QUOTE(KingArthurVI @ Jan 18 2022, 01:30 AM)

Thanks for taking the time to write your recommendation

One thing I wanted to point out is that VWRA doesn't seem to carry small caps at all, the factsheet mentions it only carries large and mid-cap companies. But aside from that, I wholeheartedly agree with your general philosophy of holding total global market and chilling. I'm currently in the midst of rotating out of my Bursa dividend stocks into IBKR and looking to build a braindead portfolio. I was initially thinking SWRD+EIMI for some time (was thinking Eimi Fukada holding a sword.... lol

) because of the lower TER as compared to VWRA, but you made a good point about rebalancing and purchasing separate tickers adding to the hidden costs of the portfolio.

I also think about IWDA which is the OG developed markets ETF with 0.20% TER until SWRD came with 0.12% TER. If you compare IWDA's 0.20% with VWRA's 0.22% it's a no-brainer to just "VWRA-and-chill". I think this is a convincing-enough argument for me to go VWRA for my core "safe" portion of my portfolio.

If I have about RM50k, do people generally recommend lump sum since VWRA is relatively stable, or does it still make sense to DCA one's entry over maybe 3–6 months?

Yeap, VWRA unfortunately do not carry small caps, its not ideal but it's impact is smaller than you might think. I've posted this before somewhere else so don't mind the copy paste:

QUOTE

I've considered it and was basically my portfolio finalist (VWRA+VAGU or SWRD+WSML+EIMI+AGGH). My reasoning for my current choice is that -

1. I don't really need the small cap coverage.

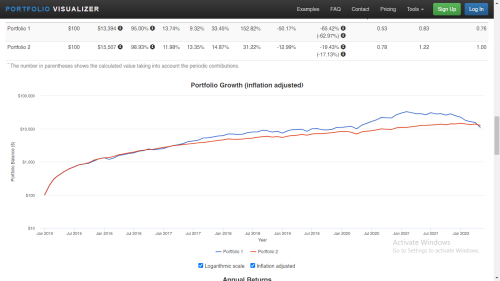

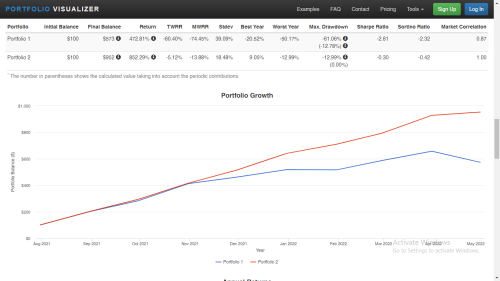

For assessing whether I needed the small cap, I compared VWRD (FTSE All-World) to FTSE Global All Cap Index (which VT tracks), VWRD has ~90% coverage of FTSE Global All Cap Index, which has ~98% coverage of FTSE Global Total Index (missing some microcaps).

If I recall correctly, the 5 year annualized return of both index is within 0.1% (14.3 vs 14.2).

So I came to the conclusion that I am essentially paying complexity in management and fees (TER and Transaction) of 4 Fund VS 2 Fund portfolio for essentially no difference in performance.

2.This is very feely crafty with not much basis, but Vanguard portfolio have the tendency to improve its fees overtime plus I prefer the spirit of the company, even though it's probably changing or going to with the loss of John Bogle.

Of course, if you believe in small cap value tilt or factor tilting in general, it's very easy to quickly dig back into the rabbit hole that we just crawled out of, like adding in AVUV/AVDV and just ignore the withholding tax since small caps rarely generate enough dividend to matter, and since they are US listed, the trading cost is way lower, etc.

But my personal recommendation is always, keep it simple, hold VWRA, spend the time on increasing one's income instead.

As for lump-sum vs DCA, it's a much debated topic so I'll just give you my personal opinion:

Time in the market > Timing the market, lump sum should give you a higher return - keyword being should.

While VWRA is relatively stable, with VWRA being basically ~60% US, and lump-sum into a decade long bull market is always scary, can you really withstand your 50k poofing to 30k overnight, and keep holding it for another decade or two?

For me, I have a good 20 year horizon minimum ahead of me, I'm looking forward to a crash to test my resolve, get cheap shares, and I believe in investing in VWRA enough that I haven't really found another place that I would put the majority of my money into (e.g. if for any reason VWRA drops 50% overnight, well, chances are nowhere else is really safe anyway), so personally I will lump-sum that amount in today.

Besides, I think I'll have much bigger regret seeing VWRA go up by 3 dollars when I only deposited only 5k out of 50k and end up panic FOMO lump-sum anyway

This post has been edited by Hoshiyuu: Jan 18 2022, 03:03 AM

This post has been edited by Hoshiyuu: Jan 18 2022, 03:03 AM

Jan 15 2022, 01:15 AM

Jan 15 2022, 01:15 AM

Quote

Quote

thanks for the much valuable insight! I like the idea of a braindead portfolio a lot, coming from someone who thinks buying dividend stocks on Bursa is even too much of a pain, so I think I'll go with your recommendation of VWRA over micro-managing multiple ETFs. Lump-sum investing is a bit scary for me, but I think my investment horizon is definitely very far out, 10-20 years, so short-term volatility shouldn't factor in too much over time.

thanks for the much valuable insight! I like the idea of a braindead portfolio a lot, coming from someone who thinks buying dividend stocks on Bursa is even too much of a pain, so I think I'll go with your recommendation of VWRA over micro-managing multiple ETFs. Lump-sum investing is a bit scary for me, but I think my investment horizon is definitely very far out, 10-20 years, so short-term volatility shouldn't factor in too much over time.

0.0396sec

0.0396sec

0.59

0.59

6 queries

6 queries

GZIP Disabled

GZIP Disabled