oh... yesterday news... after my position is cut at 6.60.

https://www.theedgemarkets.com/article/glov...ng-vaccinations

https://www.theedgemarkets.com/article/glov...ng-vaccinationsthis section below:

“Malaysian glove producers’ aggregate market capitalisation is 86% correlated to the US daily new testing data. The high 90% correlation was due to higher hospitalisation rate, driven by more testing, which in turn leads to higher demand for medical supplies and glove,” the bank commented.

The anticipated slower demand, JP Morgan said, implies limited upside to the average selling prices of the rubber glove.

In an earlier research note dated Jan 6, JP Morgan said it expects glove prices to reach a peak by the first half of 2021, with prices and profits to normalise thereafter.

The bank had compiled data of 18 countries, representing 17% of the world population, and found that besides India, Canada, Russia and the UK, the remaining countries it tracked are seeing a slow down in testing.

This limits the upside to glove prices, said JP Morgan, as “the more one tests, the more cases will be discovered which leads to hospitalisation and the need for medical supplies and gloves... Surges in testing created shortages which changed glove pricing from negotiated basis to spot”.

At the time, the average selling price stood at US$140 versus US$22 pre-Covid-19, which the bank said was driven by unsystematic buying.

Secured revenue growth is unsecured

Investors argue that the revenue growth is secured as most glove producers claim to have two or more years of order backlog, but JP Morgan begs to differ.

"It is crucial to understand order backlog and secured revenue. Orders are merely an agreement to buy a certain volume with prices determined or undecided. Buyers can walk away from it,” it wrote, noting that secured revenue is when customers have paid fully or partially for future delivery.

"As shown in Top Glove's quarterly results, we have indeed seen a sharp spike in deposits collected, from RM60 million a year ago to the latest quarter’s RM1 billion.

"However, the deposit paid is merely 4.7% of projected revenue for the financial year ending Aug 31, 2021 (FY21). It is not even equal to a month’s worth of glove sales," said JP Morgan.

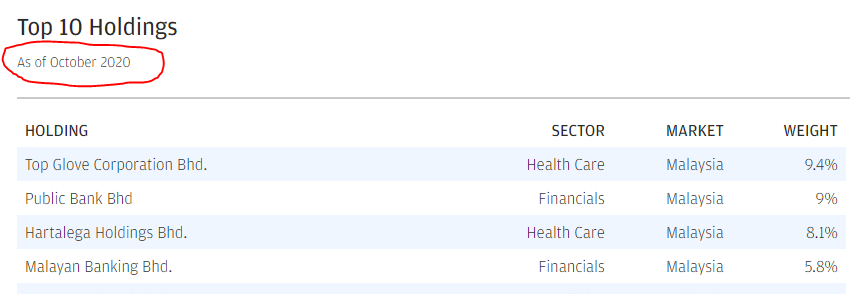

JP Morgan maintained “underweight” calls on Top Glove Corp Bhd with target price (TP) at RM3.50, Hartalega Holdings Bhd (TP: RM8.50) and Kossan Rubber Industries Bhd (TP: RM3.80).

However, it cautions that the risks to the calls on the three glove producers include a second global wave of Covid-19 which could lift glove prices to new heights, unscheduled capacity shutdowns, a significant fall in input costs such as nitrile and natural rubber, a significant step-up in dividend payouts as well as a substantial degree of ringgit depreciation.

Very fair reporting. Well i believe sure got some glove holder will try to counter each point with their own argument.

Jan 12 2021, 10:18 AM

Jan 12 2021, 10:18 AM

Quote

Quote

). Anything below 40x with a great management team, consistent growth, small to mid market cap seemed like a no brainer now.

). Anything below 40x with a great management team, consistent growth, small to mid market cap seemed like a no brainer now.

0.0333sec

0.0333sec

0.46

0.46

7 queries

7 queries

GZIP Disabled

GZIP Disabled