QUOTE(codercoder @ May 2 2024, 10:02 AM)

I am paying rm275 for plan 200. I think got 2 years already. if switch to medisaver, I think save around rm600 per year.

that person who recommended me can some kind of referer fee

this one

https://www.lonpac.com/personal-insurance/health/medisecure is lonpac generic product. not the one they design for medisaver.

Yup. You are focusing on how much you save per year. But what are you getting for paying that 275? Do you know? What other coverage attach to your IL policy?

Anyway, i admit budget is an important concern for many but what if i have a better option than medisavers that is about the same price? How would you feel? (Just giving general advice, you can sought out options but i am not agent, i can propose you anything). Anyway, is this medisecure same as medisavers? I can help provide more advice if i have more information. This medisecure having less benefit, naturally less cost to you as customer.

I wrote this somewhere to another person, i just copy paste again... i know i'm bombarding you with questions but buying insurance is not buying a tshirt.

QUOTE

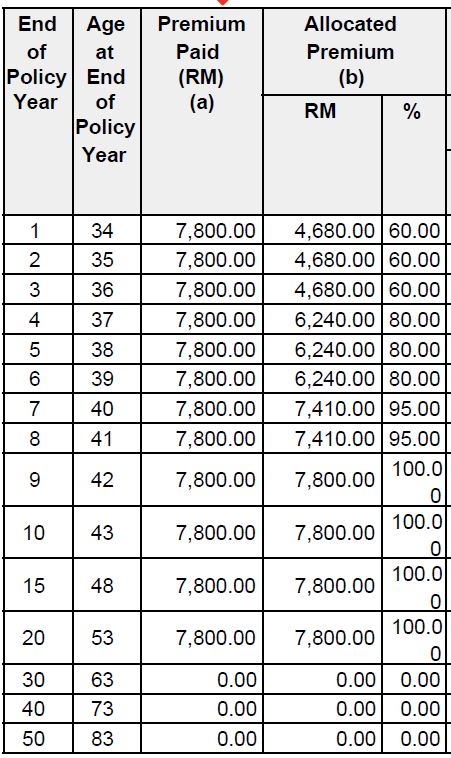

Changing insurance plan is not like changing your phone postpaid plan. There is alot of fees that you have paid. And you may pay more if you buy a new one. Which is why BNM always have this warning that they force the companies to put in. Buying a life insurance is a long term commitment, it is not advisable to switch plans due to the high initial cost.

But what most people dont know is, you can go back to AIA ask to reduce the premium instead of getting another plan that you requires you to pay rm50 less. There are limitations adjusting premium but for simplicity, let's assume it can. In the world of mobile postpaid plan, it may have the same effect. In the world of insurance it is not the same. I dunno how to explain how it's not the same but that warrants a separate reply and post all together.

The actions available to you arent just 0 and 1 where you keep or you say bye bye. There is something in between.

Ok. Having said that, you "only" been in it for 2 years. Although 1st and 2nd year charges are the highest, you can still "take yourself" out i suppose. If year 5 or 6, i really strongly recommend think 3 to 4 times because i wrote what's up there.

It's tedious, it's alot of work, but it's worth putting the effort to find out why you pay 275 every month. Else you will come back again few years down the road, aiya, AIA still better, more panel hospital, i think i want to switch back to AIA. Then you end up enriching the pockets of agents or people who earn referral fee and does not benefit you and in fact, not benefitting the insurance company too.

This post has been edited by adele123: May 2 2024, 10:47 AM

Mar 2 2024, 12:58 PM

Mar 2 2024, 12:58 PM

Quote

Quote

will look further into it.

will look further into it.

0.0294sec

0.0294sec

0.62

0.62

7 queries

7 queries

GZIP Disabled

GZIP Disabled