Apr 4 2021, 08:20 AM

Apr 4 2021, 08:20 AM

https://www.wsj.com/articles/the-mortgage-m...355802?mod=e2tw

QUOTE

The mortgage market is humming, but getting approved for a home loan is as difficult as it has been in years.

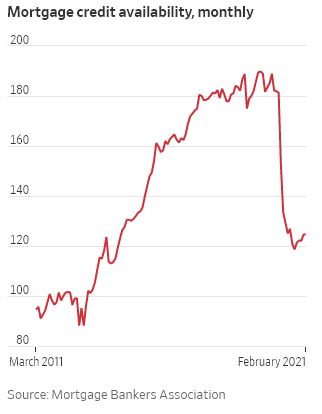

Mortgage credit availability, a measure of lenders’ willingness to issue mortgages, is near its lowest level since 2014, according to the Mortgage Bankers Association, or MBA.

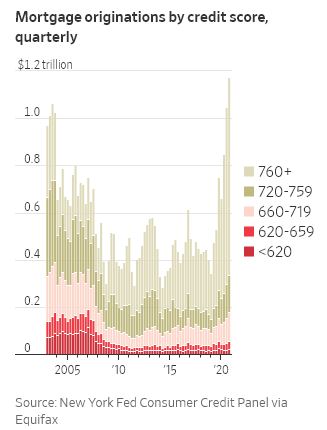

The tight lending environment illustrates a growing cleavage in the mortgage market: More home loans are being made than almost ever before, but they are going almost exclusively to borrowers with pristine credit histories and sizable down payments. Borrowers with credit qualifications that fall just outside the stellar category are finding fewer lenders willing to approve their applications. A segment of borrowers who would have qualified for a home loan early last year are now out of luck, deemed too much of a credit risk.

“Because mortgage credit is more difficult to obtain, it is a more competitive environment overall,” said Dr. Lawrence Yun, chief economist at the National Association of Realtors.

About 70% of mortgages issued in 2020 went to borrowers with credit scores of at least 760, up from 61% in 2019, according to the Federal Reserve Bank of New York.

The median credit score of borrowers approved for mortgages reached 786 in the fourth quarter of 2020, up from 770 during the same period in 2019.

Americans who want to break into the housing market this spring face plenty of other challenges. Home prices tend to fall in a slowing economy, but they have jumped during the coronavirus pandemic, keeping many families out of home ownership.

Home prices are increasing at the fastest pace in 15 years, propelled by a record-low supply of homes for sale and a flood of well-off workers looking for second homes or space for home offices. The median existing-home price topped $300,000 last summer and has stayed there ever since.

And mortgage rates, while still historically low, have risen meaningfully from last year’s record-setting lows, pushing monthly payments higher for would-be buyers.

The availability of mortgage loans plummeted as much as 35% year over year in 2020, when lenders wanted to protect themselves from making loans to borrowers who might lose jobs during the pandemic. The MBA’s mortgage credit index has drifted higher since last fall but remained about 31% lower in February than the same time last year.

“In one week last spring, jobless claims were in the millions,” said Tendayi Kapfidze, chief economist at LendingTree. “A borrower who was fine one week could be a much riskier borrower the next week.”

Lenders’ concerns about the financial stability of borrowers prompted them to increase verification of employment and income. Some borrowers were asked to sign statements affirming that they had no intention of requesting forbearance after being approved for a mortgage. Some lenders are asking that documents used in mortgage applications, such as bank statements and pay stubs, be no older than 30 days, where they once allowed them to be 60 days older or more.

Stricter credit requirements appeared most clearly at either end of the mortgage market. The average credit score for borrowers approved for Federal Housing Administration loans rose to 672 in the fiscal year 2020, up from 666 in 2019. FHA loans typically have lower incomes and smaller down payments.

At the same time, lenders upped requirements for jumbo mortgages, which tend to go to well-off buyers. Jumbo mortgages are too big to be sold to government-backed mortgage giants Fannie Mae and Freddie Mac, so banks often keep them on their own books and bear the risk of default.

Jeanne Griffin’s local credit union in Minnesota denied her mortgage application earlier this year. She said she was told her 713 credit score and the fact that her student loans were in pandemic-related forbearance disqualified her.

“They said if I had applied a year ago, I would have been approved,” said Ms. Griffin, who has close to $20,000 saved for a down payment.

The credit union encouraged her to begin making student-loan payments and pay off about $4,000 in credit-card debt before reapplying.

The meteoric growth of home prices has made some lenders reluctant to take on first-time home buyers or others they view as slightly risky. Lenders who were comfortable offering mortgages of $300,000 or $320,000 to borrowers with good-but-not-great credit histories might not be willing to lend the $350,000 or more now required to buy the same property.

Loan officers and underwriters weigh a handful of variables when determining whether to approve a mortgage application: employment history, income source, credit score and debt level, among others.

Are you looking to buy a house for the first time? Share your experience below.

Strict lending requirements play an important role in keeping the housing market healthy. Making sure that borrowers can afford mortgage payments is key to limiting defaults. Ultraliberal lending policies, including loan approvals for people with spotty income histories or mountains of debt, helped spark the 2008-09 financial crisis.

Lending standards are unlikely to expand meaningfully until housing demand ebbs, economists said. The dearth of homes for sale means lenders can select only the best from an abundance of applications.

Still, credit requirements should loosen slightly this year as interest rates rise, drying up refinancing, said Mike Fratantoni, the MBA’s chief economist.

“Since lenders aren’t being flooded with calls to refinance, more of their resources can be used to reach out to first-time buyers for purchases,” Mr. Fratantoni said.

Refinance loans are expected to comprise 46% of the mortgage market in 2021, down from 59% in 2020, according to the MBA.

Mortgage credit availability, a measure of lenders’ willingness to issue mortgages, is near its lowest level since 2014, according to the Mortgage Bankers Association, or MBA.

The tight lending environment illustrates a growing cleavage in the mortgage market: More home loans are being made than almost ever before, but they are going almost exclusively to borrowers with pristine credit histories and sizable down payments. Borrowers with credit qualifications that fall just outside the stellar category are finding fewer lenders willing to approve their applications. A segment of borrowers who would have qualified for a home loan early last year are now out of luck, deemed too much of a credit risk.

“Because mortgage credit is more difficult to obtain, it is a more competitive environment overall,” said Dr. Lawrence Yun, chief economist at the National Association of Realtors.

About 70% of mortgages issued in 2020 went to borrowers with credit scores of at least 760, up from 61% in 2019, according to the Federal Reserve Bank of New York.

The median credit score of borrowers approved for mortgages reached 786 in the fourth quarter of 2020, up from 770 during the same period in 2019.

Americans who want to break into the housing market this spring face plenty of other challenges. Home prices tend to fall in a slowing economy, but they have jumped during the coronavirus pandemic, keeping many families out of home ownership.

Home prices are increasing at the fastest pace in 15 years, propelled by a record-low supply of homes for sale and a flood of well-off workers looking for second homes or space for home offices. The median existing-home price topped $300,000 last summer and has stayed there ever since.

And mortgage rates, while still historically low, have risen meaningfully from last year’s record-setting lows, pushing monthly payments higher for would-be buyers.

The availability of mortgage loans plummeted as much as 35% year over year in 2020, when lenders wanted to protect themselves from making loans to borrowers who might lose jobs during the pandemic. The MBA’s mortgage credit index has drifted higher since last fall but remained about 31% lower in February than the same time last year.

“In one week last spring, jobless claims were in the millions,” said Tendayi Kapfidze, chief economist at LendingTree. “A borrower who was fine one week could be a much riskier borrower the next week.”

Lenders’ concerns about the financial stability of borrowers prompted them to increase verification of employment and income. Some borrowers were asked to sign statements affirming that they had no intention of requesting forbearance after being approved for a mortgage. Some lenders are asking that documents used in mortgage applications, such as bank statements and pay stubs, be no older than 30 days, where they once allowed them to be 60 days older or more.

Stricter credit requirements appeared most clearly at either end of the mortgage market. The average credit score for borrowers approved for Federal Housing Administration loans rose to 672 in the fiscal year 2020, up from 666 in 2019. FHA loans typically have lower incomes and smaller down payments.

At the same time, lenders upped requirements for jumbo mortgages, which tend to go to well-off buyers. Jumbo mortgages are too big to be sold to government-backed mortgage giants Fannie Mae and Freddie Mac, so banks often keep them on their own books and bear the risk of default.

Jeanne Griffin’s local credit union in Minnesota denied her mortgage application earlier this year. She said she was told her 713 credit score and the fact that her student loans were in pandemic-related forbearance disqualified her.

“They said if I had applied a year ago, I would have been approved,” said Ms. Griffin, who has close to $20,000 saved for a down payment.

The credit union encouraged her to begin making student-loan payments and pay off about $4,000 in credit-card debt before reapplying.

The meteoric growth of home prices has made some lenders reluctant to take on first-time home buyers or others they view as slightly risky. Lenders who were comfortable offering mortgages of $300,000 or $320,000 to borrowers with good-but-not-great credit histories might not be willing to lend the $350,000 or more now required to buy the same property.

Loan officers and underwriters weigh a handful of variables when determining whether to approve a mortgage application: employment history, income source, credit score and debt level, among others.

Are you looking to buy a house for the first time? Share your experience below.

Strict lending requirements play an important role in keeping the housing market healthy. Making sure that borrowers can afford mortgage payments is key to limiting defaults. Ultraliberal lending policies, including loan approvals for people with spotty income histories or mountains of debt, helped spark the 2008-09 financial crisis.

Lending standards are unlikely to expand meaningfully until housing demand ebbs, economists said. The dearth of homes for sale means lenders can select only the best from an abundance of applications.

Still, credit requirements should loosen slightly this year as interest rates rise, drying up refinancing, said Mike Fratantoni, the MBA’s chief economist.

“Since lenders aren’t being flooded with calls to refinance, more of their resources can be used to reach out to first-time buyers for purchases,” Mr. Fratantoni said.

Refinance loans are expected to comprise 46% of the mortgage market in 2021, down from 59% in 2020, according to the MBA.

Quote

Quote

0.4170sec

0.4170sec

0.87

0.87

7 queries

7 queries

GZIP Disabled

GZIP Disabled