fyi, baby medical insurance is very expensive.

if you ignore all the noises, medical insurance is the same for kids and adult. after all, what you need is someone pay the hospital bill if you are sick. now the problem is babies get sick alot when they are younger. so this resulted in frequent hospitalisation and thus resulting in more expensive medical insurance.

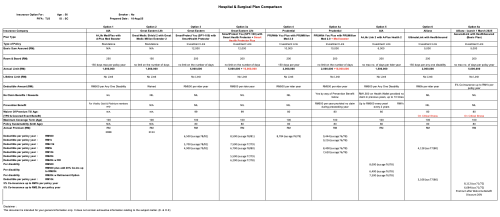

looks like you have tried searching online, so i summarise to a few potential option (realistically). we are not here to debate why babies masuk hospital often and whether those hospitalisation is necessary because that's beyond me and that wont be helpful to your question anyway.

1) you buy medical insurance from agent. this is likely to cost AT LEAST 150 a month if you want low deductible amount like 300 500. If you are ok to go higher deductible, i may be cheaper. how much higher deductible. 5k 10k... etc... but this is probably not something suitable for you.

2) you probably need to buy as family plan, as you have pointed out above (not sure what's the cost, you do your own maths)

3) as cruel as it sounds, private medical insurance may not be the option for you. you can consider this maybe after your child grows abit older, the cost of medical insurance starts to dive around age 5 to 6 also.

You can buy standalone medical which is a cheaper option, most insurers have it and it covers to 80-100 years old.

Take note of your sustainability if you buying from agents, and they always come with investment link which may not be best the difference put it in your epf and you get best returns and standalone medical. Best from both

Aug 14 2025, 05:59 AM

Aug 14 2025, 05:59 AM

Quote

Quote

0.0767sec

0.0767sec

0.40

0.40

6 queries

6 queries

GZIP Disabled

GZIP Disabled