QUOTE(Unkerpanjang @ Jan 19 2023, 06:05 AM)

Respects! No stopping you once you set a goal...!! Wishing Mr Wolves a successful asnb journey with big pot of gold at the end of rainbow.

Unker is a simple person, your asnb determination n explanation gave Unker the confidence n emotional support to hang on to my asnb purchases.

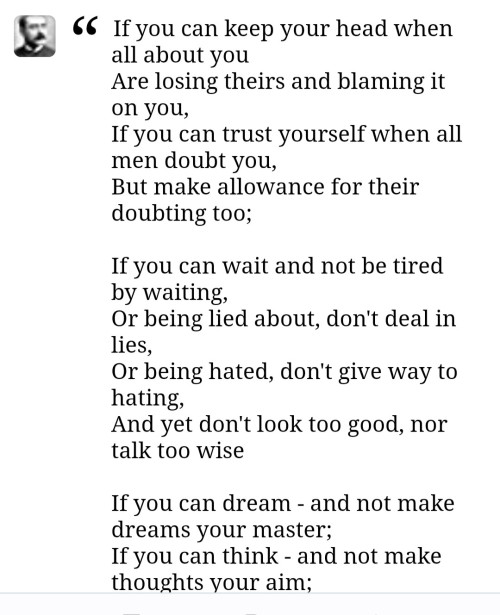

Really a Rudyard Kipling moment.

Thank you. And yes i am stubborn

Ah.. you are shaken and wondering if you should sell like some of the ppl here. Well, this is not financial advice.

My personal opinion. First of all, this is as good as a bank can get. PNB is gov entity (or semi gov) and asnb is under the PNB umbrella. Can they screw up? Sure. But it's something the gov created to enrich the bumi (then the non). So it is as stable as it gets. Unless Malaysia goes bankrupt, i don't see how this thing will go bust. And if Malaysia do go bankrupt, then where you put in Malaysia is pointless. This is better than MAS coz MAS went private. This one still under gov. And look at MAS

most importantly, they cannot screw up coz bumi uses it too.

Second of all, it is liquid. You can withdraw 2k per month and if you need more, go to the branch or any banks in Malaysia. It's like a universal bank that all banks recognized and service. That should say something about it's reliability. You can even go post office for this.

Third of all, its fixed fund. Aka no matter what happen (unless they change the fixed fund), it will forever be rm1 per unit. Like i said previously. Worse case scenario you lose time and get 0 interest for a year. By that time you can just liquidate them.

These fundamentals don't change. Unless it changes then i might act on it. Now we talk about potentials. If you look at interest rates only. Yeah.. they "could" potentially be lower by a bit. But don't forget. If 2023 March announced 4% interest rate, it actually means April 2022 (last year) until March 2023, aka previous 12 months. Not future 12 months. If you look at data, from April 2022 to march 2023, what's the average interest rate of banks? We talking about average. I believe "highest" until december 2022 (last year) was 3.8%. 4% and above only happened around january 2023. So technically they are doing better than FD. On "average". They might not beat every bank and every scenario out there but they do beat majority. If you are chasing the best of the best of the best then yes they sucks. But with that you have to chase like no others as well. Not everybody have access to every bank and have account in every bank and access thier privileges and combos products and fulfilled thier requirements for the special rate. And definitely i am not going to go there every 12 to 18 months to redo all over again as most require "fresh fund" aka you need to withdraw and then put into another account and then withdraw or transfer over every cycle.

In terms of other vehicles, yes there is reits, oversea investments, sp500, US bonds, ETFs, insurance cum investment, mutual funds and properties for rentals and so on and so forth which can gives you higher returns. Even stocks. The question will then become, do you know how to do it? And can you weather the price volatility and the risk involved? Do you wanna lock your funds up for a period of time? 5 years? 10 years? Do you want to look at it everyday and do maintenance? The higher the yield the more you need to do. Property need to pay tax and lawyer fee to acquire. You need to find a "good" tenant or you are toast. You need contracts and you need maintenance. It sounds good. But when you start doing it, it's a different story. Unless you are lucky you get a good place and you are lucky the lawyer did not overcharge and you are lucky to have a very good tenant for next 20/30 years (loan time) and interest rates doesn't eat into your income and lhdn doesn't knock your door and no natural disasters or pest did not come say hello. If you are young (below 30s) then yes coz you got plenty of time and energy to play with this. But even so, i still choose this asm. 0 buy fee 0 sales fee 0 maintenance fee 0 risk 0 fuss. Buy and forget and every year wait dividends.

And that is why i so rajin lo when i see asm1 units available. Can correct me if i am wrong and that's the drive behind my decisions. If asm units no longer available and if i can last 5 more years, i will put into kwsp coz higher yield and same advantages except need to wait until 50 to withdraw some and then 55 to withdraw when i need. Kwsp also have a guranteed minimum interest every year. So it is better in some sense if not for the age requirement to withdraw.

This post has been edited by Wolves: Jan 19 2023, 10:50 AM

Jan 18 2023, 02:25 AM

Jan 18 2023, 02:25 AM

Quote

Quote

0.0381sec

0.0381sec

0.57

0.57

7 queries

7 queries

GZIP Disabled

GZIP Disabled