QUOTE(xuzen @ Aug 14 2016, 11:14 AM)

... Do you calculate them yourself ...

Office system does all the heavy lifting la. If it has to be done manually, I won't have time to layan LYN and chase Pokemon already. Anyway, I don't really rely on ratios when it comes to funds. Not useful when managers make changes to the portfolio, actively rebalance holdings or keluar mandate. It becomes qualitative instead of quantitative.

» Click to show Spoiler - click again to hide... «

Anyway, these ratios are WMDs as there is a tendency to curve fit to maximize the numbers, without understanding the implications

Investors tend to want to be spoon fed, or be given strict guidelines on how to make money. So when they are told simply that a high sharpe ratio is good, they will just sort funds by sharp ratio, and pick a few funds with the high returns ... fits the "curve".

Hypothetical situation :

4Q2014 :

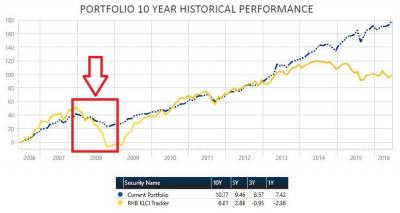

- 1Y, 3Y Sharp ratios for CIMB APDI, Eastspring MY Focus, Kenanga Syariah Growth all above 1.3, APDI >2.0

- 1Y, 3Y (and some 5Y) performance was double digit.

- "High sharpe" and "high returns" ..... go balls deep lor.

1Q2016 :

- Invested for one year all the "winners" are now "losers".

- Portfolio is down 10-20%.

- Too painful, cut loss. The end.

10-20% may not sound like a lot, but when it can buy a house, it can be painful, even to HNIs. Which is why WMDs, weapon of mass destruction.

This post has been edited by lukenn: Aug 14 2016, 12:53 PM

Jun 15 2016, 07:08 PM

Jun 15 2016, 07:08 PM

Quote

Quote What the hell was it reported for? I am asking a genuine question.

What the hell was it reported for? I am asking a genuine question.

... if at his age I was asking these questions, instead of trying to khau lui, I think I'll be much better off now.

... if at his age I was asking these questions, instead of trying to khau lui, I think I'll be much better off now.

0.2449sec

0.2449sec

0.53

0.53

7 queries

7 queries

GZIP Disabled

GZIP Disabled