QUOTE(JIUHWEI @ Oct 5 2023, 05:10 PM)

There's 3 parts to an ILP policy - 1) regular premiums; 2) regular top-up; 3) ad-hoc top-up.

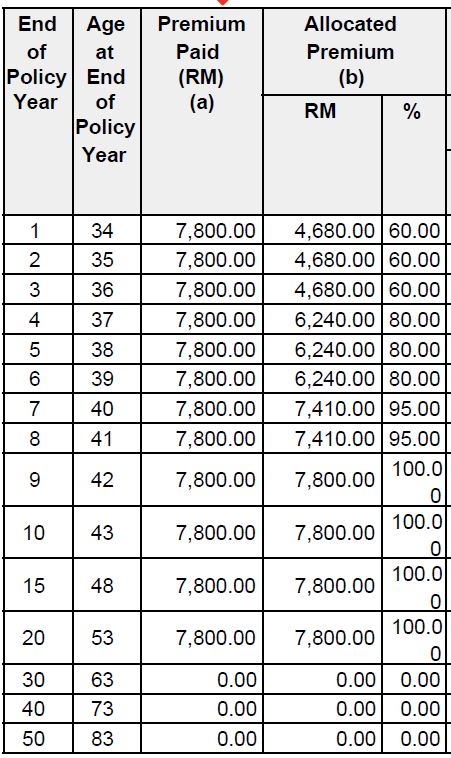

So everybody knows about the regular premiums - 161% of the annual premiums, spread out over 6 years, subject to adherence to BSC and persistency over D0, D1 & D2.

Now come the regular top-up - 2.xx% perpetually.

Now come the ad-hoc top-up - 2.xx% on each and every top-up.

Any new amounts that come in under any of the 3 categories above will be treated the same accordingly.

So if you love your agents a lot, maybe consider some amounts in regular top-up and ad-hoc top-up regularly?

Then we come to traditional policies - 171% of the annual premiums, spread out over 6 years, also subject to adherence to BSC and persistency over D0, D1 & D2.

If I can be even more transparent about it, let me know how.

Thanks for the extra color. To me, it is still a bit confusing as it could be due to the terminology used.

What we can understand is that ILP is a more lucrative to both the insurer and the agents, which is why ILP is sold more actively. Nothing wrong with this, but to keep on claiming medical card is inferior on its own is not right.

The product manager (someone I knew due to my work, and no, I am not from insurance industry) essentially said agents will get rewarded for the revenue generated by the investment funds as well. For better or worse, she mentioned that included trailer fees. I didn't ask further about formula or incentive schemes, as I know every biz activities will have its own profit margin and knowing full details serve no purpose to my work back then.

Now, don't get me wrong. I myself purchased a ILP and I understand the product bundle. But it doesn't mean that agents can simply talk or hide info about said products when asked. that is unethical. Choosing to remain quiet is a different story (I noticed some agents do that here, and that is completely fine as it is a free public forum). Threatening others who are sharing info is outright despicable.

A simple example is like a store selling a full gaming computer system vs selling individual parts. Savvier persons can assemble one themselves, while others choose to get a the full system. No right, no wrong.

(yeah, I also understand that sometimes, a client will choose not purchase the bundle when they find out how much margin the seller is making. Such client always exist, and as sales people, just need to educate the client better: No one does things for free.... Just see the 161% of annual premium as commission for the agent... some just cannot stomach this cost, but they don't realize that such is the market here. either buy or don't buy or find alternatives)

Eitherway, I am not here to break anyone's rice bowl... This is just a public forum, and lets just make it informative at least for all.

Aug 30 2023, 04:16 PM

Aug 30 2023, 04:16 PM

Quote

Quote

0.0302sec

0.0302sec

0.57

0.57

7 queries

7 queries

GZIP Disabled

GZIP Disabled