Apr 11 2024, 07:01 PM

Apr 11 2024, 07:01 PM

QUOTE(adele123 @ Apr 8 2024, 04:24 PM)

My mum has aia plan too but up to age 100. The premium i paid recently, at age 70 is 8.3k.

You probably dont have much alternative

1) you continue paying

2) you find alternative from aia or other companies

3) you fund for it yourself

2) for older parents, probably not much options. On paper, they can enter into buying a new one but in reality most likely they usually have some health conditions by then.

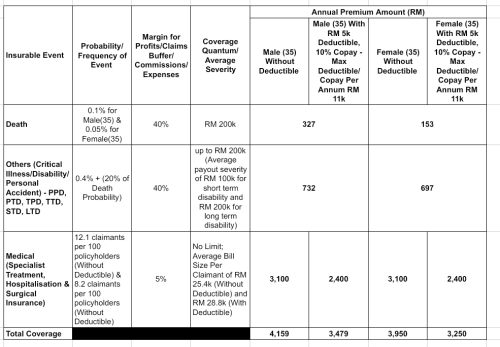

Alternatively, and something i have always advocate is you buy something with a high deductible. Say 10,000 for example. When your parents sick, you pay 10k (that's what deductible mean). Any expenses after 10k, is borne by insurance company. If you can afford 10k on your own then the premium will be cheaper.

This alternative will be better than option 3, which is funding it yourself. It's less damaging but yes you gotta fork out some money if something happens.

Moving to Co-pay and/or high deductible are something i am considering recently. You probably dont have much alternative

1) you continue paying

2) you find alternative from aia or other companies

3) you fund for it yourself

2) for older parents, probably not much options. On paper, they can enter into buying a new one but in reality most likely they usually have some health conditions by then.

Alternatively, and something i have always advocate is you buy something with a high deductible. Say 10,000 for example. When your parents sick, you pay 10k (that's what deductible mean). Any expenses after 10k, is borne by insurance company. If you can afford 10k on your own then the premium will be cheaper.

This alternative will be better than option 3, which is funding it yourself. It's less damaging but yes you gotta fork out some money if something happens.

My ILP premium went up from 3XX to 5XX over 2-3 years while still within the age band. Crazy stuff.

Quote

Quote

0.0300sec

0.0300sec

0.45

0.45

7 queries

7 queries

GZIP Disabled

GZIP Disabled