Oct 6 2019, 09:57 PM

Oct 6 2019, 09:57 PM

QUOTE(boldsouljah @ Oct 6 2019, 09:47 PM)

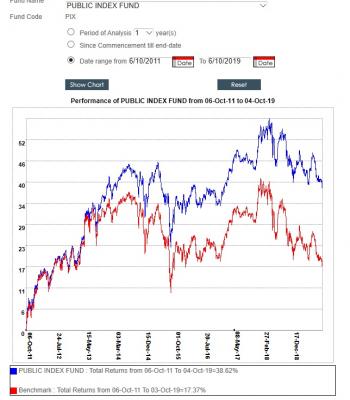

Sorry, mine is the EPF scheme. I have been putting money into PM from my EPF for the past 7 years, So now i have around 74k, and it shows Total Returns : -RM6454

Sales charge for EPF is 3%.....

Sales charge for EPF is 3%.....past 7 yrs doing periodic reinvestment....

with minus 8% ROI......It will be a tough nut to beat if were to includes the cumulation of the yearly 6% opportunity cost

may I suggest you stop the reinvestment but invest into some other fund or just stop taking out the money from EPF to earn 6%

btw, did you do the calculation of profit/losses by yourself?

This post has been edited by MUM: Oct 6 2019, 09:59 PM

Attached thumbnail(s)

Quote

Quote

alamak

alamak

it allows unitholders to make investment and transaction requests (including redemption and switching), and enquire on account balances, transactions and statements.

it allows unitholders to make investment and transaction requests (including redemption and switching), and enquire on account balances, transactions and statements.

0.0961sec

0.0961sec

0.36

0.36

7 queries

7 queries

GZIP Disabled

GZIP Disabled