Outline ·

[ Standard ] ·

Linear+

Insurance Talk V7!, Your one stop Insurance Discussion

|

mycolumn

|

Mar 18 2021, 01:30 PM Mar 18 2021, 01:30 PM

|

|

QUOTE(MUM @ Mar 18 2021, 01:16 PM) googled and found this Am I required to present my e-Medical card at a hospital upon admission? You are required to present your NRIC (or equivalent) and/or e-Medical Card to the hospital during admission for verification purposes. Please refer to our Hospital Alliance Services here. https://www.prudential.com.my/en/claims-and...pruaccess-plus/Owh, IC is enough. That's good and convenience. Thanks for the info! QUOTE(lifebalance @ Mar 18 2021, 01:18 PM) You can mention your NRIC number or download the Pulse app Thanks! I have just downloaded the Pulse app  |

|

|

|

|

|

ping325

|

Mar 18 2021, 02:06 PM

|

|

|

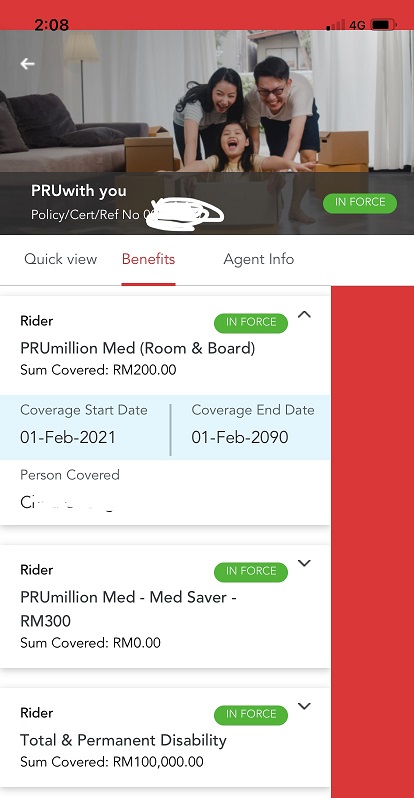

QUOTE(mycolumn @ Mar 18 2021, 01:09 PM) Hi, I wanna ask, for e-medical card, how do i go about this? Let's say need hospitalization; I just tell the hospital that I have insurance? Or do I need to print my e-medical card and keep it with me always? This is for Prudential. nowadays everything stored in database , just flash your NRIC will do , do note that cashless for prudential got waiting period. if you already purchase for very long time then it works cashless, at least one year onwards to be safe. if you just purchase and want to use within few months , hospital might ask for pay first , claim later from prudential basis. Btw , you can download pulse and link your policy for your convenience. Sample of one of my client as below :  This post has been edited by ping325: Mar 18 2021, 02:13 PM This post has been edited by ping325: Mar 18 2021, 02:13 PM |

|

|

|

|

|

ckdenion

|

Mar 18 2021, 05:25 PM

|

|

|

QUOTE(kumarz84 @ Mar 15 2021, 04:54 PM) can sumone suggest me insurance for 1 year old and how much eill be the cheapest premium and what will be the coverage like? QUOTE(kumarz84 @ Mar 15 2021, 05:26 PM) thanks for ur reply if u say 188 monthly what insurance like? my budget around 200 hi kumarz84, usually insurance for baby, my guide will be focusing on both medical and critical illness payout benefit - Medical Card that comes with RM1million annual limit is a very good start and it is definitely within your budget of 200/month. - Critical Illness payout amount will be determined by you yourself. My guide on this is to have amount equivalent to your 1 year salary. Reason being is to replace your income should in any critical illness event and your child need a full time caretaker. Caretaker (the father/mother) can take unpaid leave to take care of the child during that period. |

|

|

|

|

|

mycolumn

|

Mar 19 2021, 06:56 AM

|

|

|

QUOTE(ping325 @ Mar 18 2021, 02:06 PM) nowadays everything stored in database , just flash your NRIC will do , do note that cashless for prudential got waiting period. if you already purchase for very long time then it works cashless, at least one year onwards to be safe. if you just purchase and want to use within few months , hospital might ask for pay first , claim later from prudential basis. Btw , you can download pulse and link your policy for your convenience. Sample of one of my client as below : If i recall correctly, my agent told me that for prudential, yups, within the first 4 months i have to pay first and then claim later. After the 4 months, then during admission, have to pay rm500 deposit first and when discharged, rm300 out of the rm500 will be paid to prudential. |

|

|

|

|

|

lifebalance

|

Mar 19 2021, 08:55 AM

|

|

|

QUOTE(mycolumn @ Mar 19 2021, 06:56 AM) If i recall correctly, my agent told me that for prudential, yups, within the first 4 months i have to pay first and then claim later. After the 4 months, then during admission, have to pay rm500 deposit first and when discharged, rm300 out of the rm500 will be paid to prudential. The first 4 mths is the waiting period. Thereafter you're covered fully for your medical benefits. The RM300 is the deductible within your plan. |

|

|

|

|

|

ragk

|

Mar 22 2021, 05:32 PM

|

|

|

I have a protection plan from AIA (A-Life Signature Beyond), it cost me 1.3k per month, already paid for around 2.5 years.

Recently i review my financial status and i realize the cost of this plan was build up from A-Life Signature Beyond-RM555 + A-Plus CriticalReset-RM759 per month.

The initial motive i bought this plan was for the 500k protection (A-Life Signature Beyond) for my family, i do aware i have the reset plan, but i didn't aware that it cost more than my main protection.

So it came to my mind to cancel this plan (i dun mind the sunken cost) and go for pure protection, because 9k per year just for reset is too much imo.

But on 2nd though, i already paid for the 2 years 50% premium, if i continue to pay what im paying now, but withdraw 9k from my account every year, will the the reset plan still sustain? Is this approach possible instead of cancelling it?

This post has been edited by ragk: Mar 22 2021, 05:33 PM

|

|

|

|

|

|

lifebalance

|

Mar 22 2021, 05:37 PM

|

|

|

QUOTE(ragk @ Mar 22 2021, 05:32 PM) I have a protection plan from AIA (A-Life Signature Beyond), it cost me 1.3k per month, already paid for around 2.5 years. Recently i review my financial status and i realize the cost of this plan was build up from A-Life Signature Beyond-RM555 + A-Plus CriticalReset-RM759 per month. The initial motive i bought this plan was for the 500k protection (A-Life Signature Beyond) for my family, i do aware i have the reset plan, but i didn't aware that it cost more than my main protection. So it came to my mind to cancel this plan (i dun mind the sunken cost) and go for pure protection, because 9k per year just for reset is too much imo. But on 2nd though, i already paid for the 2 years 50% premium, if i continue to pay what im paying now, but withdraw 9k from my account every year, will the the reset plan still sustain? Is this approach possible instead of cancelling it? Oh I'm quite surprised that you've only noticed this 2.5 years later (but it's never too late). Depending on the cash value within the policy, it may not sustain long as your policy is still very young, the rider will still be there until your policy account value is RM0. |

|

|

|

|

|

KLlang

|

Mar 22 2021, 05:46 PM

|

New Member

|

QUOTE(ragk @ Mar 22 2021, 05:32 PM) I have a protection plan from AIA (A-Life Signature Beyond), it cost me 1.3k per month, already paid for around 2.5 years. Recently i review my financial status and i realize the cost of this plan was build up from A-Life Signature Beyond-RM555 + A-Plus CriticalReset-RM759 per month. The initial motive i bought this plan was for the 500k protection (A-Life Signature Beyond) for my family, i do aware i have the reset plan, but i didn't aware that it cost more than my main protection. So it came to my mind to cancel this plan (i dun mind the sunken cost) and go for pure protection, because 9k per year just for reset is too much imo. But on 2nd though, i already paid for the 2 years 50% premium, if i continue to pay what im paying now, but withdraw 9k from my account every year, will the the reset plan still sustain? Is this approach possible instead of cancelling it? ragk, A-Plus CriticalReset is an optional rider that can be attached to A-Life Signature Beyond regular premium Investment-Linked Insurance plan. Is a unit deducting rider that pays the coverage amount in the event you are being diagnosed with any one of the 39 critical illnesses. It is up to 200% payable sum assured for Stroke, Cancer or Heart Attack, thereafter the coverage shall terminate. It is a pure protection on top of death coverage. |

|

|

|

|

|

ragk

|

Mar 22 2021, 06:13 PM

|

|

|

QUOTE(lifebalance @ Mar 22 2021, 05:37 PM) Oh I'm quite surprised that you've only noticed this 2.5 years later (but it's never too late). Depending on the cash value within the policy, it may not sustain long as your policy is still very young, the rider will still be there until your policy account value is RM0. ok understood, thanks! QUOTE(KLlang @ Mar 22 2021, 05:46 PM) ragk, A-Plus CriticalReset is an optional rider that can be attached to A-Life Signature Beyond regular premium Investment-Linked Insurance plan. Is a unit deducting rider that pays the coverage amount in the event you are being diagnosed with any one of the 39 critical illnesses. It is up to 200% payable sum assured for Stroke, Cancer or Heart Attack, thereafter the coverage shall terminate. It is a pure protection on top of death coverage. Yes it's an additional protection, if i understand correctly, the reset grant me protection twice (which mean i still entitled for protection if 2nd illness were discovered). But the reset payment alone is more than my main plan. This post has been edited by ragk: Mar 22 2021, 06:13 PM |

|

|

|

|

|

Cyclopes

|

Mar 22 2021, 06:38 PM

|

|

|

QUOTE(ragk @ Mar 22 2021, 05:32 PM) I have a protection plan from AIA (A-Life Signature Beyond), it cost me 1.3k per month, already paid for around 2.5 years. Recently i review my financial status and i realize the cost of this plan was build up from A-Life Signature Beyond-RM555 + A-Plus CriticalReset-RM759 per month. The initial motive i bought this plan was for the 500k protection (A-Life Signature Beyond) for my family, i do aware i have the reset plan, but i didn't aware that it cost more than my main protection. So it came to my mind to cancel this plan (i dun mind the sunken cost) and go for pure protection, because 9k per year just for reset is too much imo. But on 2nd though, i already paid for the 2 years 50% premium, if i continue to pay what im paying now, but withdraw 9k from my account every year, will the the reset plan still sustain? Is this approach possible instead of cancelling it? The Cost of Insurance for the rider is very transparent in the Sales Illustration, before you sign up. You can terminate the rider if it doesn't serve your needs or too expensive. Do contact your Life Planner how best to proceed with the policy/rider. This post has been edited by Cyclopes: Mar 22 2021, 07:45 PM |

|

|

|

|

|

KLlang

|

Mar 22 2021, 10:12 PM

|

New Member

|

QUOTE(ragk @ Mar 22 2021, 06:13 PM) ok understood, thanks! Yes it's an additional protection, if i understand correctly, the reset grant me protection twice (which mean i still entitled for protection if 2nd illness were discovered). But the reset payment alone is more than my main plan. ragk, Yes. If it is not what you want, you can contact the servicing agent to remove the reset rider itself. This change normally will not affect the basic death coverage. This post has been edited by KLlang: Mar 22 2021, 10:13 PM |

|

|

|

|

|

ragk

|

Mar 22 2021, 10:56 PM

|

|

|

QUOTE(Cyclopes @ Mar 22 2021, 06:38 PM) The Cost of Insurance for the rider is very transparent in the Sales Illustration, before you sign up. You can terminate the rider if it doesn't serve your needs or too expensive. Do contact your Life Planner how best to proceed with the policy/rider. QUOTE(KLlang @ Mar 22 2021, 10:12 PM) ragk, Yes. If it is not what you want, you can contact the servicing agent to remove the reset rider itself. This change normally will not affect the basic death coverage. remove/terminate the rider, mean the plan can be maintain but just remove the critical reset? no need to cancel and rebuy new plan starting from year 1 again? |

|

|

|

|

|

KLlang

|

Mar 23 2021, 06:42 AM

|

New Member

|

QUOTE(ragk @ Mar 22 2021, 10:56 PM) remove/terminate the rider, mean the plan can be maintain but just remove the critical reset? no need to cancel and rebuy new plan starting from year 1 again? YES |

|

|

|

|

|

Cyclopes

|

Mar 23 2021, 06:44 AM

|

|

|

QUOTE(ragk @ Mar 22 2021, 10:56 PM) remove/terminate the rider, mean the plan can be maintain but just remove the critical reset? no need to cancel and rebuy new plan starting from year 1 again? Yup, you can maintain the existing policy. |

|

|

|

|

|

ragk

|

Mar 23 2021, 10:13 AM

|

|

|

QUOTE(KLlang @ Mar 23 2021, 06:42 AM) QUOTE(Cyclopes @ Mar 23 2021, 06:44 AM) Yup, you can maintain the existing policy. Thanks!! |

|

|

|

|

|

lifebalance

|

Mar 23 2021, 10:17 AM

|

|

|

QUOTE(ragk @ Mar 22 2021, 06:13 PM) ok understood, thanks! Yes it's an additional protection, if i understand correctly, the reset grant me protection twice (which mean i still entitled for protection if 2nd illness were discovered). But the reset payment alone is more than my main plan. if you think that you don't need the critical illness coverage at this moment, you have an option to 1. Reduce the CI coverage to a lower amount 2. Remove the CI Coverage totally |

|

|

|

|

|

ragk

|

Mar 23 2021, 10:44 AM

|

|

|

QUOTE(lifebalance @ Mar 23 2021, 10:17 AM) if you think that you don't need the critical illness coverage at this moment, you have an option to 1. Reduce the CI coverage to a lower amount 2. Remove the CI Coverage totally A-Plus Critical Reset is not really mean for CI coverage right? As i understand the main purpose is to reset the coverage if u have been diagnose of CI the 2nd time. A-Life Signature Beyond it self already has CI coverage no? But paying reset with price higher than my main plan is weird, i might as well buy 2 plan and its still cheaper. This post has been edited by ragk: Mar 23 2021, 10:46 AM |

|

|

|

|

|

ping325

|

Mar 23 2021, 10:46 AM

|

|

|

QUOTE(ragk @ Mar 23 2021, 10:13 AM) Hi ragk Another forummer, his aia agent told him not possible to reduce or remove , which is totally not true. If your agent behave this way , you can just bypass him & directly email or contact HQ instead. Some bad agent reluctant or find excuse not to do this as it affect his commission. This post has been edited by ping325: Mar 23 2021, 10:48 AM |

|

|

|

|

|

lifebalance

|

Mar 23 2021, 10:50 AM

|

|

|

QUOTE(ragk @ Mar 23 2021, 10:44 AM) A-Plus Critical Reset is not really mean for CI coverage right? As i understand the main purpose is to reset the coverage if u have been diagnose of CI the 2nd time. A-Life Signature Beyond it self already has CI coverage no? But paying reset with price higher than my main plan is weird, i might as well buy 2 plan and its still cheaper. The "Critical Reset" is the CI coverage which also includes a reset feature that is payable for cancer, heart attack and stroke. it's an all-in-one rider. You don't have an option to nit-pick certain features to maintain tho, it's either you take or drop it entirely. |

|

|

|

|

|

ckdenion

|

Mar 23 2021, 02:54 PM

|

|

|

QUOTE(ragk @ Mar 23 2021, 10:44 AM) A-Plus Critical Reset is not really mean for CI coverage right? As i understand the main purpose is to reset the coverage if u have been diagnose of CI the 2nd time. A-Life Signature Beyond it self already has CI coverage no? But paying reset with price higher than my main plan is weird, i might as well buy 2 plan and its still cheaper. hi ragk, you can look on A-Plus Critical Reset details here.. You can opt to remove this rider. perhaps before you do so, review again your risk management needs. perhaps this CI payout will really benefit you. best to discuss with your agent and see will this benefit help. other than that, cant give much advise cuz I don't know much about your needs and situation. |

|

|

|

|

Quote

Quote

0.0264sec

0.0264sec

0.19

0.19

6 queries

6 queries

GZIP Disabled

GZIP Disabled