Dec 31 2020, 12:43 AM

Dec 31 2020, 12:43 AM

QUOTE(Mike.Chang @ Dec 30 2020, 11:01 PM)

Any advantage to this plan? Really that good or not?

I'm a University Student, with little knowledge on insurance, going to graduate soon in 2021 May.

My insurance agent been bugging me to upgrade to this Medical Plan, since I recently changed the ownership of my plan under my name for above 18++ from my parents name.

Because he claims economy getting worst, and insurance company won't "give" such a good plan anymore in the near future...

First time getting these type of plans. Any advice and precaution that I will need to be warry about?

https://www.greateasternlife.com/my/en/pers...quiry-form.html

The Brochure is below:

https://www.greateasternlife.com/content/da...on-brochure.pdf

Deadline is tomorrow. He say can give me 15 day cancellation. But dunno what's the T&C.

He say can give me 15 day cancellation. But dunno what's the T&C.

I'll say grab it while you still valid to apply.I'm a University Student, with little knowledge on insurance, going to graduate soon in 2021 May.

My insurance agent been bugging me to upgrade to this Medical Plan, since I recently changed the ownership of my plan under my name for above 18++ from my parents name.

Because he claims economy getting worst, and insurance company won't "give" such a good plan anymore in the near future...

First time getting these type of plans. Any advice and precaution that I will need to be warry about?

https://www.greateasternlife.com/my/en/pers...quiry-form.html

The Brochure is below:

https://www.greateasternlife.com/content/da...on-brochure.pdf

Deadline is tomorrow.

He say can give me 15 day cancellation. But dunno what's the T&C.Age below 1- 30 can get from RM150-200 monthly depending riders (& age)

No hesitate I change for both my children.

And you got 15 days free look period. Here is the term in policy I copy :

FREE-LOOK PERIOD

Within 15 days after this policy has been received by you, you may return this policy to the Company. We shall then

immediately refund the sum of

· any amount of premiums that have not been allocated to purchase Units; and

· Total Investment Value of this policy, if any; and

· total values of the Units deducted for Insurance Charges and Policy Fees based on the Net Asset Value on the

Next Valuation Date

of your policy and cancel this policy subject only to the deduction of expenses incurred for the medical examination,

if any, of the Life Assured.

Meaning to say, grab 1st and still got time to learn and compare. Anyway, this is the greatest deal at the moment with similar premium.

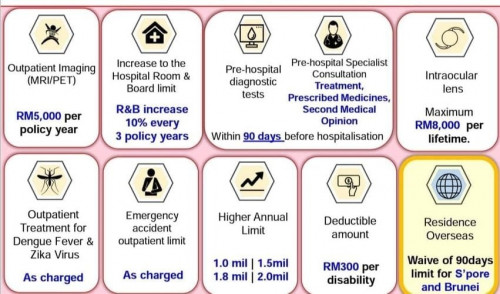

Simple feature summary

Quote

Quote

0.1309sec

0.1309sec

0.79

0.79

7 queries

7 queries

GZIP Disabled

GZIP Disabled