oof

KWEB has 10% of its holdings in T*nc*nt

can see it drop pretty sharply too

can see it drop pretty sharply tooalthough in long run unlikely to lose much since T*nc*nt has almost no competitors

Investment StashAway Malaysia, Multi-Region ETF at your fingertips!

|

|

Mar 15 2021, 06:55 PM Mar 15 2021, 06:55 PM

Return to original view | IPv6 | Post

#101

|

Senior Member

2,610 posts Joined: Aug 2011 |

https://www.bloomberg.com/news/articles/202...intech-business

oof KWEB has 10% of its holdings in T*nc*nt can see it drop pretty sharply tooalthough in long run unlikely to lose much since T*nc*nt has almost no competitors |

|

|

|

|

|

Mar 15 2021, 07:05 PM

Return to original view | IPv6 | Post

#102

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

QUOTE(Merubin @ Mar 15 2021, 05:14 PM) wahai, expert expert sekalian, i was searching for ETF fund and bump into this, as its kinda lengthy to read all the detail from 2019. i think its easier for fellow members here to share experience. I have some double on this platform hoping to have some answer around +1 to above comments not recommending to park emergency funds in SAMY because of requiring 3-5 biz days from withdrawal order to bank account, and on top of that there's forex risk (as all ETFs traded on SAMY is in USD), which combined with even the lowest risk index of 6.5% can be very painful if timing is bad 1. from my understanding stashaway is a auto trading platform where it trade base on ETF? 2. does anyone withdraw the fund from trust? how long does it takes? 3. i have some emergency fund available looking forward to park on a better liquidity place with lower risk, just wondering whether suitable or not  would recommend to just keep emergency funds in conditional high yield savings account or a hybrid FD+savings account like Frank by OCBC, if emergency funds less than 6 months' worth of expenses if more than 6 months' expenses maybe can do a split of 70% in saving account/FD and 30% in low risk SAMY portfolio, but honestly not that big of a benefit unless you've got a lot of assets and can afford the risk |

|

|

Mar 15 2021, 07:27 PM

Return to original view | IPv6 | Post

#103

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

Additional advice:

Ultimately remember that emergency fund is for EMERGENCY, any growth should be seen as a "bonus if can afford" only and not a necessity. if concern about inflation you should be able to top up extra anyway from additional monthly savings or bonuses if you find that your monthly expenses keep going up and your emergency funds can't keep up, it's a sign that you've fallen into "lifestyle inflation" trap (read: spending beyond your actual means) and it's time to sit down and have a brutally honest financial evaluation with yourself to cut back expenses |

|

|

Mar 16 2021, 12:08 PM

Return to original view | IPv6 | Post

#104

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

QUOTE(blackchides @ Mar 16 2021, 11:04 AM) Yeah, think you're right, it could be more for US roboadvisors who also have a lower fee structure overall. In this and other article, they did say generally that they have strong unit economics and healthy cash holdings, so yeah, I think SA should do alright. SA's fees are noted to be one of the higher robo fee structures out there In Singapore, traditional banks have started offering roboadvisor-type products too though. Interested to see if Malaysian banks will follow suit - but they may not wanna cannibalize their own business. so I think they should be doing ok if their AUM continues to grow at their current rate. There's little competition here in Malaysian robo-advisor landscapeUnlikely so soon that banks will release their own robo as Malaysia still have poor percentage of internet savvy users and low trust in online investing. People still prefer brick n mortar banking 😅 maybe 4 to 5 years more I think. People here still rather invest in mutual funds or in FDs/gold. This post has been edited by DragonReine: Mar 16 2021, 12:10 PM |

|

|

Mar 16 2021, 12:43 PM

Return to original view | IPv6 | Post

#105

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

QUOTE(Hoshiyuu @ Mar 16 2021, 12:12 PM)    Stashaway's doing great from a pure popularity standpoint I guess? Malaysian are a massive, massive sucker for UT though. I've still got 500 in both Wahed and myTheo, but mostly because I am just interested to benchmark all 3 of them (incl. Stashaway) for a full year. But as I use Stashaway more and more I really don't see a reason to be on other platform, and I certainly don't see Malaysian Banks offering anything that would come close to it. Not to mention I already have an exit strategy in mind for Stashaway once I have a bigger capital... don't see much promos for other investment platforms. They also do a lot of seminars and educational videosalso I think people like SAMY because it's slick UI and moderately transparent fee structure, easy to understand mostly |

|

|

Mar 16 2021, 12:55 PM

Return to original view | IPv6 | Post

#106

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

QUOTE(Hoshiyuu @ Mar 16 2021, 12:46 PM) Slightly disagree on the transparent fee structure. I'm willing to change my opinion when they provide a fee calculator. As it is, its very misleading - I won't be surprised if your everyday person would thought that "oh if I have RM1m invested the fees are RM3000 a year" reading their fee's page. This is true, although I'm mostly comparing with MFs 🤣 I think the clearest one for fees is Raiz? But SAMY giving a proper fee calculator would be godsend, except it also exposes that they aren't the cheapest on the market right now LOLOL Hoshiyuu liked this post

|

|

|

|

|

|

Mar 16 2021, 07:01 PM

Return to original view | IPv6 | Post

#107

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

QUOTE(DragonReine @ Mar 16 2021, 12:08 PM) SA's fees are noted to be one of the higher robo fee structures out there And I oop so I think they should be doing ok if their AUM continues to grow at their current rate. There's little competition here in Malaysian robo-advisor landscapeUnlikely so soon that banks will release their own robo as Malaysia still have poor percentage of internet savvy users and low trust in online investing. People still prefer brick n mortar banking 😅 maybe 4 to 5 years more I think. People here still rather invest in mutual funds or in FDs/gold. https://fintechnews.my/26573/wealthtech-mal...a-robo-advisor/ QUOTE Kenanga Investment Bank revealed on Monday that it had received a Digital Investment Manager license from Securities Commission Malaysia. The newly granted license allows for Kenanga to operate a robo advisor. Currently, there are 7 other companies in Malaysia with a Digital Investment Manager license namely; Akru, BH Global Fintech, GAX MD, Raiz Malaysia, StashAway, UOB Asset Management, and Wahed Invest. Kenanga previously received an approval in principle from the regulator in 2020, they previously revealed to Fintech News Malaysia that their robo advisory platform will be named Kenanga Digital Investing and is slated for 2021 launch. Interesting, now got big fish join in. Even UOB's UOBAM Invest was a hybrid robo+direct buy platform. Wonder if Kenanga will focus on ETFs like SAMY or UTs like Raiz/Wahed This post has been edited by DragonReine: Mar 16 2021, 07:08 PM Hoshiyuu liked this post

|

|

|

Mar 17 2021, 08:29 AM

Return to original view | IPv6 | Post

#108

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

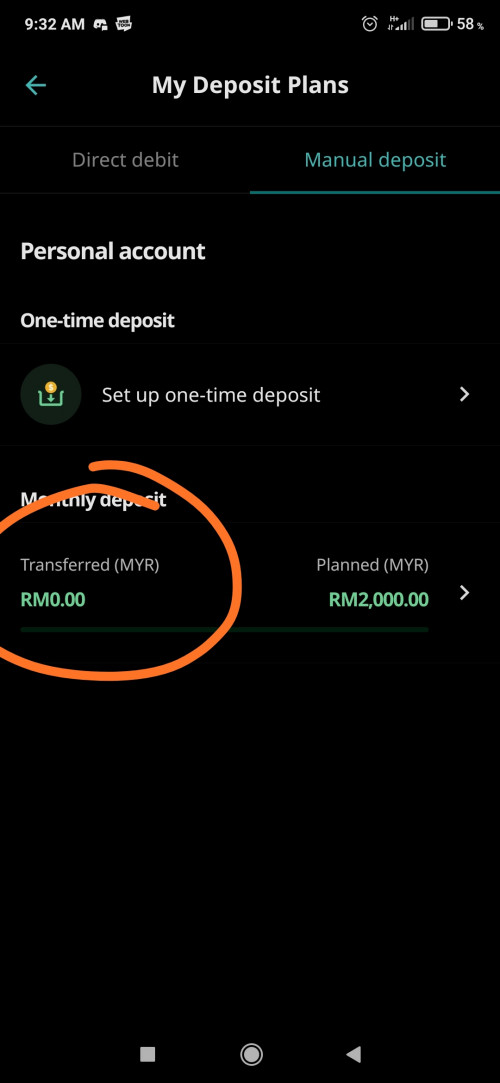

QUOTE(pinksapphire @ Mar 16 2021, 11:56 PM) I'll get reprimanded for asking this, but I browsed information on recurring deposit and the posts here mentioned about monthly settings, which I can also see from SA app. How do you guys do it for weekly? Or some people even do it daily. I'm not familiar with Jompay, which I've seen been mentioned some times here, if that's the solution, I appreciate your patience in explaining to me. Thanks. You can do recurring on different dates, certain banks allow you to schedule/do standing instruction to do weekly for Jompay (however you'd need to create manual deposit amount in SA every time before the scheduled payment executes) |

|

|

Mar 17 2021, 09:33 AM

Return to original view | IPv6 | Post

#109

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

QUOTE(pinksapphire @ Mar 17 2021, 09:17 AM) Oh my, have to set up manual deposit. That's not very 'auto' friendly then. Only for weekly JomPay la SA doesn't give option to do weekly deposit in a user friendly way.Monthly then there's an option to put a monthly deposit allocation in StashAway and then schedule the JomPay through your own bank, SA will "reset" the transfered amount back to zero at the start of each calendar month  |

|

|

Mar 17 2021, 09:43 AM

Return to original view | IPv6 | Post

#110

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

QUOTE(sohailili @ Mar 17 2021, 09:32 AM) If you are planning to deposit weekly on a fixed amount basis, Doesn't work that way, SA won't invest the money until hit the full amount (I tested b4), so in the end it's effectively only a monthly deposit.1. Set monthly deposit in Stashaway 2. Set weekly deposit via CIMB jompay This post has been edited by DragonReine: Mar 17 2021, 09:43 AM |

|

|

Mar 17 2021, 09:55 AM

Return to original view | IPv6 | Post

#111

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

QUOTE(sohailili @ Mar 17 2021, 09:47 AM) been on this setup close to 2yrs now Oh you can actually do that? Interesting, didn't think it'll work that way. 1. Set monthly xx amount in stashaway. 2. CIMB jompay xx amount on weekly basis. (xx amount is the same. If i set 50 at Stashaway monthly deposit, i set 50 for jompay transfer) Monday jompay transfer Monday Stashaway confirm fund received Monday/Tuesday fund conversion to USD Monday/Tuesday/Wednesday buy order I assumed that it'll not deposit money if you already transferred the full amount. My bad. sohailili liked this post

|

|

|

Mar 17 2021, 01:22 PM

Return to original view | IPv6 | Post

#112

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

QUOTE(zstan @ Mar 17 2021, 01:16 PM) credit card with high credit limit and medical card Some of these not always accessible depending on circumstances (health, salary) While it's true that it's 'unlikely' the reason it's called emergency is you really never know what might happen  |

|

|

Mar 17 2021, 05:40 PM

Return to original view | IPv6 | Post

#113

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

😅 kidnapping and accidents went beyond what's the usual definition of emergency fund ady, that kind of sudden accidents should be insured or report police LOL

anyway, liquidity is one thing but if you are ok and secure with keeping it in Simple or low risk portfolio for the additional gains, that's 100% ok if it suits your needs and your appetite personally I'm very risk adverse for my emergency funds and because I have access to a high interest savings account, I'd rather keep in that since Simple's projected interest is lower. Credit card I keep for the credit profile and member benefits only |

|

|

|

|

|

Mar 22 2021, 10:08 AM

Return to original view | IPv6 | Post

#114

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

Ultimately it's you pay for the convenience of not needing to research individual ETF performance + the ability to buy fractional shares + cheaper way to diversify, if use SA

obviously DIY will be cheaper but need knowledge, time, and large capital |

|

|

Mar 22 2021, 10:32 AM

Return to original view | IPv6 | Post

#115

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

QUOTE(MUM @ Mar 22 2021, 10:24 AM) but postings in last page (653) mentioned SA "cheaper" As mentioned above and after analysis, "cheaper" to go SA if low capital and/or want a very diversified portfolio.If have a lot of money to invest with and will only stick with one or two ETFs, in decades it'll be "cheaper" than SA because of how fees work. But not many have the capability or capital to do that honsiong liked this post

|

|

|

Mar 22 2021, 11:57 AM

Return to original view | IPv6 | Post

#116

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

QUOTE(MUM @ Mar 22 2021, 10:42 AM) i read "Small to moderate albeit anything under USD100k SA will perform better. 🤣 it's the same problem in long run of overall "net gain" that SA themselves talk about when comparing SA fees to mutual funds fees. In 10, 20, 30 years, fees of managing investments adds up. So "perform" better maybe not the best term for it (?) IF USD100k = low capital.....than DIY ETF is > USD100k  to be "cheaper" to be "cheaper"Obviously this is relative and in Malaysia at least, our median income puts the majority of Malaysian in "small capital" territory when they invest |

|

|

Mar 22 2021, 12:36 PM

Return to original view | IPv6 | Post

#117

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

QUOTE(MUM @ Mar 22 2021, 12:33 PM) As long as there is money made in the end that is significantly larger than the fees... I guess many don't mind. Pretty much yes. The whole fee structure thing usually only matters for people who really calculative about net gains |

|

|

Mar 23 2021, 11:00 AM

Return to original view | IPv6 | Post

#118

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

QUOTE(PPZ @ Mar 23 2021, 10:35 AM) maybe perhaps 15 to 20% will be good enough? Normally the rule of thumb of investing will be having 2 portfolios where one is high risk and one is low? 15-20% p.a. possible if based solely on past performance of the higher risk portfolioshowever as any savvy investor can tell you, past performance ≠ future performance. Also that high risk ≠ high reward 😛 2020 gave SA very unusual high returns because of the bull run of tech stocks, but don't expect something to happen like that constantly for something as passive and as diversified as SA's portfolios, 15% is pretty unrealistic, I would actually say even 10% p.a. is considered "amazing" performance. 15% p.a. you want that level of return, you're better off gambling on crypto or meme stocks (and there's a reason why I'd call it gambling lol) 2 portfolios, one high and one low risk, will average out the overall performance of your account if you already have low risk elsewhere (EPF/SSPN/ASB/ASM) and you're investing in SA for retirement + you're under 40 years of age, my dua sen is don't choose anything lower than 22% the only reason you'd want a low risk portfolio is if you plan to withdraw it within the next 3 to 10 years, either because you're already near retirement age, or you're planning for something like wedding or trip and are willing to risk the money a little to get potential extra bonus money (but if that's the reason for holding a low risk portfolio, please for the love of your future self, don't ever commit 100% of your planned budget into SA, and please withdraw immediately when hit your "goal" amount even low risk doesn't mean it's impossible for you to end up in negative returns if you wait too long and are forced to withdraw at bad time)This post has been edited by DragonReine: Mar 23 2021, 11:11 AM cucumber liked this post

|

|

|

Mar 23 2021, 06:33 PM

Return to original view | IPv6 | Post

#119

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

QUOTE(Macam Yes @ Mar 23 2021, 06:17 PM) hi, may i know Stashaway really can make money? 1) Yes, but returns not guaranteed. You may refer to their 2020 report here: https://www.stashaway.my/r/our-returns-2020any good example here? how much to invest ? how much profit get back? 2) There is no minimum or fixed deposit amount required, you can deposit how much you want, whenever you want. 3) This is an investment product, so returns are not guaranteed. StashAway can only give "projected" returns but it's not a guaranteed amount like fixed deposit interest rate. If market/economy good, then profit up. If you withdraw when market bad like in 2018 or in early 2020, then you can end up making losses. StashAway "profits" come from capital gains (read here to understand: https://www.investopedia.com/ask/answers/03...ent-income.asp) and sometimes dividends for portfolios with bonds. This post has been edited by DragonReine: Mar 23 2021, 06:37 PM |

|

|

Mar 25 2021, 09:08 AM

Return to original view | IPv6 | Post

#120

|

|

Senior Member

2,610 posts Joined: Aug 2011 |

I'm so glad I made a partial withdrawal when it was still high

|

| Change to: |  0.4297sec 0.4297sec

0.58 0.58

7 queries 7 queries

GZIP Disabled GZIP Disabled

Time is now: 29th November 2025 - 10:04 AM |

Quote

Quote