QUOTE(tchau83 @ Jun 20 2017, 08:16 PM)

Moving ASx fixed price funds to Esther bond might not be a good idea. ASx correlation to equities is near zero, while Esther bond to say, kgf, is 0.24 (post 5196 page 260). You might want to ask Xuzen to run algozen with ASx and see..

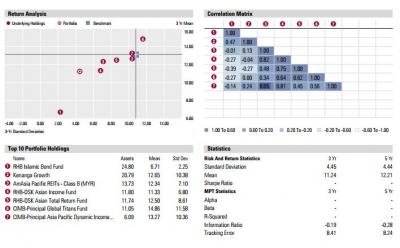

Some thoughts on the bonds recommended by algozen - they seemed somewhat risky. In the literature of standard 60/40 or 70/30 stock/bond portfolios, backtesting is usually done with S&P500 / 10 year treasuries. US treasuries and other high grade government debt are much safer and have negative correlation with stocks. In comparison, Esther bond is mostly emerging market corporate bonds. From the fund factsheet, 20+% of Esther bond are junk bonds (below BBB), assuming that 'Others' are grades lower than B.

RHB EMB seems a bit dodgy to me; I can't find any mention of the credit ratings of its holdings anywhere, and in %country allocation, 'others' has an allocation of 60%! What gives?! Better hope its not full of junk.

Anyway, its correlation to local stocks is surprisingly negative. Just a wild guess - when foreign funds pulled out of bursa en masse a few years ago, myr was severely devalued. This decreases the NAV of local stocks, while increasing the NAV of foreign bonds (RHB EMB) in ringgit terms. The RHB EMB might not be hedged to myr (can't find any mention) while Esther bond is. Hence Esther bond behaves more like EM/corporate bond - low positive correlation to stocks.

I doubt both bonds would fare well when the next economic crisis comes.

In 2015 and 2016, myr depreciated nearly 30% against USD, which affects the relative performance of local vs international stocks/bonds. This is probably a one off event (hopefully!), so it might not be prudent to base portfolios primarily off this time period. Algozen is based on past 3 years data, right?

RHB EMB mainly invests in government bonds. I don't have time to get you screenshots but you can see that clearly from the financial statements

In terms of ASx, there's 2 school of thoughts, depending on which angle you look at. They invests primarily in Msian equities, so investment risk wise is the same as the likes of KGF, public ittikal etc

But because they cap the fund value to 1.00 at all times, one would argue there's 0 volatility and hence is "risk-free"

However, the argument we usually put forth here is, given the same investment risk in Msia equity market, why not invest in KGF and the likes which give you >10% per annum compared to ASx of almost always below 10%. This applies to the non-bumi portion where ppl tend to put in and never take out for years.

For ASB where the bumi treats it like current account, that's a different story la

QUOTE(Ramjade @ Jun 20 2017, 08:27 PM)

Excuse me? ASx invest fully in bursa saham. Where did you get the info it have nearly correlation with equities. Why do you think ASx returns have been diminishing over time? It's because bursa saham have been in bad shape for almost 3 years.

I'm glad you actually say all these, at least my long winded comments didn't go to waste

QUOTE(puchongite @ Jun 20 2017, 09:50 PM)

Even though ASx invests in bursa, it is still possible they have low correlation with other local funds. This maybe due to the way the calculate return. Who knows what magic they put inside the calculation, don't you think so ?

Technically there's low correlation since it's always valued at 1.00 no matter how the equity market is doing. However, is the risk really 0? I think that's very much subjective. One could argue that it is risk free since I can always get back my capital given the political implications.

May 29 2017, 05:13 PM

May 29 2017, 05:13 PM

Quote

Quote what makes you think that....

what makes you think that....

Joking.

Joking. I kind of lost the link to the iportfolio/snapshot.

I kind of lost the link to the iportfolio/snapshot.

.

.

0.0450sec

0.0450sec

0.43

0.43

7 queries

7 queries

GZIP Disabled

GZIP Disabled