Oct 31 2021, 10:26 AM

Oct 31 2021, 10:26 AM

I'm thinking of increasing my Annual Limit on the Medical Card & adding Riders.

1. If I wish to increase my Death/TPD or CI coverage, would it cost less to upgrade my current Rider or to buy a standalone Term Life Online Policy (until 80yrs coverage) ?

2. Can I upgrade my current plan to the Smart Medic Million + Extender & upgrade my Riders, Without Underwriting again ?

3. Would it be better to collect my surrender value & change to Allianz Medisafe Infinite+, as it provides better additional benefits (20% NCB Discount & Traditional Medicine/2nd Opinion) OR should I just continue with Great Eastern because I've already paid the Agent's fee ?

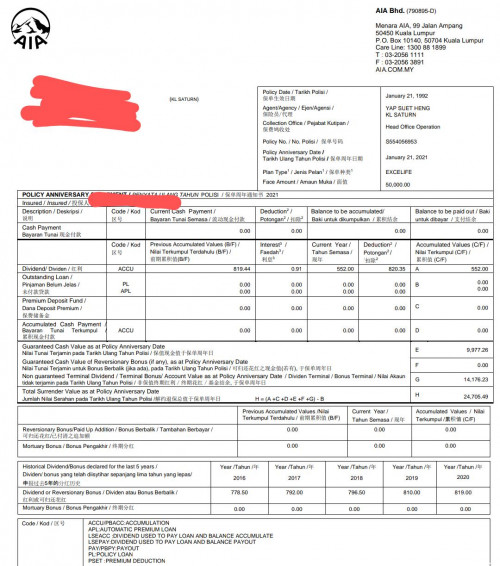

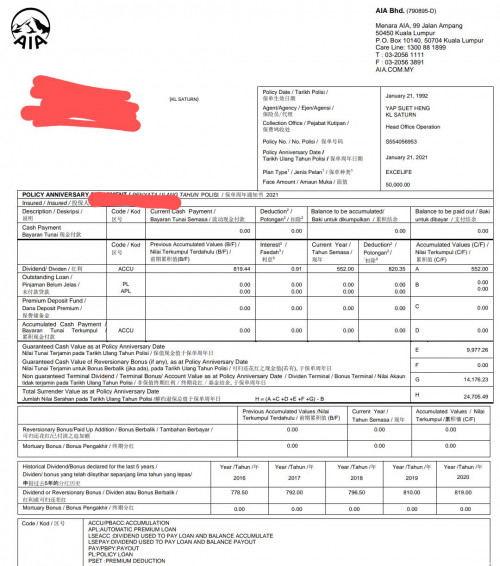

4. A relative of mine has an AIA Excelife Whole Life Policy.

Is it possible to Withdraw the Cash Value & still maintain coverage by paying the premium annually ?

All research so far says No, however, an Insurance Agent, said Yes. I'm wondering if he's confused Whole Life with ILP ?

Apologies for so many questions.

Thanks in advance, been researching Insurance for the past 3 days. I'm confident I can explain insurance policies better than 50% of Agents

https://pictr.com/images/2021/10/31/BVwdQ6.md.png

https://pictr.com/images/2021/10/31/BVwuDq.md.png

Attached thumbnail(s)

Quote

Quote ), and the NCB would probably cover the Agent's Commission in the long run.

), and the NCB would probably cover the Agent's Commission in the long run.

0.0279sec

0.0279sec

1.14

1.14

7 queries

7 queries

GZIP Disabled

GZIP Disabled