Outline ·

[ Standard ] ·

Linear+

myTHEO MY, Invest in a Moment

|

zacknistelrooy

|

Jul 6 2019, 04:19 PM Jul 6 2019, 04:19 PM

|

|

QUOTE(CardNoob @ Jul 6 2019, 08:59 AM) SA for 36% risk is rather US heavy. It isn't Most of the top holdings in SA are MNC expect the small cap and reit holdings for the high risk holders If the world and US are doing well then ultimately those companies do well Would you rather that then take country and currency exchange risk like South Korea where Samsung just announced a plunge in profits. This is the EWU vs EWJ vs SPY with dividend reinvested

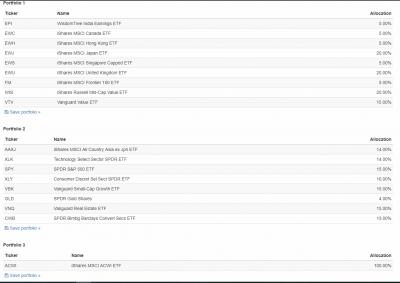

For anyone interested here is a simple back test of the assets Port 1 is MyTheo, Port 2 is Stashaway and Port 3 is All country world index ETF Allocations will be slightly off but should give everyone the general idea Dividends are reinvested and port is rebalanced quarterly Asset Allocation Performance

Performance Annual Returns

Annual Returns This post has been edited by zacknistelrooy: Jul 6 2019, 04:26 PM

This post has been edited by zacknistelrooy: Jul 6 2019, 04:26 PM |

|

|

|

|

|

zacknistelrooy

|

Jul 7 2019, 05:54 PM

|

|

|

QUOTE(Ancient-XinG- @ Jul 6 2019, 05:23 PM) Hmmm. Based on the graph, SA>MT Yes A lot of MyTheo ETF has currency exposure which is one of the main reason for underperformance Also a couple of them have a high dividend yield I am not sure if they are trying to just differentiate themselves or have another reason for their picks. Only their CIO would be able to answer that question. They have essentially taken a value and weak dollar view overall based on their picks Also they have a significantly higher allocation towards financial firms and industrials which are notoriously cyclical sectors

|

|

|

|

|

|

zacknistelrooy

|

Jul 7 2019, 06:03 PM

|

|

|

QUOTE(David_Yang @ Jul 5 2019, 08:41 PM) Just checked one: Sounds not so good: If want to read full report need to pay  This is the best that I could get QUOTE Role in Portfolio

This fund is not the best vehicle for investors seeking passive exposure to the Japanese large-cap equity market. An unreasonably high management fee and the availability of peers that track broader and more representative indexes such as the MSCI Japan IMI and Topix means we cannot award this fund a positive rating.

The market-cap-weighted MSCI Japan Index tracks the performance of around 320 large- and mid-cap Japanese companies, which represent around 85% of the total market value. With an ongoing charge of 0.59%, the fund is one of the most expensive exchange-traded funds tracking Japanese equities and much pricier than other ETFs tracking the very same index (for example, the HSBC MSCI Japan ETF with an ongoing charge of 0.19%).

There are also numerous funds that track broader and more representative indexes such as MSCI Japan IMI and FTSE Japan for a lower fee. The excessively high management fee has seen the fund shrink in a market in which rivals have gathered assets.

Fund performance has been uninspiring, having matched or slightly edged out surviving category peers on a risk-adjusted basis over three, five, and 10 years.

The annual tracking difference (fund return less index return) has hovered around the ongoing charge over the past three years. This suggests that the fund has tracked its benchmark tightly (gross of fees). Net of fees, however, the fund has unsurprisingly been one of the worst-performing MSCI Japan trackers.

Investors in all foreign markets should be aware of the potential impact that currency movements can have on returns. For example, a UK investor in the Japanese equity markets is exposed to both the returns on the underlying market and the fluctuations in the pound/yen exchange rate. Although the fund offers broad and representative market exposure, several broader and more representative passive offerings exist.

The fund also charges an indefensibly high fee, which has helped make it one of the worst performing MSCI trackers over recent years. For these reasons, we have awarded this fund a Morningstar Analyst Rating of Neutral. |

|

|

|

|

|

zacknistelrooy

|

Jul 9 2019, 06:47 PM

|

|

|

QUOTE(lee82gx @ Jul 9 2019, 05:57 PM) My completely uncle uneducated guess is that because Mytheo is in part founded by many Japanese, the underlying "algorithm" may be also Japan market biased. Of course, $$ speaks so we need to see how well it will do in the long run, especially seeing as their own back test says it works... Do you happen to have the backtest they did? If so, could you please post it here I looked at their Japanese operation and some of their ETF are different https://theo.blue/portfolio This post has been edited by zacknistelrooy: Jul 9 2019, 06:48 PM

This post has been edited by zacknistelrooy: Jul 9 2019, 06:48 PM |

|

|

|

|

|

zacknistelrooy

|

Dec 11 2020, 12:34 AM

|

|

|

MYTHEO from the start has had a tilt towards value and a weaker dollar so as long as those trends continue like for the past 3 months then MYTHEO will outperform. Below is an example of the iShares MSCI United Kingdom ETF (EWU) vs iShares Currency Hedged MSCI United Kingdom ETF (HEWU) to show the effect from the dollar depreciation from the March bottom.  This post has been edited by zacknistelrooy: Dec 11 2020, 12:37 AM This post has been edited by zacknistelrooy: Dec 11 2020, 12:37 AM |

|

|

|

|

Quote

Quote 0.0260sec

0.0260sec

0.30

0.30

7 queries

7 queries

GZIP Disabled

GZIP Disabled