QUOTE(TOS @ Dec 3 2019, 11:42 PM)

That 200k limit is for ASB funds. No maximum limit on ASM, ASM2 and ASM3 fund holdings.

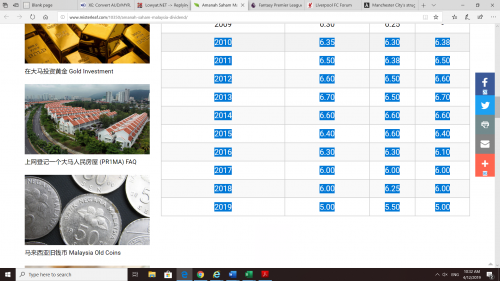

What are the returns like for ASM1, 2 and 3 in the last 10 years?Ultimate Discussions of ASNB Fixed Price UT, Magical UT only in Malaysia

|

|

Dec 4 2019, 09:01 AM Dec 4 2019, 09:01 AM

Return to original view | Post

#1

|

All Stars

12,267 posts Joined: Oct 2010 |

QUOTE(TOS @ Dec 3 2019, 11:42 PM) That 200k limit is for ASB funds. No maximum limit on ASM, ASM2 and ASM3 fund holdings. What are the returns like for ASM1, 2 and 3 in the last 10 years? |

|

|

|

|

|

Dec 4 2019, 10:39 AM

Return to original view | Post

#2

|

|

All Stars

12,267 posts Joined: Oct 2010 |

QUOTE(bourse @ Dec 4 2019, 09:12 AM) Thanks mateBut the yield is trending downwards for most of the funds. Not a good sign. Why are so many still interested in this?   |

|

|

Dec 4 2019, 11:18 AM

Return to original view | Post

#3

|

|

All Stars

12,267 posts Joined: Oct 2010 |

QUOTE(MGM @ Dec 4 2019, 10:52 AM) For those not financial savvy, these funds have so far been the 'safest' n higher yield. At 5% , its only a slight above FD rates. That is not too safe.  |

|

|

Dec 4 2019, 11:29 AM

Return to original view | Post

#4

|

|

All Stars

12,267 posts Joined: Oct 2010 |

QUOTE(beLIEve @ Dec 4 2019, 11:24 AM) in terms of losing principal/capital You do not lose your principal with FD. |

|

|

Dec 6 2019, 11:26 AM

Return to original view | Post

#5

|

|

All Stars

12,267 posts Joined: Oct 2010 |

QUOTE Financing approved: RM200,000 Takaful contribution: n/a + Protection amount: n/a + Protection term: n/a Total financing: RM200,000 Financing tenure: 37 years (max) Rate: 4.85% Monthly Payment: RM971/month Processing Fees: RM60 (one time, included in the first installment) 4.85% finance cost to receive around 5 to 5.5% total returns???? Am I missing something here? |

|

|

Dec 6 2019, 01:16 PM

Return to original view | Post

#6

|

|

All Stars

12,267 posts Joined: Oct 2010 |

QUOTE(bourse @ Dec 6 2019, 11:52 AM) Finance for ASB1 & ASB2. NOT any fp fund. I see. Its for ASB. A tongkat really. Dividend ASB1 6.50% Dividend ASB2 6% This is free money giving away. You are not missing anything here. Anyhow, not many bumi understand. |

|

|

|

|

|

Dec 6 2019, 03:18 PM

Return to original view | Post

#7

|

|

All Stars

12,267 posts Joined: Oct 2010 |

QUOTE(wild_card_my @ Dec 6 2019, 03:01 PM) You are missing quite a lot. Try reading up on: Compounding at 5% is better than compounding at 1.5% p.a 1. Amortization 2. Compounding interest Thank you. Apparently based on the above person's reply, plenty of non-bumi don't understand it either. As if they do not know that you can't simply compare annual interest rates and compounding returns; and proceed to make silly comments. I rest my case. So how does amortization bring a return on investment? |

|

|

Dec 6 2019, 03:41 PM

Return to original view | Post

#8

|

|

All Stars

12,267 posts Joined: Oct 2010 |

QUOTE(wild_card_my @ Dec 6 2019, 03:35 PM) Interest on the loans are paid based on a reducing balance. As you pay your installments, your interest payments get reduced. That's true. Provided all things being equal at that dividend being maintained. Right now I see the dividends on a down trend from 10 years back.On the other hand, you are probably already clear about compounding. For those who don't, compounding returns takes into account the previously accumulated returns plus capital when calculating the upcoming return So in general, people who keep on mentioning 4.85% vs 6.5% really has some understanding to do. For example of actual calculation: after 5 years of taking up RM200k financing, the 4.85% interest on a loan balance of RM189k yields a different number than a 6.5% on the now compounded RM275k value. |

|

|

Dec 6 2019, 03:58 PM

Return to original view | Post

#9

|

|

All Stars

12,267 posts Joined: Oct 2010 |

QUOTE(wild_card_my @ Dec 6 2019, 03:55 PM) then we can discuss the compounding returns, and when I said returns, it includes negative returns as well. Thus you may even have negative returns over the years like properties, or depreciation like cars. 4.85% vs 6.5% is a start. It gives an indication of the expected premium earned. Nothing wrong with that.But to talk about 4.85% vs 6.50% is just a folly, as if you can't relate the reducing balance interest (4.85%) vs the compounding returns (6.50%) |

| Change to: |  0.0395sec 0.0395sec

0.48 0.48

7 queries 7 queries

GZIP Disabled GZIP Disabled

Time is now: 26th November 2025 - 05:39 PM |

Quote

Quote