Nov 4 2021, 01:12 PM

Nov 4 2021, 01:12 PM

QUOTE(tigerjkt @ Nov 4 2021, 12:23 PM)

I guess he used 5.5% / 4 = 1.38%. But the point is, you put money there for 3 months, then you cannot annualized it using 12 months period to derive the return%. That's very misleading

i get what u r saying, but u mixed up the termthey refer 'real/actual return' to 1.38% is when they DID NOT annualised the return, hence u do not see the p.a.

but i agree with your point that we should refer to the annualised return (p.a.) for comparison

the daily compounding interest should also be taken into consideration

there is one issue which i m not quite sure about

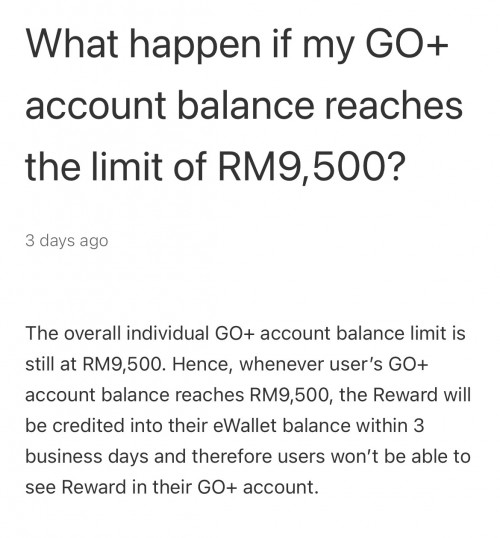

the GO+ maximum limit is RM 9,500, not sure if they will accumulate the bonus earnings since it will be payout to ewallet instead

QUOTE(tan_aniki @ Nov 4 2021, 12:57 PM)

guys, 4%pa is per annum, 1 Nov to 31 Jan only 92 days, so over these period you only got 4% / 365 x 92 ~= 1%

as for the standard rate we assume 1.5%pa, so you will get the usual 1.5% / 365 x 92 ~= 0.378%

so total you will get 1.378% of RM9500 = RM130.91 at the end of 31 Jan 2022

and that is the pointas for the standard rate we assume 1.5%pa, so you will get the usual 1.5% / 365 x 92 ~= 0.378%

so total you will get 1.378% of RM9500 = RM130.91 at the end of 31 Jan 2022

annualised return is easier for comparison

Quote

Quote

0.2848sec

0.2848sec

0.43

0.43

7 queries

7 queries

GZIP Disabled

GZIP Disabled