Dec 29 2023, 09:16 AM

Dec 29 2023, 09:16 AM

QUOTE(devilmaycry9 @ Dec 12 2023, 02:52 PM)

I have a question.. if i want to upgrade my existing insurance plan for example plan 250 to 350 room&board will my policy subject to waiting period & 2 yrs contestability period again?

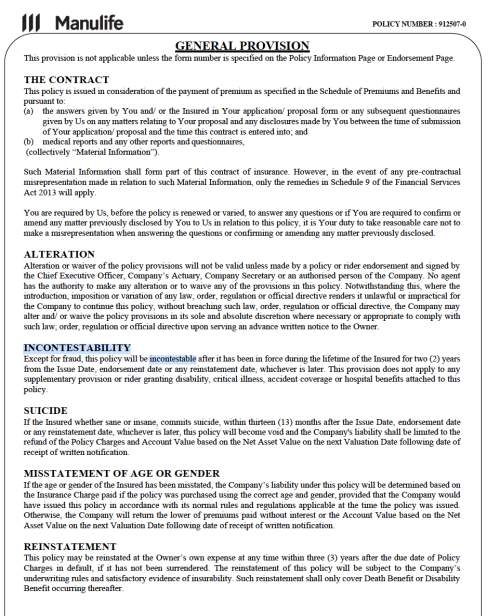

It depends on internal offer to upgrade or self upgrade.If internal offer the contestable period waived off.

QUOTE(Gaza @ Dec 28 2023, 03:31 PM)

If my spouse stops working and i take over the payment of her life or medical insurace, am i able to claim the income tax relief if policy owner and life insured is under my spouse's name?

Request to change the policy owner under your name.QUOTE(Ramjade @ Dec 28 2023, 11:27 AM)

Yes. This is the only worth it place to buy insurance online

https://fi.life/

Now whether they have cash value is another story. You need to explore the product yourself.

If you don't mind lower coverage then Deartime (designed for B40), and FWD.

Rest of insurance online are just pure rubbish. (Low coverage).

Group insurance? is this guaranteed renewal up to age 99?https://fi.life/

Now whether they have cash value is another story. You need to explore the product yourself.

If you don't mind lower coverage then Deartime (designed for B40), and FWD.

Rest of insurance online are just pure rubbish. (Low coverage).

if anything happened along the way, will kena charge loading or subject to company renewal? TQ

QUOTE(fishermanG @ Dec 25 2023, 12:25 PM)

What’s the recommended medical insurance for Malaysian working in Brunei?

Currently has Zurich ILP which covers 200k coverage for death/TPD. And, 50k for medical insurance. But just realise that it doesn’t cover overseas if I am residing for > 90 days which I’m currently am due to my work.

Am currently thinking of switching to AIA which cover Singapore and Brunei.

Is it recommended to get one with a local insurance company?

Good day! Manulife covered brunei and sg as well. not limited to 90days. TQCurrently has Zurich ILP which covers 200k coverage for death/TPD. And, 50k for medical insurance. But just realise that it doesn’t cover overseas if I am residing for > 90 days which I’m currently am due to my work.

Am currently thinking of switching to AIA which cover Singapore and Brunei.

Is it recommended to get one with a local insurance company?

Quote

Quote

0.0228sec

0.0228sec

0.27

0.27

7 queries

7 queries

GZIP Disabled

GZIP Disabled