Ever wonder why your agent ask you surrender after 2 years and not anytime before that? your agents have indirectly asked you to buy a new policy, pay MORE premium, PAY her COMMISSION AGAIN and now you end up with 2 policies. the reason she asked you to surrender the old one after 2 years is because she will get to enjoy commission on PruWith You (PWY). if you surrender within 1 year, she will get nothing.

There is always one warning by insurance companies whereby insurance is meant for long term and switching is costly because of high initial cost. Based on this statement you really have to study whether do you really need this PWY or not.

your existing lifetime limit of 1 million is comparatively low in the market, but still more than enough. My own policy 120k per year, 720k per life, i haven't upgraded it yet but i'm planning to upgrade soon. However, if you do want to upgrade, you can upgrade. there are usually 2 options, upgrade existing or buy new policy.

Upgrade existing is cheaper, buy new policy is usually more expensive. but i do have to admit, sometimes there's a limit to how much you can upgrade in your existing but my point is, this probably wasn't presented to you by your agent and you buta-buta sign up new policy and getting weird comments like, then the old one no need to pay can only surrender after 2 years. of course you can surrender anytime

Without knowing the details it will be hard to judge whether you need (choice of word is 'need' not should) paying for the old one but your agent has misled you by asking you buying a new one and simply asking you not to pay the old one. maybe she did the calculation but she was not transparent. your current policy is prulife or prulink one? how old is it?

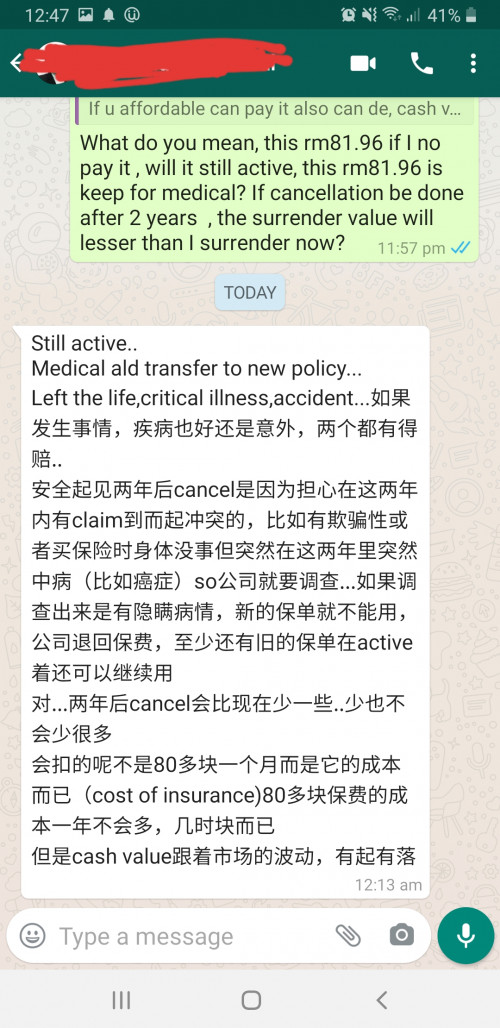

Hi Adele123, I not sure how to differentiate prulife or prulink, my type of assurance is prulife ready. I dont have much knowledge , I just simply thought is converting my existing plan to new plan, whereby my current premium change from rm190 monthly to rm220 monthly with medical claim limit upgrade to lifetime unlimited. I do plan to upgrade the medical from 1M lifetime to unlimited. Then when I check from this forum, then I sense something incorrect, so I seek for more advice from this forum to find out why I need keep both policy while she mentioned the current medical transfer to new policy.

May 17 2020, 12:49 AM

May 17 2020, 12:49 AM

Quote

Quote

0.1400sec

0.1400sec

0.52

0.52

7 queries

7 queries

GZIP Disabled

GZIP Disabled