QUOTE(kradun @ Sep 24 2016, 09:28 AM)

But after 4-5 years with max return 0.46% can get total return up to 21%? That probably have mixed up with something else.

Those are the fund allocation percentage in his portfolioPublic Mutual Funds, version 0.0

|

|

Sep 24 2016, 09:34 AM Sep 24 2016, 09:34 AM

Return to original view | Post

#1

|

Senior Member

1,166 posts Joined: Jul 2016 |

QUOTE(kradun @ Sep 24 2016, 09:28 AM) But after 4-5 years with max return 0.46% can get total return up to 21%? That probably have mixed up with something else. Those are the fund allocation percentage in his portfolio |

|

|

|

|

|

Oct 14 2016, 10:13 AM

Return to original view | Post

#2

|

|

Senior Member

1,166 posts Joined: Jul 2016 |

QUOTE(dasecret @ Oct 14 2016, 10:08 AM) Abang, I think you have not looked at the unit trust industry landscape for a while Straight to the point Instead of choosing a single fund house, now you get the option of almost all the fund houses by going to: 1) Banks - their offering still a bit limited due to their shortlisting requirements, more foreign feeder funds 2) FA Firms/CUTA/IUTA - provided CFP advisory and portfolio construction with funds from various fund house 3) DIY via fundsupermart - cheap sales charge, easy to switch, again, availability of most funds from most fund houses Who cares about the single ancient titanic fundhouse with lots of poor performance funds anymore. And seriously, 5.25% sales charge even if I do it myself on the online portal?!  Especially the last one  so little discount even DIY via public mutual online so little discount even DIY via public mutual online  which is one of the main reason I am hesitant to give public mutual a chance to explore what they offer, not to mention their sub par performance compare to its peers within the same period, the gap is really unjustifiable  This post has been edited by AIYH: Oct 14 2016, 10:14 AM |

|

|

Dec 31 2016, 03:31 PM

Return to original view | Post

#3

|

|

Senior Member

1,166 posts Joined: Jul 2016 |

QUOTE(contestchris @ Dec 31 2016, 03:06 PM) Guys what are the sales charge fees to enter Public Mutual, and what is the annual MER (Management Expense Ratio) of their funds? Is it in line with other funds from companies like CIMB-Principal, RHB, Eastsprings and TA? You need to read their respective product highlight sheet and annual report to find out the SC and MER for each fundIf Public Mutual has higher MER than the other fund companies in Malaysia, that may explain their lower than normal returns. I think the best way is to educate yourself and buy "open market" funds from the companies I listed above rather than closer market funds like PM. And define open market, because, afaik, pm hass very very very little difference to cimb kenanga TA etc in terms of mutual fund offering  |

|

|

Jan 1 2017, 01:30 PM

Return to original view | Post

#4

|

|

Senior Member

1,166 posts Joined: Jul 2016 |

QUOTE(Avangelice @ Dec 31 2016, 08:03 AM) for those looking to buy into PM. I think they update the bloomberg graph dy, sometimes they delay in distribution informationhave a go at Bloomberg and key in every PM fund within the search bar and study the performance of each PM funds especially the graph performance for 1 yr and 5 years. not sterling performance now is it? the Ytd for public savings fund is - 6.33% public focus ytd loses hovering at - 5.71% public Islamic savings fund -5.03% PB growth sequel fund -9.41 mind you those are negative returns. i felt a need to post this up after public mutual went on the papers to declare their "dividends" . please be aware dividends are priced in your NAVs and don't do jack shit. just doing my part to educate. I do not like it when companies use false propaganda to push people to use them. You might need to see PM own performance chart (which do include distribution reinvestment) vs its peers on FSM performance chart to get a apple to apple comparison QUOTE(frankzane @ Jan 1 2017, 01:22 PM) I still dont understand the concept of dividends dont do shit jack. In mutual funds, distribution doesn't actually increase your wealthWhenever distribution declare, it was taken from the NAV, hence NAV reduced by the distribution declared. You need to reinvest the distribution in order to get back the same fund value as you have before distribution Otherwise, if the distribution is not reinvest, goes to cash in you hand instead, even though u get the cash, your fund value will decrease by the distribution amount. This post has been edited by AIYH: Jan 1 2017, 01:34 PM |

|

|

Jan 10 2017, 10:17 PM

Return to original view | Post

#5

|

|

Senior Member

1,166 posts Joined: Jul 2016 |

QUOTE(e_X @ Jan 10 2017, 10:14 PM) Hi, hard to digest in this topic but I make it a simple question Not sure about PMO but FSM do have such feature with lower SCOpen 1000 for an account but every month add 300. The question is, it is easy to add fund maybe like m2u transfer without agen? Gonna invest for a long time > 20 years. I don't want auto deduction on my bank account. But you need to ensure what fund you invest  |

|

|

Jan 10 2017, 10:59 PM

Return to original view | Post

#6

|

|

Senior Member

1,166 posts Joined: Jul 2016 |

QUOTE(e_X @ Jan 10 2017, 10:38 PM) For PMO i can invest fund like Public SmallCap and for FSM like Kenanga Growth right? Minimum for FSM is 100? Normally rm1000 to start and rm100 to top up, however you can start with 100 by subscribing to RSP (monthly regular saving) in FSMYou are right, but is better to compare the same sector region and class between peers to see which fund house provides the best return or risk return ratio |

|

|

|

|

|

Jan 10 2017, 11:27 PM

Return to original view | Post

#7

|

|

Senior Member

1,166 posts Joined: Jul 2016 |

QUOTE(kyone @ Jan 10 2017, 11:12 PM) Any PM fund in foreign currency? Did a simple google but can't get any useful info. You can check from here https://iportfolio.com.my/screenIf dont have means there is no FCY mutual fund by PM |

|

|

Jan 11 2017, 02:50 PM

Return to original view | Post

#8

|

|

Senior Member

1,166 posts Joined: Jul 2016 |

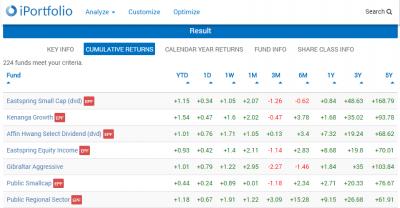

QUOTE(eastwest @ Jan 11 2017, 02:36 PM) My friends said now will be a good time to buy unit from PM since the price is lower than before.. Now is a good time to buy, but not necessary from PMTo give you an idea, compare top 7 MY funds from PM vs top 7 MY funds in Malaysia Attached thumbnail(s)

|

|

|

Jan 11 2017, 03:43 PM

Return to original view | Post

#9

|

|

Senior Member

1,166 posts Joined: Jul 2016 |

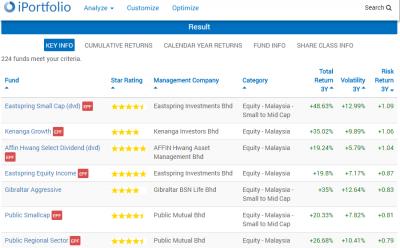

QUOTE(eastwest @ Jan 11 2017, 03:34 PM) I see.. There are a lot of ways to look, each column provides different meaningActually which part in the column is the most important one that I should take note? The YTD? For example, the 3 year risk return ratio is the 3 year annualized return generated per unit of risk being taken. Generally, the higher the number, it means that within the same class of fund (equity / fixed income), it generate better return given the risk it took Lower number generally means the risk you need to bear doesnt worth the return it generated. the other cumulative performance data with different dates tell you about how each fund perform for different period, whether some funds perform better or worse recent or long term wise, which can generate better or certain returns than others for more comparison on your research, refer to iportfolio.com.my or fundsupermart.com.my or bloomberg or morningstar, but the main idea is this: PM is only on of the many fund houses in Malaysia, each fund houses had different strength in certain areas of performance, and as you will see, for each region/sector/class, they topped by different fund houses, therefore, it is important to research and compare before you decide which is better to invest, be open minded in exploring information This post has been edited by AIYH: Jan 11 2017, 03:45 PM |

|

|

Jan 11 2017, 04:24 PM

Return to original view | Post

#10

|

|

Senior Member

1,166 posts Joined: Jul 2016 |

QUOTE(eastwest @ Jan 11 2017, 04:15 PM) Thanks for the insight... IMO is hard to interpret it as a standalone valueand for the bold part, based on your example, what is the lowest number for return that is considered as worth the risk? For example, money market tend to have high RRR due to low volatility/ nil fluctuation, however that return may not be what you desire RRR is best to compare with several funds For example, within malayisa region equity fund, you can compare which fund has higher RRR compare to its peer, it will generally means that given the risk it takes, it can generate better return than its peers Its best to compare it in conjunction with their return within the same period the RRR were measured The picture I attached previously were sorted by RRR descending, so the top one usually can be intepreted as the better fund that can generate high return for its volatility That is the basic way to choose a good fund, if you want to go deeper, you proceed to study each fund's FFS, PHS and annual report to understand what they invest and why such a difference between funds This post has been edited by AIYH: Jan 11 2017, 04:36 PM |

|

|

Jan 11 2017, 10:16 PM

Return to original view | Post

#11

|

|

Senior Member

1,166 posts Joined: Jul 2016 |

QUOTE(ehwee @ Jan 11 2017, 05:37 PM) Thanks for the great guides, @AIYH do you mind to share your thought on smallcap fund either public or eastspring, these fund is it consider high risks if we consider mid term investment like 3-5 yrs from now? Personally I choose eastspring small cap for 4 reasons:1) Sales Charge : Public Mutual charge SC about 5% to 5.5% per investment, which may not seem much if you invest once, but to me who advocate to DCA every month by income, that will be costly to me For Eastspring, I can buy from FSM from 0.5% to 2% SC per investment, lower cost to DCA for me 2) Performance : From the performance data and chart that I posted previously along with the website you can check, EI small cap beat Public small cap by some margin 3) Flexibility : Staying invested in an isolated fund house platform, I find it hard to switch around and compare between peers if the market doesnt turn well or you want to diversify into something different In FSM, I can compare and switch between fund houses if I forsee another fund house having a better fund that what I own now, invest EI small cap in FSM allows me to switch to different fund houses in the future within the platform 4) Documents : PM hardly publish FFS publicly to update their investors about the fund update, whereas other fund house they provide FFS on their website by monthly, easier to study and compare within FSM That is just my opinion, I haven't have the knowledge to read in depth in the fundamentals of what they invest, what difference do they make and their future potential prospect, so I just provide my basic reasoning As far as I know, small cap in Malaysia is still an inefficient market, therefore investors or fund manager can try to compete for information, insight and careful selection to outperform the market. Though it is less risky compare to sector specific like property funds, it is still riskier than large cap funds, so it is advisable not to put what you cant afford to lose into this segment QUOTE(eastwest @ Jan 11 2017, 06:50 PM) There are so many terms in this topic that I don't know yet... So many things to learn.. Unless you are lucky or very rich to have a very good agent or financial planner that will update you promptly and advise you accordingly, chances that you will need to self study and understand your investment to prevent being cheated and misguided by own sentiment and peer influenceThank you again. I have been through that, and still learning Just wish to spread this awareness in some self study on your own investment |

|

|

Jan 11 2017, 10:51 PM

Return to original view | Post

#12

|

|

Senior Member

1,166 posts Joined: Jul 2016 |

QUOTE(e_X @ Jan 11 2017, 10:36 PM) Thanks You can either subscribe to monthly RSP or top up on your own pace.AIYH Can I do this at FSM or I need minimum RM 100 every month? Usually they will have seperate minimum for manual top up and RSP This fund [URL=https://www.fundsupermart.com.my/main/fundinfo/Manulife-Investment-U-S-Equity-Fund-MYML008] MANULIFE INVESTMENT U.S. EQUITY FUND[/URL] have different minimum manual top up and RSP EASTSPRING INVESTMENTS SMALL-CAP FUND have both the same minimum You can either put an initial investment into it or trigger a RSP for 1 month which happens on 15th of every month, then cancel it, then you can top up manually according to the subsequent investment amount whenever you like |

|

|

Jan 18 2017, 11:21 PM

Return to original view | Post

#13

|

|

Senior Member

1,166 posts Joined: Jul 2016 |

QUOTE(Holocene @ Jan 18 2017, 11:18 PM) If I have an existing fund that was bought via an agent, I do monthly contribution. Can I choose to stop paying via auto debit and buy the units from FSM instead? Afaik, FSM do not offer public mutual funds.BUt if you want its peers, you may talk to FSM about your change from PM to FSM, they will guide you, or refer to wongmunkeong 's guide on previous pages |

|

|

|

|

|

Jan 19 2017, 05:58 AM

Return to original view | Post

#14

|

|

Senior Member

1,166 posts Joined: Jul 2016 |

QUOTE(Holocene @ Jan 18 2017, 11:46 PM) Hmum I didn't know that but I wasn't thinking about PM 🤓 thanks by the way.. If the fund you bought from agent is available in FSM, then the process will be much easier  |

|

|

Jan 19 2017, 08:13 AM

Return to original view | Post

#15

|

|

Senior Member

1,166 posts Joined: Jul 2016 |

QUOTE(wongmunkeong @ Jan 19 2017, 07:57 AM) er.. not necessarily I tried moving my EastSpringInvesments SmallCaps to FSM from a Prudential agent (bought >10 years back): 1. FSM asked me to contract ESI 2. ESI asked me to get agent to sign-off on the transfer - ie. she will lose her "assets under management" commissions from my portion if moved 3. Guess what happens next? dang.. Means her commission paid in the past will be revoked? |

|

|

Jan 26 2017, 07:49 PM

Return to original view | Post

#16

|

|

Senior Member

1,166 posts Joined: Jul 2016 |

QUOTE(Rasheed.JF @ Jan 26 2017, 06:43 PM) I have been a Public Mutual agent for years, then I Quit. There is a point where it is sucks to sell something that you can't control . One of the fund PISSF, didnt declare dividend in 2016. That is a sign for me to shy away. Unit trust is not stockThe distribution are irrelevant because when distribution declared, the NAV drop If you opt for cash, your capital will shrink If you opt for reinvestment, it will just reinvest back into your capital and your fund value didn't change You should focus on the fund performance instead of distribution, |

|

|

Jan 26 2017, 10:33 PM

Return to original view | Post

#17

|

|

Senior Member

1,166 posts Joined: Jul 2016 |

QUOTE(wongmunkeong @ Jan 26 2017, 10:28 PM) psst.. agent leh If agent don't tell you this, they either don't know, which may be new or don't really care type (if he willing to learn, then still got hope  ) )Or those who purposely con customer for self interest (this one no hope, boycott )This post has been edited by AIYH: Jan 26 2017, 10:35 PM |

|

|

Jan 27 2017, 12:51 PM

Return to original view | Post

#18

|

|

Senior Member

1,166 posts Joined: Jul 2016 |

QUOTE(Rasheed.JF @ Jan 27 2017, 11:22 AM) Market have drop tremendously since end of 2014. Not just PISSF, many funds does not perform as good as before. Many of my client, I do advice them to put their money elsewhere. But if they still want to wait (5 -10 years), it is up to them. You can check yourself the performance of PISSF in Bloomberg. » Click to show Spoiler - click again to hide... « PIDF and PITSEQ still OK, but many opt for Asia fund. I just don't want the same case as Ittikal China happened again, until now, many people haven't recovered their capital since first invest. But whoever did re invest during down time, surely make some money. PISGIF still not making money since first inception. QUOTE(Rasheed.JF @ Jan 27 2017, 11:39 AM) Look, I am not saying that Unit Trust is bad per se. But if possible I want to gain the customer's trust, and it is not my money, it's theirs. I can't be playing around when the economy is bad and then I go and say, this is the best time to invest. I am not saying that UT is a bad product, dont worry Yes the price is damn cheap, but when do you think they will make money? 5-10 years? I mean that is waaayy to long. I may not have the talent to twist my word to say bad thing as good thing. There will be at some point that you will meet a client who is well verse in the market than the agent. That's when you learn a lot. You can try to check Public Mutual performance in Morning Star, Public Mutual fund is hardly on top 10. Marketing and Facts is different. Just the fact that other than public mutual, there are other fund houses which have better performing fund for certain categories For instance, PISSF

and Eastspring Investments Dana Al-Ilham

(both islamic malaysia general equity) There are other funds which public mutual excel, like public islamic opportunities (islamic malaysia small cap) Just that if you want customer to have the best, pick them the fund that public mutual do best |

|

|

Apr 3 2017, 09:47 PM

Return to original view | Post

#19

|

|

Senior Member

1,166 posts Joined: Jul 2016 |

QUOTE(lch78 @ Apr 3 2017, 09:39 PM) I already have substantial investment in iFast platform. Dont diversify by fund houses I just want diversification.  Rather by region, pick the best across different fund house If u want diversify, go for other investments like stock bonds FD forex to diversify your risk |

| Change to: |  0.0954sec 0.0954sec

0.67 0.67

7 queries 7 queries

GZIP Disabled GZIP Disabled

Time is now: 4th December 2025 - 08:12 AM |

Quote

Quote