QUOTE(Deal Hunter @ Feb 23 2017, 12:03 AM)

Okuribito, if any pizza bimbo here calculates like that, please ask them to refer to you and michaelchang as their sifus for coming up with this misleading special interpretation of Effective Rate.

If you had not been reading properly, the problem is michaelchang's misinterpretation and those who did not read or understand later. The record is as follows:-

Frozz - Feb 20 8:01 PM

isn't HLB promotion (not taking the bonus into account) only 4% p.a. ?

that is only 2.666% since 8 months ... quite low IMHO.

Deal Hunter - Feb 20 10:17 PM

Yes, HLB interest is actually 2.666% of the principal as you figured 8 /12 x 4 %. It is up to the FD investor whether any luck to make another 4 months worth at 4% or end up with a higher or lower rate.

I agreed with Frozz that ACTUAL INTEREST is 2.666% of the PRINCIPAL which Frozz says is quite low for the risk.

michaelchang - Feb 21 5:28 PM

Because it's 8 months @4% interest the effective rate is 2.666??? If malaysian standard of mathematics is at this level, we are doomed to be 3rd world country for a long long time

Misinterprete and uses irrelevant jargon of EFFECTIVE RATE which was not in discussion at all till he puts this in.

Deal Hunter - Feb 21 11:25 PM

Nobody mentioned effective rate except you. Frozz and I both know that we will only get 2.666% return on the money put in.

okuribito - Feb 22 9:37 PM

Pizza bimbo reads this thread & learns that "effective interest" is calculated as "2.666% of the principal as you figured 8 /12 x 4 %" if the deal is 4% for 8mths

which was not what I wrote, but your own wrong interpration

wow so much drama here ... how did my "that is only 2.666% is a little low IMHO" turn into bimbos and pizzas ?

why am i also getting hints that i reported someone's post too ? i welcome all opinions and live in peace, do not have the time to report people

i only mentioned the E.R. for HLB is on the low side in my opinion, what say others ? suddenly bimbos and pizza comes in ... nice jokes

@deal hunter ... seems like you are the only one who gets what i am saying

QUOTE(cclim2011 @ Feb 22 2017, 04:44 PM)

The effective rate for hong leong is 4.0p.a regardless what is the duration of the FD.

I hope you can get the concept right.

even after i kindly break it down for you ... well if you say so pal cheers whatever floats your boat

Interest Rate = Interest rate / Marketed Rate

Effective Rate = Actual interest Rate you finally get which will be used to multiple with your deposited amount (some banks have started using this term like Maybank 3.91% rate promo)

Feb 21 2017, 09:06 PM

Feb 21 2017, 09:06 PM

Quote

Quote

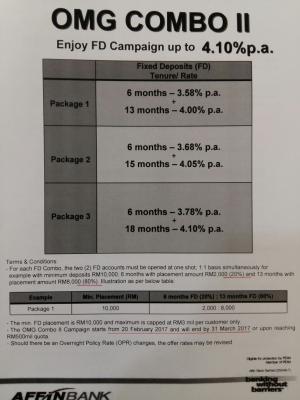

I collected their previous OMG Combo yesterday morning from Affin Islamic branch during walk around survey after EPF dividend announcement.

I collected their previous OMG Combo yesterday morning from Affin Islamic branch during walk around survey after EPF dividend announcement.

0.0282sec

0.0282sec

0.49

0.49

6 queries

6 queries

GZIP Disabled

GZIP Disabled