Jul 27 2021, 08:37 PM

Jul 27 2021, 08:37 PM

QUOTE(brando_w @ Jul 27 2021, 08:13 PM)

It has come to my knowledge recently that only AIA covers for hospitalization (medical card) due to ‘Pandemic’, thus any admission due to Covid-19 can be covered by their medical card.

Being a Prudential customer for close to 20 years, am a little disappointed that PMM or PVM does not offer the same benefit; especially when we need it the most.

I understand that one can opt to be treated in private hospitals at present if one is to be unfortunately infected with Covid-19. The cost cost of treatment can run into hundreds of thousands if you’re in the critical stage.

Am looking into taking up AIA’s medical card and eventually disposing off my PRU med cards for the entire family (Will maintain Life, TPD & CI with Pru).

Need some unbiased opinion on this matter.

Being a Prudential customer for close to 20 years, am a little disappointed that PMM or PVM does not offer the same benefit; especially when we need it the most.

I understand that one can opt to be treated in private hospitals at present if one is to be unfortunately infected with Covid-19. The cost cost of treatment can run into hundreds of thousands if you’re in the critical stage.

Am looking into taking up AIA’s medical card and eventually disposing off my PRU med cards for the entire family (Will maintain Life, TPD & CI with Pru).

Need some unbiased opinion on this matter.

what does it actually covers?...the cost of the expenses or just provide some sort of "consolations expenses/benefits"?

what does it actually covers?...the cost of the expenses or just provide some sort of "consolations expenses/benefits"?and also does this "benefits" has any sort of "coverage effect expiry date" or until total targetted pool of money being used up?

Quote

Quote

cannot simply say inside here, later other insurance agent will come hentam

cannot simply say inside here, later other insurance agent will come hentam

too limited details, can't really advise you much

too limited details, can't really advise you much

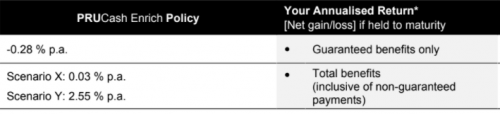

why not paint the full picture on Pru's saving plan and not just the good part?

why not paint the full picture on Pru's saving plan and not just the good part?

0.0207sec

0.0207sec

0.25

0.25

6 queries

6 queries

GZIP Disabled

GZIP Disabled