http://www.theedgemarkets.com/article/prop...not-looking-yet

PROPERTY MARKET TO BE BADLY HIT IN 2018, Tekan the greedy sellers to the max!

|

|

Nov 17 2017, 06:22 PM Nov 17 2017, 06:22 PM

Return to original view | Post

#1

|

Junior Member

132 posts Joined: Nov 2006 |

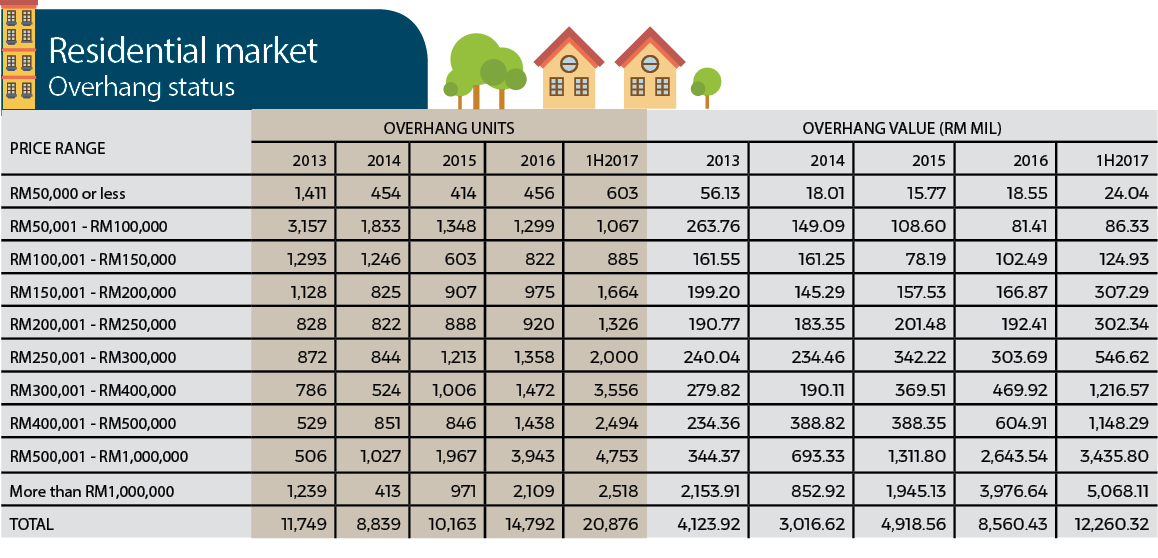

The increase of 40% overhang unit shock many parties perhaps... If you refer to theedge summary... for segment 500-1mil... the overhang value increase from 344mil to 3435mil (first half only) from 2013 to 1half 2017.... 10 times more already..... if trend continue.. what's the figure would be like?

http://www.theedgemarkets.com/article/prop...not-looking-yet |

|

|

|

|

|

Nov 23 2017, 11:35 AM

Return to original view | Post

#2

|

|

Junior Member

132 posts Joined: Nov 2006 |

QUOTE(aldtan @ Nov 22 2017, 11:24 AM) Not sure if this has been addressed but i think the key trigger for a property slowdown - continually stagnant prices for landed and significant correction to condos is the fact that the period of low interest rates are now over. Well, just look surrounding you... how many ppl that you know in-person had invested in property beside own stay unit? I can easily come out around 30+ in a minute. Many of them had justified the purchase with various reasons; i.e: ringgit shrink and inflation, treat as long investment for kid education fund, xxx friend / relative bought a house @ 300K in few years back and now 1mil, peer influence, rental passive income, prop price only goes up and limited land bank etc.Property prices - in PG, KL, JB since 2011 has been driven purely by increased affordability arising from a sustained period of all time low interest rates NOT from salary/increase. Sure people still have their jobs, but the fundamentals of property - economic and wage growth has not been supporting the level of prices we are at now. The US fed reserve is looking to hike rates 4x next year, BNM has already stated that it was hiking rates - (many expect 25-50 bps next year which will result in 5-7% increase in monthly mortgages) and stated that it will continue normalising interest rates over the course. Leading up to 2020 effective lending rates will likely be closer to 6%. So apart from the supply-demand imbalance, wages have to catch up to property prices on falling affordability levels. I can go on with this, but my question ia...are asset holders due for a rude awakening soon with the end of a multi year cycle? and how long will the downcycle last considering we are stuck in a middle income trap? Awaiting your insights :S  Sentiment is changed lately, lots of negative elements kick-in like higher lending rates, exceed supply, increased of government subsidized houses, harder to get tenant, expat is leaving, elite is leaving the country, foreign prop investor is lesser and list goes on. I believed in endowment effect... where ppl that already invested likely try drag it thru by subsidize the tenant and continue paying interest for bank so long their day-job is secured; instead of selling at loss now. I feel the depress situation will be continue at least 2-3 years if we're lucky. It'll goes pretty bad if global recession really hit during this period. Btw, the statement ""Leading up to 2020 effective lending rates will likely be closer to 6%""... it's a BNM indicative in their statement or purely a speculation? |

|

|

Nov 23 2017, 12:58 PM

Return to original view | Post

#3

|

|

Junior Member

132 posts Joined: Nov 2006 |

QUOTE(aaron1717 @ Nov 23 2017, 12:51 PM) for those generation before the bull run.... the 3 properties they have by that age is probably generating monthly 10k rental income for them.... and they never really need to touch the 1m in their bank account... It will goes up due to inflation in X years....and turned into long term player.... (don't want to sale at loss) < "strategy learned from pro stock investor"and in the end its depending on the exit strategy for property investment what type of property is it... if your property is not getting good rental yield... why u still wanna hold it til old age....  |

|

|

Nov 23 2017, 03:23 PM

Return to original view | Post

#4

|

|

Junior Member

132 posts Joined: Nov 2006 |

QUOTE(icemanfx @ Nov 23 2017, 01:26 PM) Property value rise at inflation rate in the long term. The key is sustainable loan repayment before could reap the reward. That's just a common move for most investor who stuck regardless in stock or property...of course most of average ppl aware of the repayment and certainly had built up their own buffer...(discounted those high risk taker, flipper or pro investor). Again, exception happened right? Some "asset appreciation" might actually lower than loan interest.... is Sungei Wang still the same 10 years back.  One should see the negative side of holding these asset in long run too... eg: cost & time opportunity where you can gain from other investment vehicle, long term commitment will limit your opportunity (less appetite to start a new biz or job change, etc), tenancy problems or no tenanted, added stress, anxiety and self-doubt, degraded lifestyle, property run down etc. If no more QE in coming years... god know when the next spike will come? Bear in mind factor like Malaysia become aging nation by 2035, city is be actually expanding (eg: greater KL to counter land limitation issue, we're not HK or SG), workforce pattern is changing for newer generation, flexi style and self-employed will affect property selection too (EFP SSP1M), middle income trap, etc During market is hot, there's tone of good reasons lead you to BBB, once turn sour, many bad reason will sound worrying. |

|

|

Nov 24 2017, 05:22 PM

Return to original view | Post

#5

|

|

Junior Member

132 posts Joined: Nov 2006 |

QUOTE(Nikmon @ Nov 24 2017, 04:13 PM) 4. Bank Negara informed the whole world that there are 130k unsold unit which is almost 100% increase when compare with last few years BNM is playing their role to ensure financial stability. Media will cook up anywhere based on NAPIC statistic.@frankly speaking, nobody would know this if they didn't announce it, now this was reported by all the main media, who dare to commit more loan.... Perhaps, the different is pea sized minister might react in different way... dont forget there're many property company owned by umno & kawan-kawan. |

| Change to: |  0.0262sec 0.0262sec

0.83 0.83

7 queries 7 queries

GZIP Disabled GZIP Disabled

Time is now: 30th November 2025 - 10:14 PM |

Quote

Quote