will love it. I lived that life before.

2. Get FAT FIRE. Able to go anywhere, eat anything and move to any country. Total freedom. Don't like country A, pack up your bags and move. Not restricted by your money or destination. Be a digital nomad.

3. Support my biohacking to live a long healthy life and age gracefully. No meds at 60-70 years old.

4. Imagine no need to work and money continue to come in.

5. Imagine getting 10% raise a year automatically without any KPIs to meet. Which company can increase your pay by 10%p.a into perpetuity.

Many have done it, can be done. Just be patient. Many cannot tahan the hard life so try to find excuse by having so many deviations.

Part of it.

Yup can't do that. She will freak out and leave me if I suddenly do that. She told me she don't want guys who spend like that 😂

My mum will also me if I were to spend like that.

Depends on what you want lo. I would rather retire at 45 Vs 47 or 50 just because I spend more. But that's me. If can I want 40. But have to be super conservativem

Very worth it if you have live the FIRE life before. I have done it, I can do it again on larger scale.

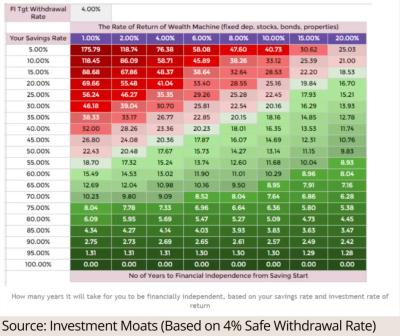

Something to ponder on…the Table below. (Source from YT video: [url=https://www.youtube.com/watch?v=y7sXA8Cn9cU] don't wanna embed the video in here because somehow my past videos embedded in here got removed

PS: Don't ask me about the formulas and technicalities on how the table is derived

But yes, I do support bro Ramjade. Still, I do agree everyone is entitled to live their own ways as long one is happy.

Aug 28 2025, 08:27 AM

Aug 28 2025, 08:27 AM

.

. Quote

Quote

0.0619sec

0.0619sec

0.90

0.90

7 queries

7 queries

GZIP Disabled

GZIP Disabled