How to Beat EPF?In the previous post, the 10-year annualized rate of EPF in the past 10 years from 2008 to 2017 was shown. It range from 4.50% to 6.90%, and a simple average of 6.02%.

While it was shown that some funds can have better returns than EPF, we should also note that EPF is the biggest mutual fund with 7-8 hundred billion in assets, and have huge revenue flowing in every month, was established more than 50 years ago, and have both in-house and external 3rd party investment teams running the show.

Needless to say, EPF can compete and outperform against many conservative mutual funds. To beat EPF, we will have to try a different field where EPF is not playing and not going head to head against it.

What fields to play? Aggressive small-cap funds, and non-local funds. And this is supported by the funds that beat EPF:

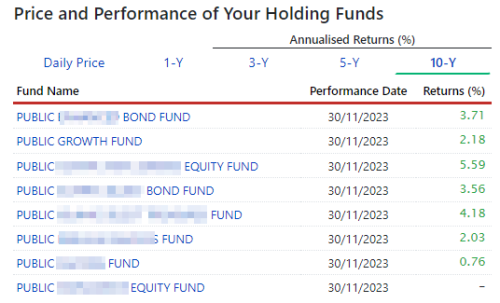

Public SmallCap Fund. 10-year total return: 136.96%

Public Islamic Opportunities Fund . 132.8%.

PB Asean Dividend Fund. 94.4%.

(If not mistaken, all the above 3 funds are oversubscribed and closed to fresh investments.)

Funds that were launched less than 10 years ago:

Public Far-East Alpha-30 Fund. 5-year total return: 101.5%

PB China Asean Equity Fund. 102.2%

When to play? EPF is in the market 24/7. To beat them, the ordinary investor has to stay in the game too.

Dropping in and out of the game (at random or following market noise or can’t handle the ‘paper loses’) means losing the game, unless of course the investor can perfectly time all his entries and exits.

So, what is the likeliest method to beat EPF? Long term buy-and-hold method. No short term timing – that is buys and sells frequently.

When to buy/invest? All the time. As and when you have spare money to invest.

What about those 10-year economic cycles? What about them?!!!

Buy all the time – whether the market is up or down – without timing… since your “long-term” is 20 to 30 years… even a 40 years buying cycle is possible if started at age 20.

What if you don’t have 10, 20 or 30 years to buy/invest continuously? Well, if you can’t beat them, you can join them.

Put the money into EPF. Or you can try your luck and put some into an equity fund too.

=========

If you are a short term player or planning to time the market, you may be interested to know that there are several funds with satisfactory YTD returns. Just to let you know what is possible... good luck!

PB Islamic Dynamic Allocation Fund

Public Islamic Global Equity Fund

Public Strategic Growth Fund

(Check their YTD returns since 29 Dec 2017.)

Have you check whether these funds which you have mentioned here are available for investment via EPF? Similar to your previous post where you have analyse and compare the performance of EPF vs some selected funds which you mentioned could beat EPF?

A quick check show otherwise...these funds are not available under EPF investment scheme. Perhaps you could just limit the analyse and comparisons to those available under the scheme instead.

Aug 7 2018, 02:22 PM

Aug 7 2018, 02:22 PM

Quote

Quote

I kinda agreed after having leave most of the decision to buy and choice of funds to my agent. I have learned that you need to manage your own funds rather than depending on your agent.

I kinda agreed after having leave most of the decision to buy and choice of funds to my agent. I have learned that you need to manage your own funds rather than depending on your agent.

0.1038sec

0.1038sec

0.41

0.41

7 queries

7 queries

GZIP Disabled

GZIP Disabled