Dec 29 2018, 11:33 AM

Dec 29 2018, 11:33 AM

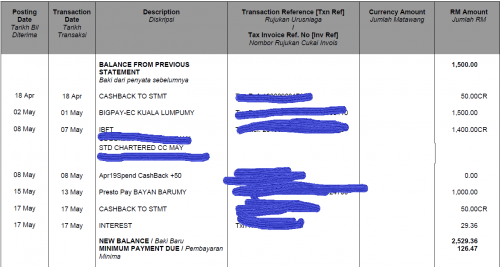

I read the terms and conditions for JOP but don’t understand.

. We will credit the amount of the CashBack to your credit card account or any other account we designate within the 60 days after the end of the relevant transaction months. All CashBack earned will not be automatically credited in the form of cash to your account. CashBack earned will only be redeemable via www.sc.com/my. Please refer to the CashBack Programme terms in the Rewards Terms.

Is what it means not automatically credited in cash?

Credit Cards Standard Chartered Bank Credit Cards V4, Everything About SC Credit Cards

Quote

Quote

The interest is pretty high but need to blame myself for overlook.

The interest is pretty high but need to blame myself for overlook.

0.0401sec

0.0401sec

0.14

0.14

7 queries

7 queries

GZIP Disabled

GZIP Disabled