Attached thumbnail(s)

Insurance Talk V5!, Anything and everything about Insurance

|

|

Jan 22 2019, 10:07 PM Jan 22 2019, 10:07 PM

Show posts by this member only | IPv6 | Post

#181

|

Junior Member

26 posts Joined: Oct 2010 |

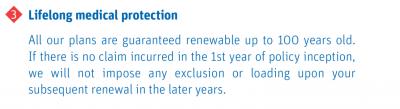

There’s one with no exclusion or loading if 1st year no claim..

Attached thumbnail(s)

|

|

|

|

|

|

Jan 22 2019, 10:18 PM

|

Senior Member

945 posts Joined: Apr 2016 From: Shah Alam |

QUOTE(kentloonghh @ Jan 22 2019, 09:52 PM) Centurial Plan 9 + Booster Plan 4 to get 1mil. 1 mil medical limit per annum? lifetime limit how much? |

|

|

Jan 22 2019, 10:40 PM

Show posts by this member only | IPv6 | Post

#183

|

|

Junior Member

26 posts Joined: Oct 2010 |

QUOTE(Mr.Weezy @ Jan 22 2019, 10:18 PM) 1 mil medical limit per annum? Yes 1mil per annum. No lifetime limit..lifetime limit how much? This post has been edited by kentloonghh: Jan 22 2019, 10:52 PM |

|

|

Jan 22 2019, 11:03 PM

|

|

Senior Member

945 posts Joined: Apr 2016 From: Shah Alam |

QUOTE(kentloonghh @ Jan 22 2019, 10:40 PM) Yes 1mil per annum. No lifetime limit.. how much premium p.a.? |

|

|

Jan 22 2019, 11:06 PM

Show posts by this member only | IPv6 | Post

#185

|

|

Junior Member

26 posts Joined: Oct 2010 |

QUOTE(Mr.Weezy @ Jan 22 2019, 11:03 PM) how much premium p.a.? 5k per annum at age 70. |

|

|

Jan 22 2019, 11:15 PM

|

|

Senior Member

945 posts Joined: Apr 2016 From: Shah Alam |

QUOTE(kentloonghh @ Jan 22 2019, 11:06 PM) 5k per annum at age 70. quite reasonable if it's sustainable to age 100  |

|

|

|

|

|

Jan 22 2019, 11:17 PM

Show posts by this member only | IPv6 | Post

#187

|

|

Junior Member

26 posts Joined: Oct 2010 |

QUOTE(Mr.Weezy @ Jan 22 2019, 11:15 PM) quite reasonable if it's sustainable to age 100 U know well the rate then... |

|

|

Jan 23 2019, 12:38 AM

|

|

Senior Member

1,309 posts Joined: Nov 2008 |

QUOTE(kentloonghh @ Jan 22 2019, 12:52 AM) Hi guys, I don’t understand why ILP is better....majority of the fund returns is actually average 4-5%. If based on average 4-5% return, high possibility that the fund will be empty by age 70, some by 65. After that you have to pay for high COI for your life insurance + medical card. For life insurance of 100k the COI could be 3k and medical card is around 5k. At the end you would be paying more than standalone medical card because of the additional life insurance cost. Is my assumption correct? Understand your concern, but returns is really not the selling points of ILP.Plus you have no choice but to continue paying higher premium for life in order to keep the medical card alive, kinda like a trap...? Sure, a lot of agents in the market use it as a seemingly good selling point (Wah see can get back some money woh, good right?). You may see ILP as a very transparent, very flexible life insurance plan (can add lots of riders), compared to traditional whole life participating life insurance, which is very rigid and not very transparent at all. The difference is that ILP exposes you to some risks, which is exactly what you pointed out, market risks. With that said, a good way to curb that is to maybe pay attention to the funds picked. Maybe you want a higher ratio in conservative/fixed income funds? That’s up to you to decide. Next, one of the most common problem in the market is forgetting to pay premiums, then the policy lapses. Klo medical card tu yg lapse masa nak pakai, die lah. ILP utilizes the fund value available to pay for the COI while something as trivial as ... credit card expired... or ... changed card..etc, happens and it wasn’t updated in a timely manner. When grace period habis, sama2 kita habis. Then like you said, return macam not that high. Yalah, after deducting the COI, memang tak hebat mne. But if you put the premiums together over the years, then put them side by side with a stand-alone plan, adding it all up together, tak beza mne pon. With all that said, yes, it is quite a pinch for some to fork out 1k or 2k extra a year to choose ILP instead of a standalone plan. It’s not wrong to choose one over another, it’s just what works for you. If ILP doesn’t sit well with your approach in managing your finances, then maybe a standalone plan is a better fit for you.  |

|

|

Jan 23 2019, 12:59 AM

Show posts by this member only | IPv6 | Post

#189

|

|

Junior Member

26 posts Joined: Oct 2010 |

QUOTE(JIUHWEI @ Jan 23 2019, 12:38 AM) Understand your concern, but returns is really not the selling points of ILP. Wow ur right. Thought my calculation was wrong initially. Just wanted standalone MC.....but few people want to layan...Sure, a lot of agents in the market use it as a seemingly good selling point (Wah see can get back some money woh, good right?). You may see ILP as a very transparent, very flexible life insurance plan (can add lots of riders), compared to traditional whole life participating life insurance, which is very rigid and not very transparent at all. The difference is that ILP exposes you to some risks, which is exactly what you pointed out, market risks. With that said, a good way to curb that is to maybe pay attention to the funds picked. Maybe you want a higher ratio in conservative/fixed income funds? That’s up to you to decide. Next, one of the most common problem in the market is forgetting to pay premiums, then the policy lapses. Klo medical card tu yg lapse masa nak pakai, die lah. ILP utilizes the fund value available to pay for the COI while something as trivial as ... credit card expired... or ... changed card..etc, happens and it wasn’t updated in a timely manner. When grace period habis, sama2 kita habis. Then like you said, return macam not that high. Yalah, after deducting the COI, memang tak hebat mne. But if you put the premiums together over the years, then put them side by side with a stand-alone plan, adding it all up together, tak beza mne pon. With all that said, yes, it is quite a pinch for some to fork out 1k or 2k extra a year to choose ILP instead of a standalone plan. It’s not wrong to choose one over another, it’s just what works for you. If ILP doesn’t sit well with your approach in managing your finances, then maybe a standalone plan is a better fit for you. |

|

|

Jan 23 2019, 01:33 AM

Show posts by this member only | IPv6 | Post

#190

|

Senior Member

2,866 posts Joined: Sep 2008 From: Wangsa Maju, KL |

QUOTE(kentloonghh @ Jan 23 2019, 12:58 AM) Wow ur right. Thought my calculation was wrong initially. Just wanted standalone MC.....but few people want to layan... dont worry here sure will have people layan you. i believed some agents will persuade you to take ILP. most importantly you know what benefit you can get from both standalone MC and MC attached to an ILP. End of the day you decide what you want. people that dont wanna layan you rugi lor...  |

|

|

Jan 23 2019, 10:18 AM

|

Senior Member

1,181 posts Joined: May 2005 |

Is there any new product that can cover a 60+ years old with heart disease and diabetes history?

|

|

|

Jan 23 2019, 02:14 PM

|

|

Senior Member

1,309 posts Joined: Nov 2008 |

QUOTE(kentloonghh @ Jan 23 2019, 12:59 AM) Wow ur right. Thought my calculation was wrong initially. Just wanted standalone MC.....but few people want to layan... Actually cuz not many comp. offering standalone mc now. But shop around ba. I’m sure the likes of AIA can help you |

|

|

Jan 23 2019, 09:30 PM

|

Senior Member

945 posts Joined: Jun 2012 |

QUOTE(kentloonghh @ Jan 22 2019, 09:52 PM) Centurial Plan 9 + Booster Plan 4 to get 1mil. Ah, yea that's quite ok but do get the agent/staff to explain the terms and conditions, for example: Know what you are signing then you'll be alright  Best, Jiansheng |

|

|

|

|

|

Jan 23 2019, 09:43 PM

|

|

Senior Member

945 posts Joined: Jun 2012 |

QUOTE(kbandito @ Jan 23 2019, 10:18 AM) Is there any new product that can cover a 60+ years old with heart disease and diabetes history? You can check out Allianz Diabetic Essential (ADE) and subsequently post your questions here if you have any. ADE is a medical card for Diabetes type 2. Best, Jiansheng |

|

|

Jan 24 2019, 11:24 AM

|

|

Junior Member

374 posts Joined: Feb 2014 |

Hi, Is Critical illness important?

A GE agent quoted me a Life Insurance with a rider for CI, which costs ~90 per month extra. As far as I understand, CI only pays out when the illness is at advance stage, and for GE, CI is part of the Life's SA. Isit worthwhile to pay RM90 extra per month just for that 'early payout'? As IMO, when your illness is at advance stage, the survival rate is also relatively low.. |

|

|

Jan 24 2019, 11:44 AM

Show posts by this member only | IPv6 | Post

#196

|

|

Senior Member

945 posts Joined: Jun 2012 |

QUOTE(Jdite @ Jan 24 2019, 11:24 AM) Hi, Is Critical illness important? There are different kind of CI coverage. It could be late stage coverage or early to late stage coverage.A GE agent quoted me a Life Insurance with a rider for CI, which costs ~90 per month extra. As far as I understand, CI only pays out when the illness is at advance stage, and for GE, CI is part of the Life's SA. Isit worthwhile to pay RM90 extra per month just for that 'early payout'? As IMO, when your illness is at advance stage, the survival rate is also relatively low.. Also, your age, occupation, smoker/nonsmoker, sex and amount of coverage will determine your premium. So whether it is worthwhile or not depends on these factors. Not discounting the fact that you will be getting the coverage. Best, Jiansheng |

|

|

Jan 24 2019, 11:46 AM

|

All Stars

10,162 posts Joined: Nov 2014 |

QUOTE(Jdite @ Jan 24 2019, 11:24 AM) Hi, Is Critical illness important? Critical Illness is quite important, I've customers who suffered cancer and good thing is there is payout from the CI benefit to buffer the living cost while going through daily life.A GE agent quoted me a Life Insurance with a rider for CI, which costs ~90 per month extra. As far as I understand, CI only pays out when the illness is at advance stage, and for GE, CI is part of the Life's SA. Isit worthwhile to pay RM90 extra per month just for that 'early payout'? As IMO, when your illness is at advance stage, the survival rate is also relatively low.. You may not want to be the lottery winner when it comes to critical illness that strikes all the sudden |

|

|

Jan 24 2019, 02:45 PM

|

|

Senior Member

945 posts Joined: Apr 2016 From: Shah Alam |

QUOTE(Jdite @ Jan 24 2019, 11:24 AM) Hi, Is Critical illness important? The payout is meant for your family A GE agent quoted me a Life Insurance with a rider for CI, which costs ~90 per month extra. As far as I understand, CI only pays out when the illness is at advance stage, and for GE, CI is part of the Life's SA. Isit worthwhile to pay RM90 extra per month just for that 'early payout'? As IMO, when your illness is at advance stage, the survival rate is also relatively low.. |

|

|

Jan 24 2019, 08:23 PM

Show posts by this member only | IPv6 | Post

#199

|

|

Junior Member

26 posts Joined: Oct 2010 |

QUOTE(Holocene @ Jan 23 2019, 09:30 PM) Ah, yea that's quite ok but do get the agent/staff to explain the terms and conditions, for example: So no choice have to go for ILP MC?Know what you are signing then you'll be alright Best, Jiansheng |

|

|

Jan 24 2019, 08:46 PM

|

|

Senior Member

945 posts Joined: Jun 2012 |

QUOTE(kentloonghh @ Jan 24 2019, 08:23 PM) So no choice have to go for ILP MC? Don't get me wrong, I'm not saying you definitely need to get an ILP.You should check out other standalone medical card before making that decision. Best, Jiansheng |

|

Topic ClosedOptions

|

| Change to: |  0.0388sec 0.0388sec

0.42 0.42

6 queries 6 queries

GZIP Disabled GZIP Disabled

Time is now: 3rd December 2025 - 04:47 AM |

Quote

Quote