Apr 8 2016, 02:22 PM

Apr 8 2016, 02:22 PM

QUOTE(cherroy @ Apr 8 2016, 11:46 AM)

In ILP, the so called "return" may be used to burn the future rise in premium of cost of insurance.

Somemore in ILP, the investment portion is not capital guaranteed, it can result in a loss as well, instead of "return".

ILP = insurance + UT.

Standalone medical = insurance without UT.

Somemore in ILP, the investment portion is not capital guaranteed, it can result in a loss as well, instead of "return".

ILP = insurance + UT.

Standalone medical = insurance without UT.

QUOTE(Ayrehn @ Apr 8 2016, 02:12 PM)

True also. But better than no returns at all right

You pay for the UT, and what is the IRR of the investment linked UT compared to if you can buy any UT that is not provided by insurance company?

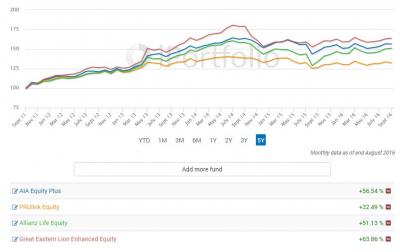

I'm a prudential client; and I can tell you the Inv linked funds performance is no where near what Eastspring investment (pure UT arm) funds are doing

If I can turn back time and choose my insurance plan again, I would check the linked fund returns on top of considering the coverage and benefits

Quote

Quote

0.0818sec

0.0818sec

0.09

0.09

7 queries

7 queries

GZIP Disabled

GZIP Disabled