Jun 14 2024, 01:15 PM

Jun 14 2024, 01:15 PM

QUOTE(hafizmamak85 @ Jun 14 2024, 11:06 AM)

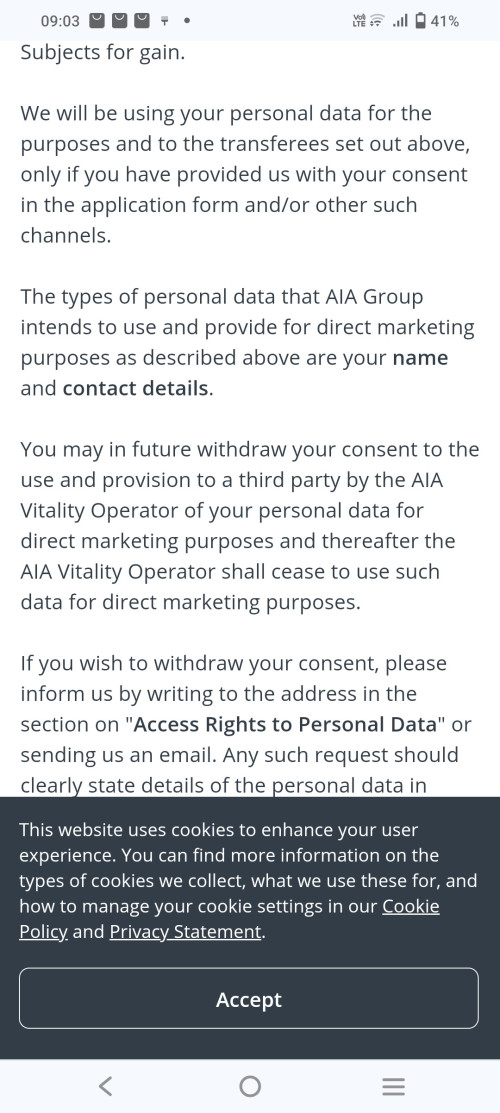

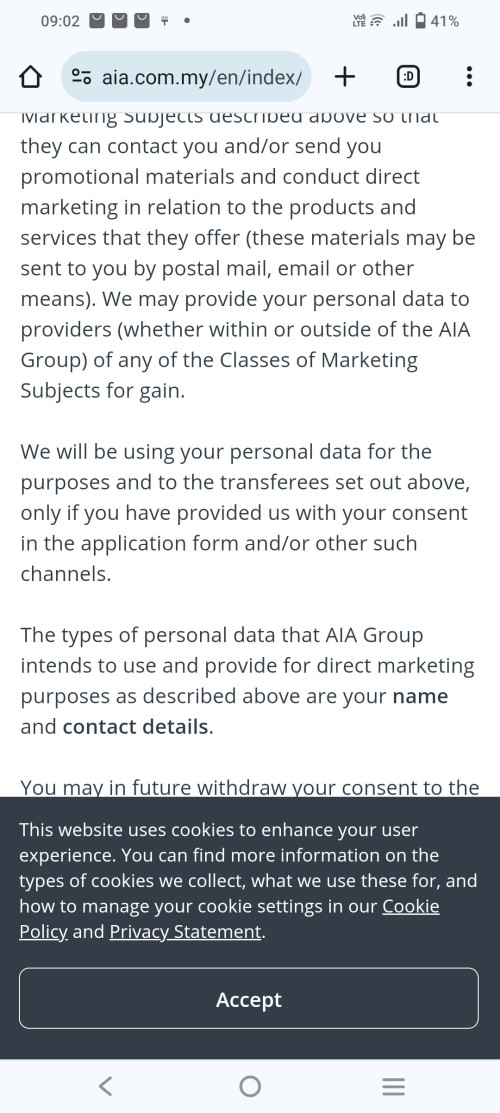

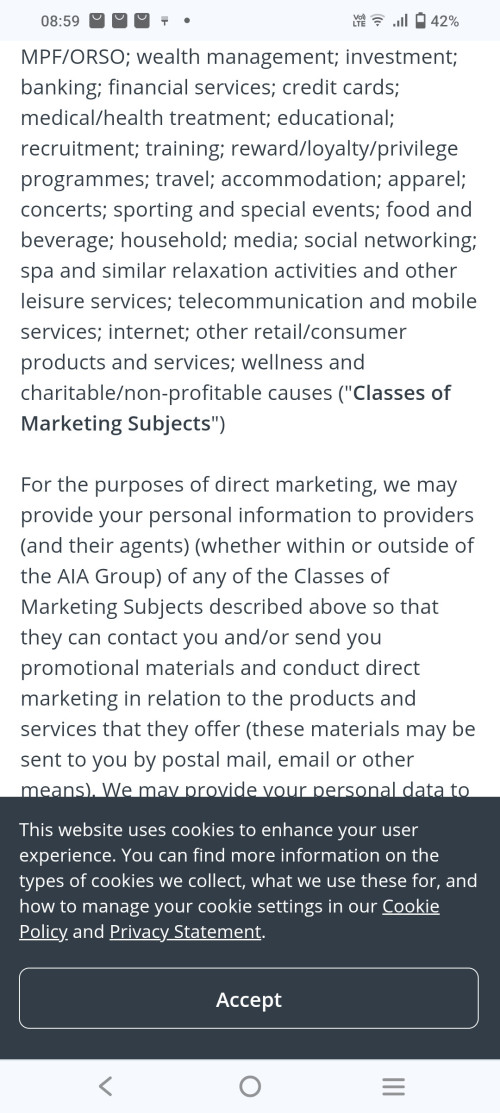

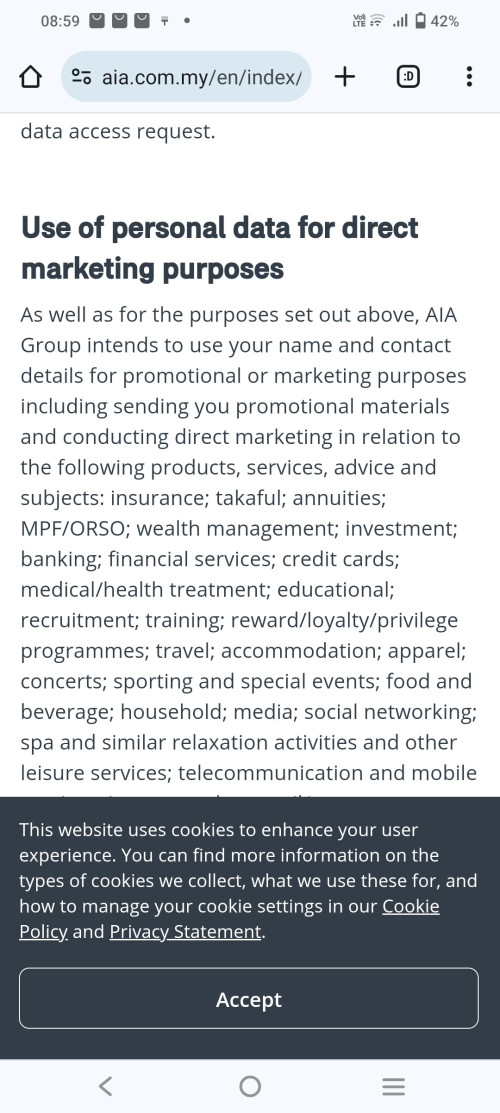

Where did you get this information that policyholders do have the right to opt out of any sharing of their personal information with partnering vendors? Short of not signing up for AIA vitality or cancelling your AIA vitality membership, there are no options, from what I can see in their website, that allow you to opt out of sharing personal information with any of the vitality partners. Even if you cancel your AIA vitality membership, the terms are silent as to the disposal of all personal information by either AIA vitality and/or their affiliates/partners. Policyholders only have the option to opt out of "direct marketing" initiatives. They will still be prone to indirect marketing and partners/affiliates will remain free to retain and manipulate personal information data for data analytics purposes. Not only that, AIA Group reserves the rights to sell your data to other parties as part of their M&A activities.

Is clarifying and enforcing rights and interests, fairness in contract now considered "victim mentality"? Superficial artifice is not the stuff that makes for financial stability, it only excites the wanton individual. Nor does illegal /unlawful activities such as sharing data without consent and the non provision of "opt-out" function in any personal information data arrangement/sharing schemes for non insurance related service provisions - this is against provisions within the Policy Document on Management of Customer Information and Permitted Disclosures. Due to the muddling of insurance value propositions with marketing value propositions , key risks arise:

- That non-vitality members are subsidizing vitality members for the provision of vitality's insurance policy benefits

- That vitality members may lose out on their vitality insurance policy benefits if they request that their personal data not be shared with any affiliates/partners and/or have their request completely ignored

- That vitality members are also at risk of having their vitality insurance policy benefits revoked, augmented in a manner that leaves them worse off at the whim of AIA vitality for whatever reason AIA vitality deems fit.

I'm glad you asked. Is clarifying and enforcing rights and interests, fairness in contract now considered "victim mentality"? Superficial artifice is not the stuff that makes for financial stability, it only excites the wanton individual. Nor does illegal /unlawful activities such as sharing data without consent and the non provision of "opt-out" function in any personal information data arrangement/sharing schemes for non insurance related service provisions - this is against provisions within the Policy Document on Management of Customer Information and Permitted Disclosures. Due to the muddling of insurance value propositions with marketing value propositions , key risks arise:

- That non-vitality members are subsidizing vitality members for the provision of vitality's insurance policy benefits

- That vitality members may lose out on their vitality insurance policy benefits if they request that their personal data not be shared with any affiliates/partners and/or have their request completely ignored

- That vitality members are also at risk of having their vitality insurance policy benefits revoked, augmented in a manner that leaves them worse off at the whim of AIA vitality for whatever reason AIA vitality deems fit.

At policy application process, the customer has the right to decide if they want their details to either be shared with partnering vendors for promotions and marketing engagements, or not. I think this is very standard option around the world. Like I said, you cannot see yourself past being a victim.

You're not clarifying bro, you're alleging things that are not true in the way YOU see everything around you.

Then you DEMAND that others PROVE TO YOU that it isn't so.

You're a learned person, maybe a bit of researching skills or just simply ASKING is not beyond you kan?

Maybe you should show some evidence to non-vitality members SUBSIDIZING vitality members, how about that?

The Vitality program is integrated into products to the benefit of the insured, and somehow you managed to find a way to see how it is a terrible program.

Yes, the companies AIA and Vitality acknowledge that the program is not immune to abuse. And even the Vitality points are indeed audited for authenticity. You used to work as an analyst, in BNM, I believe an audit is not a foreign idea to you kan?

Maybe you should provide some evidence to back your allegations that non-vitality customers personal details are being shared to Vitality partner vendors, how about that? I think it's only natural kan?

If I don't participate into the Vitality program, would it make sense for me to still enjoy the benefits of the Vitality program?

This post has been edited by JIUHWEI: Jun 14 2024, 01:16 PM

Quote

Quote

0.5056sec

0.5056sec

1.06

1.06

7 queries

7 queries

GZIP Disabled

GZIP Disabled