Oct 12 2022, 10:49 AM

Oct 12 2022, 10:49 AM

QUOTE(honsiong @ Oct 12 2022, 10:36 AM)

This guy doesn't understand the concept of hedging.

Not diversifyingn currency means you are solely at the mercy of Malaysia BNM monetary policy and Putrajaya's fiscal policy.

By investing abroad, I am not betting if Malaysia will outperform or underperform, or if Malaysia currency will moon or doom, I am hedging against MYR to ensure total ruin does not happen to me personally.

EPF is denominated in MYR and unlike PRS, your portfolio doesn't fluctuate along with market condition. If MYR hyperinflates, your EPF and FD are done for.

Do you want to end up like people in Venezuela, Argentina, Zimbwabwe, Brazil, Weimar Republic, Colombia etc?

I believe majority of average malaysian doesnt have the luxury to diversify their portfolio to overseas, or even have extra funds to perform currency hedging.....Not diversifyingn currency means you are solely at the mercy of Malaysia BNM monetary policy and Putrajaya's fiscal policy.

By investing abroad, I am not betting if Malaysia will outperform or underperform, or if Malaysia currency will moon or doom, I am hedging against MYR to ensure total ruin does not happen to me personally.

EPF is denominated in MYR and unlike PRS, your portfolio doesn't fluctuate along with market condition. If MYR hyperinflates, your EPF and FD are done for.

Do you want to end up like people in Venezuela, Argentina, Zimbwabwe, Brazil, Weimar Republic, Colombia etc?

What are the average Malaysia financial position? will have car loan, housing loan for own stay, maybe 1 more properties for investment...with the accrued loan and interest ongoing, normal average malaysian will priortising of settling their loan 1st before even think of investing/hedging abroad.....

And ya, i'm just another average malaysian.....

Quote

Quote

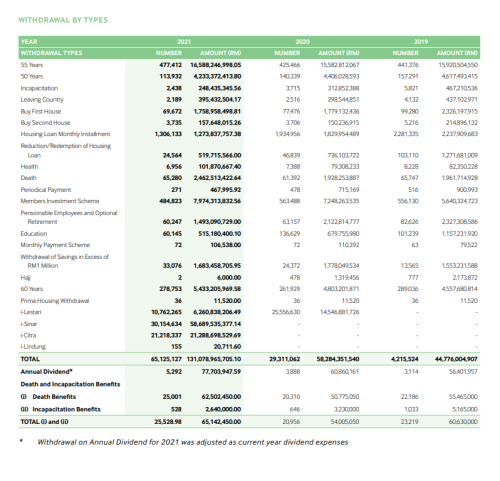

it seems that 1 ppl can perform multiple withdrawal for all the I-series

it seems that 1 ppl can perform multiple withdrawal for all the I-series

0.0254sec

0.0254sec

0.29

0.29

7 queries

7 queries

GZIP Disabled

GZIP Disabled